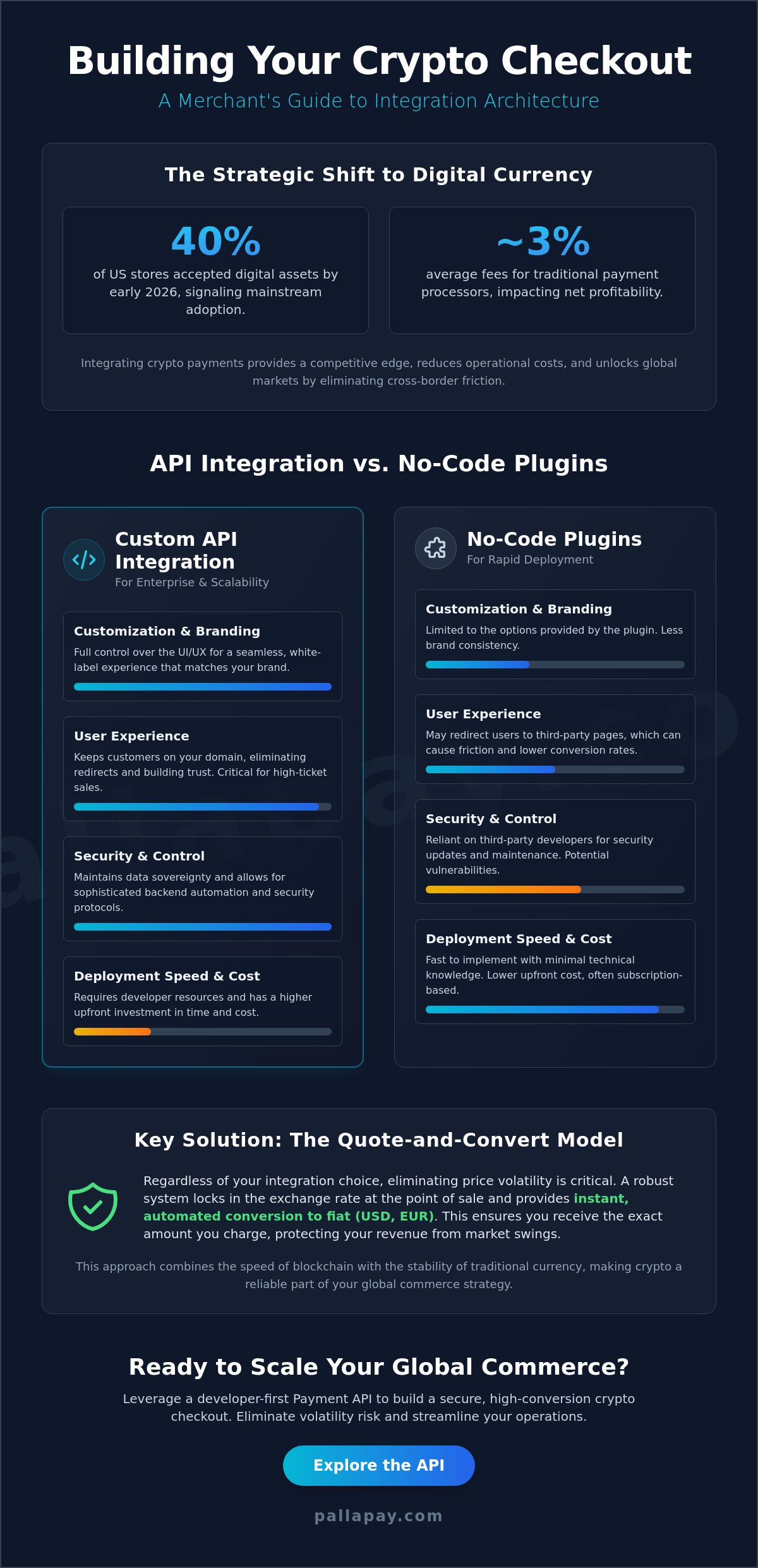

By 2026, the traditional multi-day settlement window for global markets has become an obsolete relic of a slower financial era. As you monitor the latest crypto payment trends 2026, it’s evident that the friction of moving capital between digital assets and commodity trading is finally disappearing. You’ve likely felt the frustration of slow execution and security concerns in high-leverage environments, where legacy banking rails often fail to match the speed of your professional strategy.

This article explores how the convergence of digital assets and institutional finance is revolutionizing your access to XAUUSD and USD CFD markets. You’ll discover how to utilize instant fiat-to-crypto-to-trade settlement tools to capture market movements without unnecessary delays. We will examine the synergy between crypto liquidity and CFD trading, providing a clear roadmap for leveraging gold to achieve financial independence. By understanding these high-speed liquidity rails, you can transform complex technical conversions into standard, effortless operations that accelerate your path to growth.

Key Takeaways

- Understand how the latest crypto payment trends 2026 are shifting the role of digital assets from speculative holdings to high-speed settlement layers for global markets.

- Access Gold (XAUUSD) and USD CFD trading instantly by utilizing crypto payment gateways that remove traditional settlement delays.

- Explore the path to financial sovereignty by transitioning from a passive crypto holder to a strategic market participant in the high-leverage CFD arena.

- Protect your capital by identifying the 2026 security standards, ranging from AI-driven fraud defense to the use of MSB-registered providers.

- Streamline your trading floor operations by integrating professional payment APIs that connect your crypto portfolio directly to global Forex markets.

The 2026 Convergence: Crypto Payment Rails and Global Forex Markets

The financial architecture of 2026 represents a total unification of decentralized technology and traditional market structures. Digital wallets no longer exist as isolated storage for speculative tokens; they’ve become the primary interface for global currency exchanges. As you analyze the crypto payment trends 2026, the most significant shift is the transition of Cryptocurrency from a volatile asset class into a high-performance settlement layer for international trade. For professional traders and modern brokerage firms, this evolution provides a critical solution to the historical friction of cross-border capital movement.

Stablecoins, particularly USDT, now serve as the foundational base for Forex and CFD trading. With the World Economic Forum reporting that stablecoin transaction volume exceeded $34 trillion in 2025, these digital assets provide the stability required to enter volatile currency pairs without the delays of traditional wire transfers. By using crypto payment rails, traders can move from a digital balance to a live XAUUSD or USD position in seconds. This speed isn’t just a convenience; it’s a strategic necessity for capturing alpha in a market that never sleeps.

The Death of T+2 Settlement

Traditional banking systems have long relied on the T+2 settlement cycle, forcing traders to wait 48 hours for funds to clear. Blockchain technology has effectively dismantled this delay, replacing it with instant trade execution. When liquidity moves in real-time, the natural result is a narrowing of spreads across the Forex market, as brokers no longer need to price in the risk of settlement lag. Instant settlement removes the window of uncertainty between trade execution and finality, effectively eliminating counterparty risk in 2026. This efficiency allows you to reallocate capital across different asset classes, such as gold or major currency pairs, with zero downtime.

ISO 20022 and Crypto Standardization

The bridge between disruptive innovation and institutional reliability is built on the ISO 20022 messaging standard. This global protocol allows crypto gateways to communicate seamlessly with traditional banking infrastructures, ensuring that your digital transactions meet the same rigorous data standards as legacy wire transfers. Trading safety now depends on choosing partners that prioritize these standards. Working with a provider that maintains Pallapay MSB compliance and security ensures your capital is handled within a regulated framework. In 2026, the distinction between a “crypto company” and a “financial institution” has vanished, replaced by a new class of MSB-registered fintech leaders who provide the professional bridge for modern commerce.

Real-Time Liquidity: Revolutionizing Gold (XAUUSD) and USD CFD Trading

Real-time liquidity is the pulse of the 2026 market. As you observe the crypto payment trends 2026, the most striking development is the “Invisible Funding” model. This trend describes the seamless integration of payment APIs directly into trading platforms, allowing you to move capital from a digital wallet to a high-leverage CFD account without ever leaving the trading interface. This agility is essential for navigating the volatility of USD CFDs, where market sentiment can shift in milliseconds. By removing the friction of manual deposits, you can respond to global economic data as it breaks, ensuring your capital is always positioned where it’s most productive.

Gold (XAUUSD) remains the ultimate hedge in this digital-first economy, but the way it’s accessed has fundamentally changed. Professional traders now leverage crypto payment gateways to fund their gold positions, using digital assets as the high-speed rail to reach traditional safe havens. The International Monetary Fund has highlighted the importance of global crypto regulation to stabilize these cross-border flows, creating a secure environment where digital liquidity meets physical-backed assets. This regulatory maturity allows you to trade with the confidence that your settlement layers are as robust as the commodities you’re trading.

The Allure of XAUUSD in a Digital Age

Digital-native investors are flocking to gold CFDs in 2026 because they offer a familiar volatility profile within a regulated framework. Many use USDT as a stable gateway to acquire physical-backed digital gold, allowing them to hedge against currency devaluation without the storage costs of bullion. It’s a strategic move toward financial sovereignty that combines the permanence of gold with the speed of blockchain. Generally, a strengthening USD creates tactical shorting opportunities for gold CFDs, while a weakening dollar invites long-term accumulation strategies.

Leveraging USD CFD Volatility

Traders use leverage to amplify small movements in major USD pairs, turning minor pips into significant gains. Success in this high-stakes environment depends entirely on the speed of your off-ramp and settlement. If you can’t realize your gains instantly, you’re exposed to unnecessary market risk. Utilizing professional tools to Explore Pallapay Fiat Settlement for traders allows you to capture short-term fluctuations and convert them into stable fiat balances immediately. This level of control is what separates institutional-grade trading from retail speculation. If you’re looking to optimize your capital flow, consider how an integrated settlement solution can enhance your current trading strategy.

The Transformative Potential of Professional CFD Trading

Professional CFD trading in 2026 has evolved into a sophisticated tool for individual financial sovereignty. It’s no longer just about speculative gains; it’s about utilizing high-performance liquidity to build a resilient financial base. As you analyze the crypto payment trends 2026, you’ll see a clear shift in how traders interact with global markets. The friction of moving capital between digital wallets and brokerage accounts has vanished, allowing you to focus entirely on market strategy rather than procedural delays. This era is defined by the psychological shift from being a passive “crypto holder”—waiting for a single asset to rise—to a strategic market participant who navigates global volatility with precision.

In 2026, individual financial trajectories are being rewritten by those who leverage the power of compound returns in leveraged gold and currency markets. By utilizing digital assets as a high-speed settlement layer, traders can enter and exit positions in XAUUSD or major USD pairs with institutional efficiency. This access democratizes the wealth-building tools once reserved for hedge funds, providing a professional bridge to financial independence. The ability to capture small price movements and amplify them through leverage creates a sense of momentum that can accelerate a business or personal portfolio’s progress in real-time.

Building a Financial Legacy through Strategic Trading

Strategic CFD trading allows you to profit in both rising and falling markets, a critical advantage in the dynamic economy of 2026. Whether the USD is strengthening or gold is entering a corrective phase, professional tools ensure you aren’t sidelined by market direction. Success in this environment requires a disciplined approach to risk management and a commitment to continuous education. When you master these elements, the “trading lifestyle”—characterized by freedom, mobility, and a digital-first income—becomes a practical reality. You’re no longer tethered to local economic cycles; instead, you’re participating in a unified global ecosystem that rewards agility and foresight.

Bridging the Wealth Gap with High-Performance Tools

The democratization of gateway technology has made it possible for traders to spend their gains instantly, closing the loop between digital profit and real-world utility. High-performance tools like the Pallapay Mastercard allow you to connect your trading profits directly to everyday commerce without the need for traditional banking intermediaries. This integration ensures that your financial growth isn’t just a number on a screen but a tangible asset that supports your lifestyle. The shift from local currency dependence to global asset trading marks the beginning of true financial independence for the modern trader. By adopting these solutions, you can handle complex background processes effortlessly, allowing you to stay focused on the next strategic move in the XAUUSD market.

Regulatory and Security Trends: Protecting the Modern Trader

Security is no longer an afterthought for the high-volume trader; it’s the invisible shield that enables aggressive market participation. One of the dominant crypto payment trends 2026 is the shift toward perpetual KYC (Know Your Customer) systems. These aren’t static, one-time checks. They’re dynamic, real-time verification layers that ensure liquidity remains clean without interrupting your trade flow. Research indicates that 77% of financial firms have prioritized AI compliance in 2026 to mitigate risks in high-leverage CFD environments. This technology doesn’t just block bad actors. It protects your capital from the contagion of market manipulation, ensuring that the XAUUSD and USD pairs you trade are backed by legitimate liquidity.

Trading with an MSB-registered provider is the non-negotiable standard for professional participants. For example, Pallapay maintains active registrations as a Money Services Business with FinCEN in the United States and FINTRAC in Canada. These credentials prove that the bridge between your digital assets and the Forex market is built on institutional-grade reliability. When your deposit and withdrawal APIs are secured by audited smart contracts, you eliminate the technical vulnerabilities that once plagued early crypto adopters. Zero-Knowledge identity verification further enhances this by allowing you to prove your eligibility to trade without exposing sensitive personal data to the open web.

AI vs. AI: The Battle for Payment Security

Platforms now employ advanced neural networks to monitor for anomalies in real-time. This “AI vs. AI” battle ensures that automated fraud attempts are neutralized before they can impact your gold positions. Digital ID wallets have also evolved into essential tools, acting as a single, secure source of truth for your trading credentials across multiple platforms. You can Secure your assets with the Pallapay Wallet to ensure your liquidity is always ready for the next market move. This integration makes complex technical conversions feel like standard, effortless business operations.

Navigating Global Compliance

Professional traders increasingly migrate toward platforms with multi-jurisdictional registrations to ensure absolute legal clarity. Clear regulatory frameworks, such as the EU’s MiCA framework which reached its full authorization deadline in July 2026, provide the stability required for long-term financial planning. Transparent fee structures further build trust, ensuring that your compound returns aren’t eroded by hidden costs. This regulatory clarity is the primary driver of the 2026 crypto-Forex boom, transforming a once-frontier market into a stable destination for global wealth. If you’re ready to trade with institutional security, you can integrate the Pallapay Payment API for your trading operations today.

Maximizing the 2026 Trends with Pallapay’s Ecosystem

Pallapay functions as the definitive destination for traders seeking to capitalize on the crypto payment trends 2026. It provides the professional bridge between your digital asset portfolio and the high-liquidity world of global Forex markets. By removing the traditional barriers to entry, the ecosystem allows you to move capital with the confidence of a global industry leader. Integrating the Pallapay Payment API ensures that your trading floor operations remain seamless; it provides real-time technical conversions that feel like standard business operations. This integration is designed to empower the user, making complex background processes invisible so you can focus entirely on market analysis and execution.

The year 2026 marks a pivotal transition in financial strategy. Passive holding is no longer the most efficient way to grow wealth in a market defined by rapid fluctuations and instant liquidity. By shifting toward active, strategic trading in gold and USD CFDs, you can capture momentum that was previously inaccessible to retail participants. The Pallapay ecosystem supports this evolution by offering a full-circle utility. Gains from a successful gold trade can be transitioned into daily spending or reinvested into new market opportunities without the friction of legacy banking delays. This creates a sense of momentum, suggesting that by adopting these solutions, your business can accelerate its own progress in real-time.

The Ultimate Off-Ramp for Successful Traders

Capturing profit is only half of the professional trading equation; the other half is the ability to realize those gains. Converting trading profits back to fiat is an effortless process when you utilize Pallapay Off-Ramp services. For high-volume gold and currency traders, the convenience of an OTC desk provides the necessary depth of liquidity to handle large-scale transactions without market slippage. You can consult the Institutional OTC Guide for High-Volume Traders to understand how professional desks facilitate these complex background processes. This ensures that your financial transformation is supported by a reliable, institutional-grade infrastructure that prioritizes your security.

Your Strategic Partner in Financial Evolution

Pallapay’s global presence supports professional traders in 180+ countries, ensuring that your strategy is never limited by geography or local banking constraints. The future of gold trading is here, and it’s characterized by instant execution, absolute security, and high liquidity. As the convergence of digital assets and traditional markets reaches its peak, having a forward-thinking strategic partner is essential for maintaining a competitive edge. You’ve seen how the financial landscape has changed; now it’s time to take control of your own trajectory. Start your journey toward financial transformation and experience the power of a unified trading ecosystem today.

Mastering the Future of Global Liquidity

The financial landscape has fundamentally shifted. We’ve explored how digital assets now serve as the high-speed settlement layer for professional Forex and CFD markets, replacing legacy delays with real-time execution. By embracing crypto payment trends 2026, you’ve moved beyond passive holding into a world of strategic market participation. This evolution ensures that your capital is always liquid, enabling you to capture volatility in Gold and USD pairs with institutional precision. The synergy between crypto liquidity and commodity trading is no longer a future concept; it’s the current standard for financial sovereignty.

Success in this era requires a partner that bridges disruptive innovation with institutional reliability. Pallapay provides this foundation as a regulated MSB in both the USA and Canada, serving professional traders in over 180 countries. With institutional-grade OTC and POS infrastructure, the ecosystem handles complex technical conversions effortlessly, allowing you to focus on your market edge. It’s time to take control of your financial trajectory and leverage the tools designed for the modern economy. Elevate your trading strategy with Pallapay’s high-speed crypto payment solutions and transform your approach to the global markets. Your journey toward lasting financial independence is backed by the world’s most advanced liquidity rails.

Frequently Asked Questions

What are the dominant crypto payment trends for 2026?

The dominant crypto payment trends 2026 focus on the normalization of digital assets as high-speed settlement layers rather than speculative holdings. Stablecoins now account for over $34 trillion in transaction volume, providing the primary liquidity rail for international trade. Businesses are prioritizing reliability and compliance, embedding crypto infrastructure directly into existing payment systems to ensure technical conversions feel like standard, effortless operations that accelerate global commerce.

How does CFD trading in gold (XAUUSD) work with crypto payments?

Trading Gold (XAUUSD) with crypto payments works by using a secure gateway to fund high-leverage CFD accounts in real-time. You transfer digital assets like USDT to your broker, which is instantly settled into a trading balance. This method bypasses the traditional T+2 settlement cycle, allowing you to capture market movements in the gold market with institutional agility. It’s a professional bridge between digital liquidity and physical-backed commodity assets.

Can I fund my Forex trading account using USDT in 2026?

You can fund your Forex trading account using USDT as the primary liquidity source in 2026. Stablecoins have become the foundational base for modern brokerage firms because they offer a stable value for volatile market entries. This approach removes the friction of cross-border wire transfers, ensuring your capital is ready for USD CFD opportunities the moment market conditions are favorable. It is the definitive method for high-speed capital allocation.

Is it safe to use a crypto payment gateway for high-volume CFD trades?

Using a crypto payment gateway for high-volume CFD trades is highly secure when you partner with an MSB-registered provider. Regulatory frameworks like the EU’s MiCA ensure that firms operate under strict authorization. Audit-verified smart contracts and AI-driven fraud defense protect your deposits from technical vulnerabilities. Choosing a global industry leader ensures your high-leverage positions are backed by a secure, institutional-grade infrastructure that prioritizes absolute capital safety and stability.

What is the advantage of trading USD CFDs over traditional Forex?

The primary advantage of trading USD CFDs is the ability to utilize leverage to amplify small movements in major currency pairs. Traditional Forex often requires larger capital outlays for significant returns, but CFDs allow for strategic market participation with greater capital efficiency. You can profit from both rising and falling markets, providing a versatile tool for building a resilient financial base in a dynamic global economy that rewards agility.

How can I instantly convert my trading profits from crypto to fiat?

You can instantly convert your trading profits by utilizing professional off-ramp services or crypto-to-bank transfer APIs. These tools allow you to move gains from your trading balance back into a liquid fiat account or a digital wallet immediately. Capturing profit is only effective if you can realize it without delay. This seamless integration ensures your financial growth is a tangible asset that supports your real-world utility and long-term lifestyle goals.

Why is MSB registration important for crypto payment providers in 2026?

MSB registration is critical because it ensures your provider operates under the legal oversight of agencies like FinCEN in the United States or FINTRAC in Canada. In 2026, regulatory clarity is the primary driver of market trust. Trading with a registered entity protects you from the risks associated with unregulated shadow banking. It provides a professional guarantee that your settlement layers meet rigorous anti-money laundering and institutional security standards.

What role does AI play in securing crypto-to-Forex transactions?

AI plays a decisive role by providing real-time fraud detection and monitoring for market manipulation across crypto-to-Forex transactions. Advanced neural networks analyze transaction patterns to neutralize threats before they impact user wallets. Additionally, AI-powered perpetual KYC systems ensure that identity verification is continuous and non-disruptive. This technology creates a secure environment where high-speed liquidity can flow without exposing participants to the risks of traditional financial friction or operational delays.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.