By 2026, over 45% of global merchants are projected to adopt a crypto POS machine for business, signaling a definitive shift toward a digital-first economy. You’ve likely noticed that traditional banking infrastructure feels increasingly sluggish. High transaction fees and multi-day settlement windows often act as a drag on your operational agility, especially when you’re trying to move capital across borders or into high-growth markets.

This guide reveals how a crypto POS terminal does more than just process payments. It transforms your retail checkout into a high-performance gateway for CFD trading and global liquidity. You’ll learn how to leverage instant payment verification and seamless fiat conversion to bridge the gap between daily revenue and institutional-grade investment. We’ll examine the mechanics of using business capital to access advanced markets, specifically focusing on the transformative potential of Gold and USD CFD trading to redefine your financial trajectory.

Key Takeaways

- Modernize your retail infrastructure by bypassing traditional banking rails to eliminate high transaction fees and slow settlement times.

- Ensure enterprise-grade security with PCI DSS compliant terminals that utilize rapid QR and NFC protocols for instant payment verification.

- Integrate a crypto pos machine for business to bridge the gap between daily retail sales and sophisticated global liquidity markets.

- Accelerate your financial growth by converting idle revenue into active trading capital for high-performance markets like Gold (XAU/USD) and Forex CFDs.

- Streamline operational reporting through advanced APIs that connect your digital asset inflows directly to existing ERP systems for real-time oversight.

The Evolution of Retail: Why Your Business Needs a Crypto POS Machine in 2026

In 2026, the retail environment has undergone a fundamental transformation where digital assets have moved from speculative holdings to a standard consumer expectation. Businesses that don’t adapt risk losing a segment that controls a $1.5 trillion market. A crypto pos machine for business is a regulated terminal that bridges blockchain assets with traditional business accounting. This integration allows retail stores to capture high-net-worth customers who prefer the efficiency of digital wallets over plastic cards. By adopting this technology, you aren’t just accepting a new currency; you’re upgrading your entire financial operating system to meet modern demands.

Defining the 2026 Digital Payment Landscape

Stablecoins like USDT have become the preferred medium for retail settlement because they provide the stability of the US Dollar with the speed of blockchain. Retailers require instant verification to maintain momentum on the sales floor, and modern terminals deliver this by confirming transactions in seconds rather than days. This technology effectively solves the friction of cross-border consumer spending. International tourists no longer need to visit physical exchange desks when they can pay directly from their digital wallets, ensuring your business remains their first choice for luxury and essential purchases alike.

Solving Traditional Payment Friction

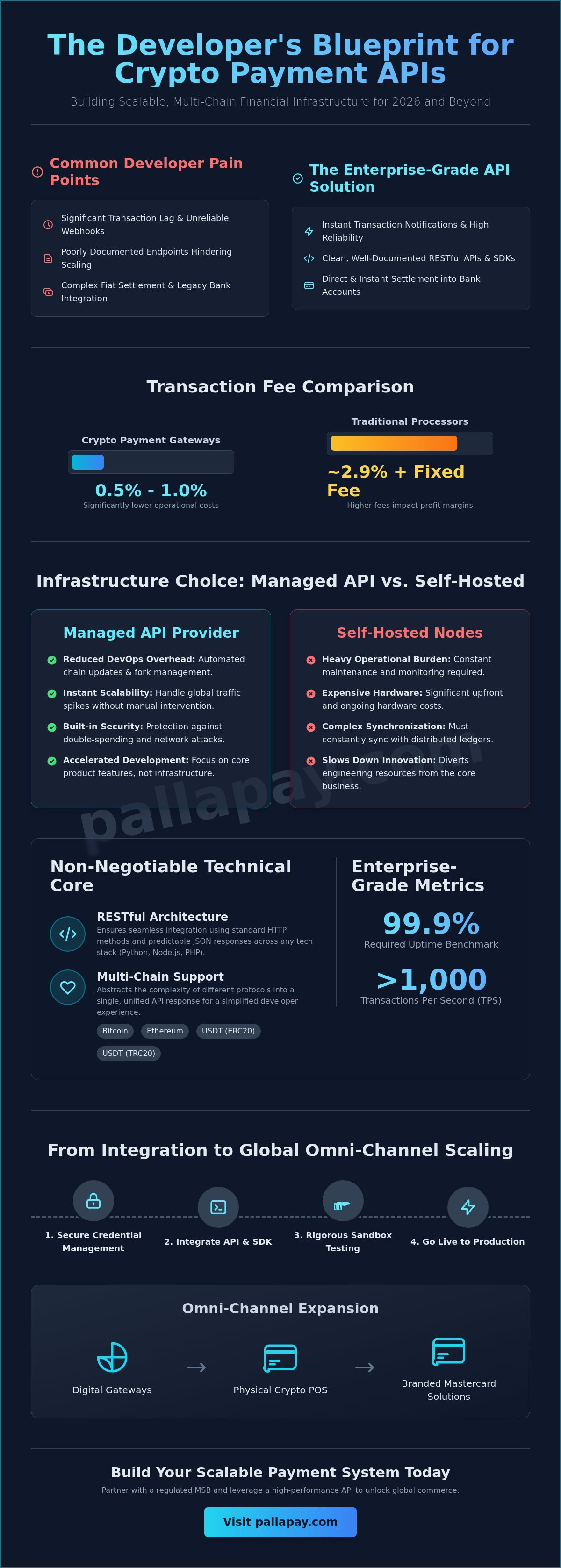

Legacy credit card processing is becoming a significant operational liability for growth-oriented firms. Traditional systems often charge fees exceeding 3.5% and hold your capital for multi-day settlement periods. In contrast, using a crypto pos machine for business reduces these costs to a range of 0.5% to 1.5% per sale. By utilizing a Cryptocurrency exchange integration, businesses can settle funds instantly, bypassing the web of intermediary banks that typically drain profit margins.

Blockchain technology also provides a definitive solution to chargeback fraud. Because these transactions are irreversible, the risk of “friendly fraud” is eliminated, saving merchants the $25 to $100 fees typically associated with traditional payment disputes. This security allows you to focus on strategic growth rather than administrative recovery. The efficiency gained here is more than just a cost-saving measure; it’s the first step in a broader financial evolution. By capturing revenue in digital form, you’re positioned to immediately enter high-performance markets like Gold (XAU/USD) and Forex CFDs. This shift from merchant to strategic trader can fundamentally change an individual’s financial life, turning daily sales into a springboard for global wealth management.

How Modern Crypto Terminals Function: Security, Speed, and Compliance

The checkout experience in 2026 demands a level of technical sophistication that traditional card readers simply can’t match. A crypto pos machine for business operates through a seamless interface where customers choose between scanning a dynamic QR code or using NFC-enabled wallets. This isn’t just about convenience; it’s about a hardened security layer that protects both the merchant and the consumer. Every transaction uses end-to-end encryption and meets current PCI DSS standards, ensuring that sensitive data remains isolated from the public ledger while maintaining institutional-grade safety.

Real-Time Blockchain Verification

The terminal communicates with a centralized gateway to verify network confirmations in milliseconds. In high-volume environments, this speed is vital for moving from ‘pending’ to ‘settled’ status without disrupting the customer queue. Managing multiple assets like Bitcoin, Ethereum, or USDT happens through one unified interface, where real-time liquidity management prevents slippage. This ensures the price at the moment of the scan is exactly what the merchant receives in value. When evaluating the Pros and Cons of Accepting Cryptocurrency, the benefit of instant, secure settlement often outweighs the initial learning curve for staff. This precision allows you to manage your cash flow with the same accuracy as a professional trading floor.

Institutional Reliability and MSB Compliance

Merchant trust rests on regulatory foundations rather than just technical promises. A professional terminal isn’t just a piece of hardware; it’s an extension of a regulated financial institution. MSB (Money Services Business) registration in the US and Canada is a non-negotiable requirement that protects your business from legal exposure and financial instability. These registrations ensure that the provider follows strict AML and KYC standards, which are essential for maintaining a global reputation. This rigorous oversight happens in the background, so your checkout line never slows down. By choosing a partner with these credentials, you’re securing a bridge to advanced financial markets. Learn more about our secure fiat settlement options to see how we protect your capital during the conversion process.

Securing your retail revenue is the primary step in a larger financial strategy. Once your capital is verified and settled, it becomes a liquid asset ready for immediate deployment. This reliability allows you to transition seamlessly into the world of CFD trading. Whether you’re targeting the stability of Gold (XAU/USD) or the high-volume movements of major currency pairs, a secure POS system provides the consistent cash flow needed to fund a professional trading account. This integration can change an individual’s financial life by turning standard business earnings into a high-growth investment portfolio. You don’t just accept payments; you’re building a foundation for institutional-grade wealth management.

Beyond the Transaction: Leveraging Crypto POS Revenue for CFD and Gold Trading

Traditional retail models often treat the point of sale as the conclusion of a financial journey. In contrast, a crypto pos machine for business serves as a high-performance starting point for sophisticated capital management. While legacy systems leave your daily takings in stagnant bank accounts, an integrated terminal allows you to deploy revenue into growth-oriented markets immediately. This shift turns your checkout counter into a strategic hub where retail inflows become active trading capital, providing a level of financial flexibility that was previously reserved for institutional players.

XAU/USD trading can hedge a business against fiat currency inflation by providing a stable alternative to fluctuating national currencies. By capturing revenue in digital assets, you’re positioned to move capital directly into the markets without the friction of multiple bank transfers. This unified approach ensures that your business capital is always working, whether it’s facilitating a sale or capturing a market movement. For a technical deep dive into the hardware that enables this, consult our sibling guide on the Crypto POS Machine: The Complete Guide for Merchants in 2026.

The Power of Gold and USD CFDs

Gold (XAU) has long been the definitive store of value for businesses looking to protect their reserves. Trading Gold CFDs allows you to benefit from price movements without the logistical burden of physical storage, ensuring your business maintains high liquidity. Similarly, USD CFD trading provides the necessary volatility and volume to scale your capital rapidly. This transition from simple merchant to active market participant has the power to change an individual’s financial life. It moves you beyond the linear growth of retail sales and into the exponential potential of global finance, where strategic leverage can amplify your business success.

The Integrated Pallapay Advantage

The synergy within a professional ecosystem is what makes this strategy viable for busy entrepreneurs. You can move funds from the Pallapay Wallet to high-stakes trading accounts in seconds, ensuring you don’t miss critical market entries. Utilizing real-time market data allows you to time your fiat conversions perfectly, maximizing the value of every transaction processed through your crypto pos machine for business. This isn’t just about accepting payments; it’s about building a comprehensive financial engine that supports both daily operations and long-term wealth accumulation. By integrating these processes, you’re not just running a store; you’re managing a global portfolio from your retail floor.

Operational Integration: Fiat Settlement, APIs, and Reporting

Operational integration is the bridge between a successful sale and institutional-grade financial management. A crypto pos machine for business functions as more than a simple card reader; it acts as an intelligent node within your company’s broader ERP framework. By customizing your settlement schedule, you can choose between instant, daily, or weekly options to align with your specific cash flow requirements. This flexibility ensures that capital is never trapped in the system when it could be deployed elsewhere. Explore our Payment API for custom business integrations to see how real-time data flows from the terminal directly into your accounting software, simplifying tax compliance and inventory management.

Seamless Fiat Settlement and Off-Ramping

Businesses operating in the global economy need the ability to off-ramp crypto to bank accounts with minimal friction. This capability allows international retail brands to manage multi-currency accounts without the typical delays associated with legacy banking. Receiving local currency directly into your account helps you avoid exchange rate volatility, preserving the value of your retail revenue. This stable foundation is essential before you transition into more active financial roles, such as using your settled funds for Gold (XAU) or USD CFD trading. Efficient off-ramping ensures that your business capital is always liquid and ready for any market opportunity.

Tailored Solutions for Specific Industries

Different sectors require unique approaches to digital asset adoption to maintain a competitive edge. For example, hotels are increasingly adopting these terminals to cater to international guests who demand modern payment options. In a retail store, touch-screen terminals optimize floor operations by providing a familiar interface for staff while handling complex blockchain verifications in the background. Meanwhile, ecommerce entities are scaling through hybrid systems that unify online and offline revenue streams. This integrated approach ensures that every transaction contributes to a singular, powerful financial ecosystem.

By centralizing your reporting and settlement, you gain the clarity needed to make high-stakes financial decisions. Whether you’re looking to change your financial life through strategic Forex market entry or simply want to hedge your reserves with Gold, the data provided by your crypto pos machine for business is your most valuable asset. The transition from retail revenue to a diversified trading portfolio becomes an effortless business operation when the underlying mechanics are handled by a sophisticated partner. Secure your business growth with our advanced fiat settlement solutions today.

The Pallapay Ecosystem: A Professional Bridge to Global Financial Markets

Adopting a crypto pos machine for business is the first step in joining a unified financial engine designed for the 2026 economy. Pallapay functions as the definitive destination for professional infrastructure, where every component is engineered to work in total synergy. Your retail terminal doesn’t exist in isolation; it’s part of a comprehensive circuit that includes the Pallapay Mastercard and a high-volume OTC desk. This integration allows you to capture revenue at the point of sale and immediately transition those funds into strategic assets or operational capital without the delays inherent in legacy banking rails.

Institutional-grade security is the hallmark of this ecosystem. We provide 24/7 strategic support to ensure your transition into the digital economy is seamless and secure. By positioning your business within this integrated framework, you aren’t just reacting to market changes; you’re placing your company at the forefront of a global evolution. The speed and reliability of our infrastructure mean that your capital is always liquid, ready to be deployed into high-performance markets the moment an opportunity arises.

Global Reliability and Institutional Trust

Success in the modern market requires a partner with a truly global reach. Leveraging a presence in 180+ countries allows your business to expand its horizons with confidence. Our MSB registrations in the US and Canada provide the peace of mind that comes from working with a regulated, transparent entity. This institutional trust is vital for merchants who handle significant volumes and require absolute stability in their financial partners. To understand the technical safeguards protecting your revenue, consult our guide on Crypto Security in 2026: The Definitive Guide.

Getting Started with Pallapay POS

The application process for modern merchants is streamlined to ensure you can begin accepting digital assets quickly. We offer diverse hardware options, ranging from portable handhelds for mobile service to integrated countertop units for high-traffic retail environments. Once your terminal is active, you gain access to our full suite of financial tools. This includes everything from branded gift cards to professional trading desks.

The ability to move from a retail transaction to a Gold (XAU/USD) trading position within minutes can fundamentally change an individual’s financial life. It transforms the nature of business ownership from simple commerce to sophisticated wealth management. By utilizing USD CFD trading to scale your retail revenue, you’re building a future that isn’t limited by local currency fluctuations. This ecosystem provides the professional bridge you need to turn daily business operations into a gateway for global financial growth.

Securing Your Place in the Future of Global Commerce

Adopting a crypto pos machine for business is more than a technical upgrade; it’s a strategic move that aligns your retail operations with the global financial evolution. You’ve seen how this technology eliminates traditional banking friction, provides instant fiat settlement, and opens a direct gateway to the transformative potential of Gold and USD CFD trading. By leveraging a regulated MSB partner with registrations in the US and Canada, you ensure that every transaction is backed by institutional-grade security and reliability.

The ability to convert daily sales into active trading capital can fundamentally change your financial life. It allows you to move beyond linear retail growth and participate in high-liquidity markets that protect your reserves against inflation. The integration of payments, APIs, and trading desks creates a singular engine for wealth management. Empower your business with the Pallapay Crypto POS ecosystem today. Your journey toward an integrated financial future starts with a single, secure transaction.

Frequently Asked Questions

Can a crypto POS machine convert payments to fiat instantly?

Yes, a professional crypto pos machine for business facilitates the instant conversion of digital assets into fiat currency at the point of sale. This process ensures that you receive the exact value of the transaction in your local currency, effectively removing any exposure to market fluctuations. It’s a critical feature for maintaining stable accounting practices while offering customers the modern flexibility they expect in 2026.

How much are the transaction fees for a crypto POS terminal compared to credit cards?

Transaction fees for crypto terminals are significantly lower, typically ranging from 0.5% to 1.5% per sale. In contrast, traditional credit card processing fees often exceed 3.5% once all intermediary costs are included. By reducing these operational expenses, your business can retain more profit from every transaction. Additionally, blockchain payments eliminate the risk of chargeback fees, which can cost merchants between $25 and $100 per dispute.

Is a crypto POS machine for business legally compliant in 2026?

A crypto pos machine for business is entirely legally compliant when managed through a regulated financial provider. Compliance is maintained through official MSB registrations in the US and Canada, ensuring that all AML and KYC standards are strictly followed. Working with a registered partner protects your business from legal risks and provides a secure foundation for international expansion across more than 180 countries.

What cryptocurrencies can my business accept through a crypto POS?

You can accept a wide range of digital assets, including Bitcoin, Ethereum, and stablecoins like USDT. Most modern terminals are designed to handle multiple coin types through a single interface, making it easy for your staff to process diverse payments. This versatility allows you to cater to a global audience of high-net-worth consumers who prefer different blockchain networks for their retail spending.

How does a crypto POS terminal handle market volatility during a transaction?

Terminals handle volatility by using real-time liquidity management to lock in the exchange rate at the exact moment of the transaction. The customer pays the current market value in crypto, and the merchant receives the equivalent fiat amount without slippage. This instant settlement mechanism ensures that the price displayed on the screen is the final value settled into your business account, regardless of market shifts.

Can I use the revenue from my crypto POS for Forex and Gold trading?

Yes, you can deploy your retail revenue directly into Forex and Gold (XAU/USD) trading accounts through an integrated ecosystem. This strategic advantage allows you to turn stagnant cash flow into active trading capital, providing a hedge against fiat inflation. Moving funds from your POS settlement into a trading account is an effortless operation that can fundamentally change an individual’s financial life by diversifying their wealth.

What hardware is required to start accepting crypto in my retail store?

Starting requires a dedicated handheld or countertop terminal, though some businesses opt for API-based integrations with their existing ERP systems. These devices are designed for retail environments, featuring touch screens and built-in printers for receipts. The hardware is user-friendly and connects seamlessly to your digital wallet, allowing you to manage payments and trading activities from a single, sophisticated hub.

Does a crypto POS require a constant internet connection to function?

A constant internet connection is necessary to verify blockchain transactions and communicate with the payment gateway in real-time. This connectivity ensures that funds are confirmed and settled instantly on the network. Most terminals use Wi-Fi or cellular data to maintain a secure link, providing the speed and reliability needed for high-volume retail environments where every second counts at the checkout counter.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.