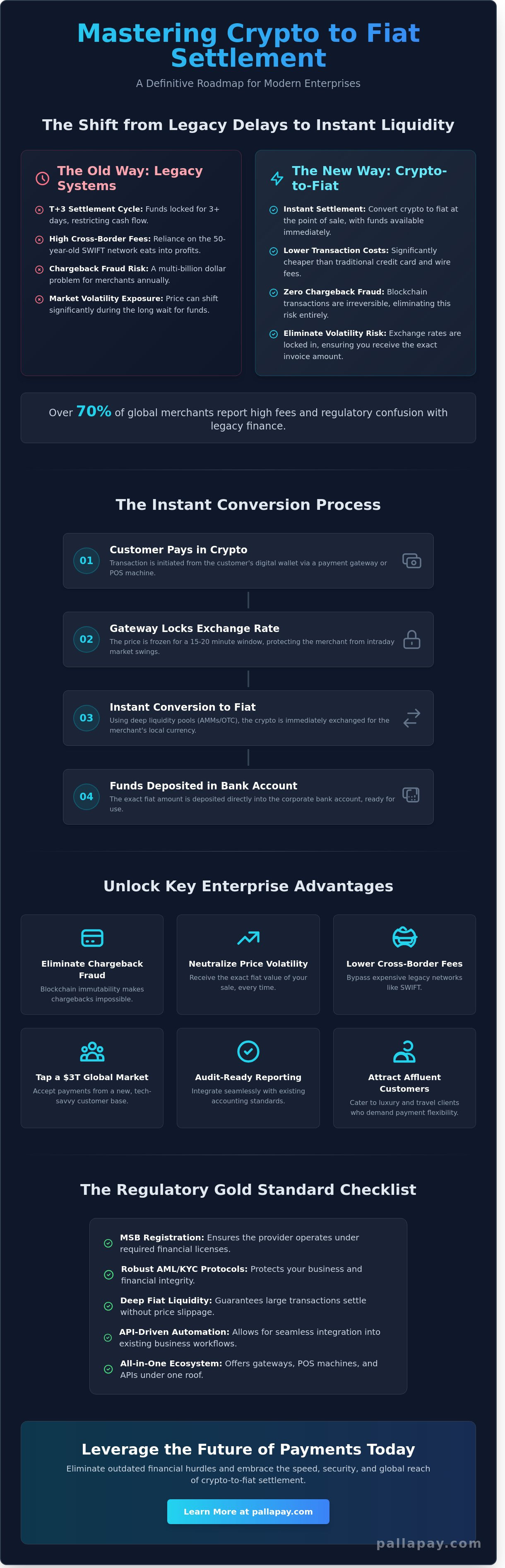

A business operating on a T+3 settlement cycle in 2026 is essentially functioning in the past while its competitors move at the speed of light. You’ve likely felt the frustration of watching market prices shift during the long wait for funds to clear your traditional bank account. It’s a common struggle; over 70% of global merchants report that the bridge between digital innovation and legacy finance is often paved with high fees and confusing MSB regulations. This guide provides a definitive roadmap to mastering crypto to fiat settlement, transforming what was once a complex hurdle into a streamlined, instant advantage for your enterprise.

We’ll show you exactly how to eliminate price volatility risks and secure lower transaction costs than standard credit card networks. You’ll gain a comprehensive understanding of how to implement audit-ready reporting and instant conversion technology that scales across borders. This breakdown prepares your business to leverage the future of payments with absolute confidence and institutional reliability.

Key Takeaways

- Understand how to transition from holding digital assets to utilizing them as high-speed payment rails for modern global commerce.

- Learn how advanced payment gateways lock in real-time exchange rates to eliminate price volatility during the conversion process.

- Master the strategic choice between instant and batch crypto to fiat settlement to optimize your business cash flow and minimize bank fees.

- Identify the regulatory gold standards, including MSB registration and AML protocols, required to protect your institutional financial integrity.

- Discover how to bridge the gap between digital and physical commerce using an all-in-one ecosystem of gateways and crypto POS machines.

What is Crypto to Fiat Settlement and Why It Matters in 2026

Crypto to fiat settlement is the automated process of converting digital assets from a customer transaction into traditional currency and depositing it directly into a corporate bank account. While early adopters historically focused on holding assets for long-term appreciation, 2026 represents a fundamental shift toward utility. Global commerce now utilizes blockchain as a high-speed payment rail rather than a speculative instrument. This transition allows enterprises to tap into a $3 trillion global market while maintaining their existing accounting standards and functional currency.

Modern technology has effectively solved the price fluctuation problem that once deterred traditional retailers. By leveraging a professional Cryptocurrency Exchange infrastructure, payment gateways now offer Instant conversion at the point of sale. This ensures that the value of a transaction remains fixed from the moment the customer pays until the funds reach the merchant’s ledger. It’s a secure bridge that connects decentralized innovation with institutional financial reliability.

The Evolution of Merchant Settlement

The industry has matured from manual exchange transfers to automated, API-driven gateway settlements. Settlement latency is the time delay between a customer’s payment and the availability of funds in the merchant’s bank account, which can severely restrict operational liquidity if not managed through real-time conversion. Modern providers now handle the heavy lifting by absorbing volatility risk during the transaction window. This evolution ensures that a business receives the exact fiat amount listed on its invoice, regardless of market movements during the crypto to fiat settlement process.

Key Benefits for Modern Enterprises

Enterprises adopting a crypto to fiat settlement strategy gain immediate competitive advantages over those relying solely on legacy systems. One primary benefit is the total elimination of chargeback fraud, a problem that continues to cost global merchants billions annually in traditional credit card processing. Additionally, blockchain-based settlements significantly lower cross-border fees when compared to the 50-year-old SWIFT banking network. This efficiency is particularly attractive for businesses targeting high-net-worth individuals. Sectors like luxury real estate and international hotels are already using these tools to provide seamless experiences for a growing demographic of crypto-affluent travelers who demand modern payment flexibility.

The Mechanics: How Crypto-to-Fiat Conversion Works

The transition from a customer’s digital wallet to a merchant’s bank account involves a sophisticated backend process that removes technical friction. When a transaction initiates, the payment gateway captures the current market price and freezes it for a specific window, typically lasting 15 to 20 minutes. This ensures the crypto to fiat settlement remains consistent even if the market fluctuates seconds later. By locking these rates, businesses avoid the risk of receiving less value than the sticker price of their goods or services, effectively neutralizing the 10% to 15% intraday swings common in digital assets.

Behind the scenes, the gateway communicates with deep liquidity pools to execute the exchange. This is essential for high-volume trades where a lack of depth could lead to price slippage. As highlighted by payment experts in the whitepaper Crypto Payments: From Virtuality to Real Use Case, the move toward practical merchant adoption relies on these robust settlement layers that bridge decentralized finance with traditional banking.

The Gateway vs. The Liquidity Provider

The gateway serves as the professional interface, while the liquidity provider acts as the financial engine. Automated market makers (AMMs) and over-the-counter (OTC) desks provide the necessary fiat depth to handle large-scale enterprise transactions without delay. These entities work in tandem to ensure that even a million-dollar transaction doesn’t disrupt the market price. In high-volume settlement, the spread between the buy and sell price is more important than the commission fee because it directly impacts the final net amount received.

API Integration and Automated Workflows

Modern businesses scale by removing manual steps from their financial operations. Using payment APIs allows companies to embed this technology directly into their existing infrastructure. For ecommerce platforms, this means crypto to fiat settlement happens automatically the moment a purchase is confirmed.

Merchants can set “Auto-Settlement” rules to convert incoming assets into their preferred local currency instantly. All activity is tracked through a comprehensive merchant dashboard crypto, providing real-time reporting and financial clarity. This level of automation turns a complex technological hurdle into a standard business process. To see how this fits your business model, you can review the benefits of a dedicated fiat settlement solution.

Comparing Settlement Methods: Instant vs. Batch vs. Stablecoin

Selecting a settlement strategy is a critical decision for any enterprise integrating digital assets. The right choice balances speed against operational costs. A business’s ability to manage a crypto to fiat settlement determines its overall exposure to market shifts. Organizations typically choose between three primary models based on their liquidity needs and transaction volume.

- Instant Settlement: This method converts digital assets at the exact point of sale. It eliminates price risk by locking in the exchange rate immediately. The merchant receives the precise fiat value displayed at checkout, regardless of market movements ten minutes later.

- Batch Settlement: This approach consolidates daily transactions into a single transfer. It is a strategic choice for high-volume retail environments. By aggregating 500 individual sales into one daily settlement, businesses reduce recurring bank transfer fees by up to 90%.

- Stablecoin Settlement: Many global firms choose USDT or USDC as their primary rail. This allows them to keep funds in a digital format that is pegged to the dollar, providing the speed of blockchain with the stability of fiat.

- Direct to Bank Model: This handles the final mile of the process. It ensures that converted funds reach local bank accounts through established financial networks, bypassing the traditional 3 to 5 day wait associated with international wires.

Same-Day Settlement vs. Traditional T+2

Traditional banking systems rely on T+2 or T+3 settlement cycles. These legacy delays often trap capital for 48 to 72 hours. Modern fiat settlement products bypass these hurdles by utilizing blockchain’s 24/7/365 availability. While a traditional bank closes on Friday afternoon, blockchain rails continue to move value. This means weekend revenue is available for use on Monday morning rather than Wednesday. It’s a fundamental shift that provides businesses with superior cash flow management and immediate access to working capital.

The Stablecoin Bridge Strategy

High-volume entities often require rapid transitions between digital and physical liquidity. In major financial hubs, selling USDT for cash dubai has become a standard procedure for managing large-scale B2B payouts. This strategy is efficient for companies that need to pay international suppliers without waiting for slow SWIFT transfers. Stablecoins offer a level of transparency that traditional bank statements don’t provide. Every transaction is recorded on a public ledger, allowing for real-time audits. This transparency simplifies the crypto to fiat settlement process, as every dollar equivalent is accounted for on-chain before it ever hits a local bank account.

By choosing the correct settlement rhythm, a business doesn’t just accept payments; it optimizes its entire financial operation. Pallapay acts as the professional bridge, ensuring these technical processes remain invisible to the end user while providing the merchant with absolute stability.

Evaluating a Settlement Provider: Compliance and Security

Selecting a partner for crypto to fiat settlement requires a rigorous audit of their legal standing and operational integrity. MSB (Money Services Business) registration represents the non-negotiable gold standard for institutional reliability. These licenses ensure the provider operates under strict financial oversight, which protects your capital from the inherent risks of unregulated markets. KYC (Know Your Customer) and AML (Anti-Money Laundering) protocols aren’t merely administrative hurdles; they’re essential defense mechanisms for your brand. By verifying every participant in the transaction chain, providers prevent illicit funds from entering your ecosystem, shielding your business from the 2024 surge in global regulatory enforcement actions.

Fee transparency separates global fintech leaders from opaque startups. You’ll typically encounter two primary models: flat transaction fees and percentage spreads. A flat fee provides predictable costs for high-volume operations, whereas percentage spreads can often mask the true cost of liquidity. It’s vital to demand clear security disclosures regarding the conversion window. Top-tier providers use deep liquidity pools to lock in rates the moment a transaction initiates, ensuring that the price you see is the price you receive without slippage.

- Regulatory Standing: Verify active MSB status in Tier-1 jurisdictions.

- Risk Mitigation: Ensure robust AML screening is integrated into the API.

- Cost Clarity: Compare the total cost of ownership between flat and spread-based models.

- Fund Protection: Review the provider’s custody and insurance protocols during the settlement gap.

Navigating Global Regulations

US and Canadian MSB registrations serve as a hallmark of trust for global enterprises, ensuring compliance with the latest 2023 FATF standards. Businesses operating in retail stores must prioritize regulated partners to ensure long-term operational continuity and avoid bank account closures. Regulatory Arbitrage is the risky practice of selecting jurisdictions with weak oversight to bypass compliance; businesses should avoid it to prevent sudden asset freezes or legal liability. Professional providers bridge the gap between blockchain innovation and institutional finance.

The Strategic Implementation Guide

Consulting a crypto pos machine for business helps brick-and-mortar setups align their physical hardware with digital settlement speeds. Your chosen infrastructure must scale to handle peak volumes, such as the 40% increase in transaction density often recorded during global retail events. Reliable providers maintain a local presence in major financial hubs to offer real-time support and localized expertise. This ensures the future of payments remains a standard, effortless part of your daily operations.

Secure your revenue stream and eliminate market risk by integrating our instant fiat settlement solution today.

The Pallapay Advantage: An All-in-One Settlement Ecosystem

Pallapay operates as a sophisticated bridge between disruptive blockchain technology and institutional financial reliability. The platform provides a unified environment where digital payment gateways link directly with physical crypto pos machines to ensure a frictionless experience for every stakeholder. By maintaining regulated operations in the USA, Canada, and the UAE, Pallapay offers a secure framework that supports global expansion without the compliance hurdles typically associated with digital assets. It’s a system built for scale and stability.

Liquidity remains the most critical factor in any crypto to fiat settlement strategy. Pallapay addresses this through a hybrid network of automated online systems and physical OTC desks. This infrastructure ensures that whether a business is processing a small retail transaction or a multi-million dollar corporate transfer, the funds are available when needed. The ecosystem currently serves a diverse range of industries, providing specialized support for gaming platforms, high-end retail, and international hospitality groups.

Bridging Physical and Digital Commerce

Modern merchants need the ability to accept crypto in store without waiting days for bank clearances. Pallapay enables businesses to receive digital payments and complete a crypto to fiat settlement within the same hour. This rapid turnaround protects profit margins from market swings. For immediate access to capital, the Pallapay Mastercard allows merchants to spend their settled fiat funds at millions of locations worldwide. Large-scale corporate entities often require more personalized service, which is where the otc crypto exchange comes into play. These desks facilitate high-volume trades with deep liquidity, ensuring that institutional moves don’t suffer from price slippage or execution delays.

The Future of Payments is Instant

Pallapay removes the heavy lifting of complex technology for non-technical merchants. You don’t need to be a blockchain expert to modernize your payment stack. By consolidating the gateway, POS hardware, and fiat settlement into a single partnership, Pallapay eliminates the fragmentation that slows down business growth. This all-in-one approach provides a clear audit trail and a simplified user experience. It’s not just about adding a new payment method; it’s about evolving with the global economy. The future of payments is instant, secure, and professional. Optimize your business with Pallapay’s fiat settlement solutions today and secure your place in the new financial era.

Future-Proof Your Global Commerce Strategy

The financial landscape of 2026 demands a transition from traditional barriers to frictionless liquidity. High-growth merchants are moving away from legacy batch processing in favor of real-time efficiency to maintain a competitive edge. Mastering crypto to fiat settlement isn’t just a technical upgrade; it’s a strategic necessity for capturing global market share. Success requires a partner that bridges the gap between digital innovation and institutional reliability.

Pallapay provides this bridge as a regulated MSB in both the USA and Canada. By leveraging an official MSB registration and a robust global OTC presence, businesses can access instant settlement across 180+ countries. This infrastructure eliminates the volatility risks typically associated with digital assets while ensuring full compliance with international standards. It’s time to integrate a solution that treats complex conversions as standard business operations.

Scale your business with Pallapay’s professional fiat settlement solutions and secure your position in the future of payments. The tools for your global expansion are ready when you are.

Frequently Asked Questions

How long does crypto to fiat settlement take?

Crypto to fiat settlement occurs instantly or within 24 hours depending on your chosen payout method. Pallapay processes these transactions in real-time to eliminate the risk of market fluctuations. While traditional bank transfers might take 1 to 3 business days, our internal ecosystem ensures liquidity is available immediately. This speed allows your business to maintain a steady cash flow without waiting for legacy banking cycles.

Is crypto to fiat settlement taxable for my business?

Tax obligations for your transactions depend on your specific jurisdiction and local tax laws. In regions like the UAE, corporate tax rates of 9% apply to businesses exceeding certain profit thresholds as of June 2023. You should consult with a certified financial advisor to ensure compliance with VAT and income reporting requirements. We provide detailed transaction logs to simplify your accounting and audit processes.

Can I receive settlement in my local currency like AED, USD, or EUR?

You can receive settlements in over 30 global currencies including AED, USD, and EUR. Our platform bridges the gap between digital assets and traditional finance by providing direct conversion into your preferred local tender. This flexibility ensures you avoid unnecessary exchange fees and can pay your local suppliers or employees without friction. It’s a key feature for businesses looking to scale internationally.

What are the fees associated with crypto to fiat conversion?

Fees for conversion are calculated based on your monthly transaction volume and the specific digital assets being processed. We prioritize transparency by displaying all costs before you finalize a transaction. This approach prevents hidden charges from impacting your profit margins. By using a professional gateway, you access institutional liquidity rates that are typically more favorable than standard retail exchanges.

Do I need a special bank account to receive fiat settlements?

You don’t need a specialized crypto bank account to receive your funds. Pallapay facilitates transfers directly to your existing corporate or personal bank account via standard SEPA or SWIFT protocols. This integration makes the transition from blockchain technology to traditional banking feel like a standard business operation. It ensures your current financial infrastructure remains compatible with the future of payments.

Is it possible to settle payments in stablecoins instead of fiat?

Businesses can choose to settle their transactions in stablecoins such as USDT or USDC to maintain digital liquidity. This option provides the stability of fiat currencies while retaining the speed and low cost of blockchain transfers. It’s an ideal solution for companies that operate globally and want to avoid the delays of the traditional banking system. You can switch between fiat and stablecoin settlements within your dashboard settings.

How does a crypto payment gateway handle price volatility during a sale?

Our gateway handles price volatility by locking the exchange rate at the exact moment of the transaction. This ensures the merchant receives the precise fiat amount regardless of market shifts that occur seconds later. By providing an instant crypto to fiat settlement, we remove the financial risk associated with digital asset price swings. This mechanism protects your revenue and provides the stability needed for predictable financial planning.

What documents are required for a business to start using fiat settlement?

Businesses must provide a valid trade license, proof of address, and identification for all beneficial owners to begin using the service. These requirements comply with global Anti-Money Laundering standards and the 2018 FATF recommendations for virtual asset service providers. Once your documentation is verified, your account is activated for full settlement capabilities. This rigorous onboarding process establishes the trust and security required for institutional financial operations.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.

Leave a Reply