Did you know that stablecoin on-chain transfer volumes reached approximately $36 trillion by 2025, surpassing the total transaction volumes of legacy giants like Mastercard and American Express? You’ve likely felt the daily friction of traditional banking, where high cross-border fees and the persistent threat of chargeback fraud eat into your margins. Building a robust business case for accepting crypto payments is no longer about following a trend. It’s about securing a strategic advantage in a globalized economy that demands speed and absolute security.

You deserve a financial infrastructure that works as fast as your business does. We’ll show you how integrating cryptocurrency payments drives revenue, eliminates chargeback fraud, and opens your doors to a high-net-worth audience of over 560 million global users. This guide provides a clear look at how modern payment gateways allow you to bypass slow settlement times and access global markets without currency hurdles. We’ll examine the operational shift toward instant fiat conversion and the regulatory frameworks that have turned digital assets into a reliable, institutional-grade tool for growth.

Key Takeaways

- Understand why legacy T+3 settlement cycles are no longer competitive and how to transition your operations toward real-time financial liquidity.

- Build a compelling business case for accepting crypto payments by comparing standard credit card fees against the efficiency of high-performance blockchain rails.

- Expand your reach into emerging global markets and connect with a high-net-worth customer base that values borderless, friction-free transactions.

- Master the strategies for mitigating market volatility through instant fiat conversion and navigating the evolving 2026 regulatory landscape.

- Explore the technical integration of sophisticated payment APIs and physical POS machines to unify your digital and in-person sales channels effortlessly.

The Strategic Shift: Why Businesses Are Prioritizing Crypto in 2026

By 2026, the global financial landscape has matured beyond the era of speculative volatility. Digital assets have transitioned from experimental novelties into essential utility-driven tools for modern commerce. This shift is driven by a fundamental breakdown in legacy banking infrastructure. Traditional T+3 settlement cycles, which keep merchant capital locked for days, are no longer viable in a high-velocity market. Businesses now demand real-time liquidity to maintain their competitive edge. In this environment, the borderless merchant has emerged, using decentralized technology to bypass the geographic and operational silos of traditional finance.

Digital assets now serve as a sophisticated bridge between disparate fiat systems. Instead of navigating a web of intermediary banks and high cross-border fees, companies use blockchain rails to move value instantly across continents. To understand what is cryptocurrency in a 2026 context, one must look past the code and see a high-performance payment rail. It provides a standardized layer for value exchange that operates independently of local banking hours or clearinghouse delays.

The Death of the “Wait-and-See” Approach

Institutional adoption is no longer a future prediction; it’s a current reality. With global crypto users exceeding 560 million, the demographic of digital asset holders is too large to ignore. A 2026 market analysis shows that 85% of merchants now view these payments as a primary vehicle for reaching tech-savvy, high-net-worth customers. Staying on the sidelines creates a measurable competitive disadvantage. If your rivals offer the speed of blockchain confirmation while you remain tethered to legacy systems, you risk losing market share to more agile competitors. The business case for accepting crypto payments is fundamentally a transition from viewing payments as a cost-center to leveraging them as a strategic profit-driver.

Stablecoins as the New Global Standard

The primary driver of merchant adoption in 2026 isn’t Bitcoin’s price action but the utility of stablecoins. Assets like USDT and USDC have become the preferred choice for commercial transactions because they combine the stability of fiat with the technical advantages of blockchain. In 2025, stablecoins supported an annual on-chain transfer volume of approximately $36 trillion. This massive liquidity pool allows businesses to price goods in familiar denominations while benefiting from instant, irreversible transactions.

Modern treasury management now relies on the ability to move in and out of positions without friction. By utilizing fiat settlement, companies can accept digital assets and receive their local currency almost immediately. This setup effectively eliminates the volatility argument. Merchants can enjoy the benefits of a global, 24-hour payment network without exposing their balance sheets to market fluctuations. It’s a secure, efficient, and highly scalable way to manage international revenue streams.

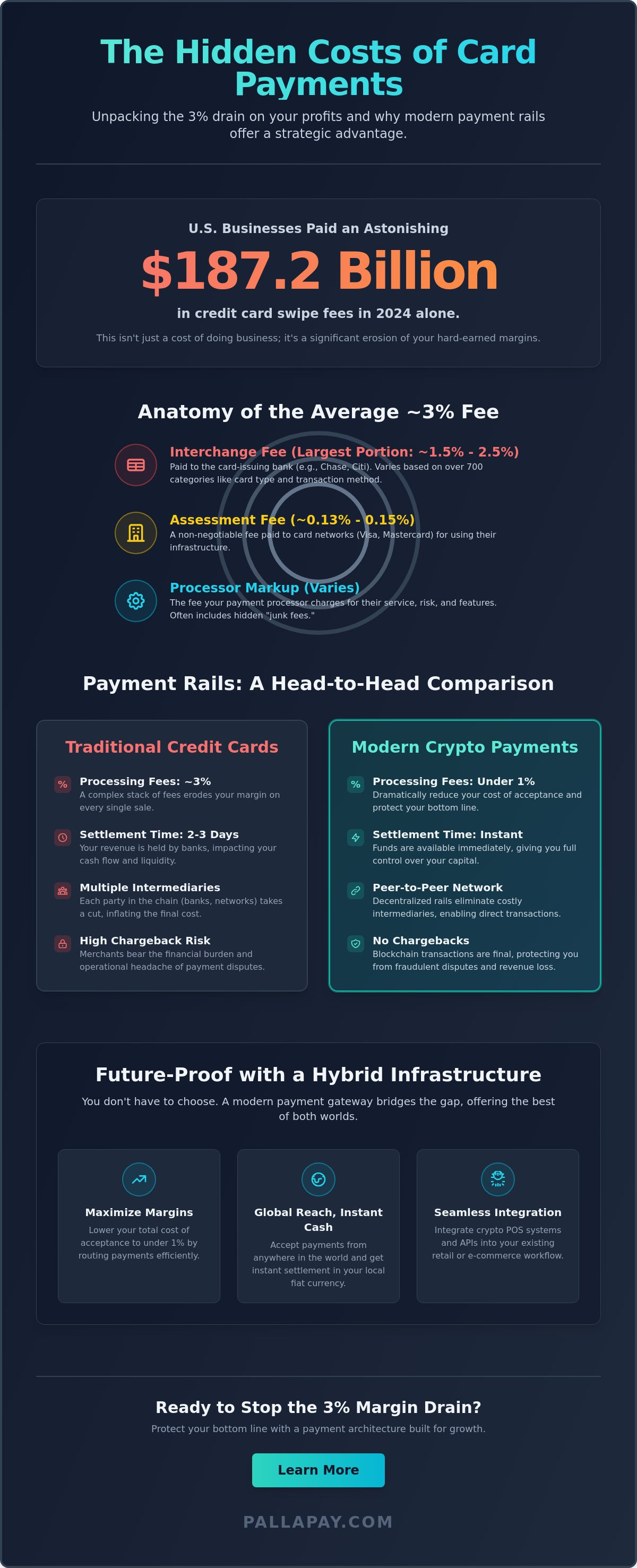

Quantifying the ROI: Transaction Efficiency and Cost Reduction

Measuring the financial impact of new technology requires a move beyond surface-level excitement. A strong business case for accepting crypto payments rests on the immediate reduction of operational overhead. Traditional merchant accounts often come with a complex web of fees that can range from 1.5% to 3.5% per transaction. In contrast, typical crypto payment gateways in 2026 operate with fees between 0.5% and 1%. For high-volume enterprises, this 2% delta represents a significant recovery of net profit that would otherwise be lost to legacy processing networks.

The savings extend into the removal of hidden costs associated with traditional banking. Intermediary banks, currency conversion spreads, and mandatory holding periods often drain resources before funds ever reach a merchant’s account. By adopting digital asset rails, businesses can expand into international markets without the need for local entities or regional bank accounts. This borderless approach allows a company to capture global demand while maintaining a centralized, efficient treasury.

The End of Chargeback Risk

One of the most immediate benefits of blockchain technology is the elimination of chargeback fraud. Credit card systems are built on “pull” mechanics, where a customer or bank can reverse a transaction weeks after a service is rendered. This creates a massive financial liability, especially for e-commerce and high-ticket retail. Cryptocurrency operates on a “push” model. Once a transaction is confirmed on the ledger, it’s permanent. This immutability protects merchants from “friendly fraud” and allows firms to redirect their fraud prevention budgets toward active growth initiatives. It’s a fundamental shift that places financial control back into the hands of the business owner.

Accelerating Cash Flow with Instant Settlement

Liquidity is the lifeblood of any scaling operation. Legacy banking systems often operate on a T+3 settlement cycle, meaning funds are locked for three business days or more. In a fast-paced economy, this delay is a significant bottleneck. Real-time payment rails provide T+0 settlement, providing almost instant access to capital. By utilizing efficient crypto to bank transfers, businesses can move their digital revenue into traditional accounts without the multi-day delays typical of the SWIFT network.

This speed enables rapid reinvestment into inventory, marketing, or payroll. Reconciliation also becomes more streamlined. Automated blockchain ledgers provide an immutable, transparent record of every transaction, reducing the administrative burden on accounting departments. For merchants looking to optimize their checkout flow, integrating a sophisticated payment API is the first step toward reclaiming lost margins and achieving true financial agility.

Capturing New Markets: Borderless Commerce and Consumer Demand

Accepting digital assets isn’t just a defensive move against transaction fees; it’s an offensive strategy to capture a share of the $3 trillion global crypto market cap. This capital represents a massive pool of liquid wealth that is increasingly seeking utility in the real-world economy. A central pillar of the business case for accepting crypto payments is the ability to reach unbanked and underbanked populations in emerging markets. These individuals may lack access to traditional credit cards or institutional banking, yet they often possess significant digital assets. By providing a gateway for these users, you open your business to entirely new demographics that were previously unreachable due to systemic financial barriers.

The B2B sector is also witnessing a major transformation through large-scale international supplier payments. Instead of waiting days for a SWIFT transfer to clear, businesses are using stablecoins to settle high-value invoices in minutes. This speed reduces the counterparty risk inherent in long settlement windows and allows for more aggressive inventory management. To build deeper engagement, sophisticated brands are launching gift card and reward programs. These initiatives allow customers to convert their digital holdings into brand-specific credit, creating a closed-loop ecosystem that encourages repeat business and enhances customer retention.

The Crypto-Native Consumer Profile

By 2026, the profile of the crypto-native consumer has evolved into a high-net-worth segment with a distinct preference for efficiency. These users typically exhibit higher average order values (AOV) compared to traditional credit card users, often due to the lack of arbitrary spending limits on blockchain transactions. For the e-commerce sector, the priority is creating a frictionless checkout experience. This involves integrating payment flows that recognize the user’s wallet instantly, allowing for a secure, one-click confirmation. When you remove the friction of manual data entry and multi-step verification, conversion rates naturally climb.

Global Expansion Without Geographic Friction

The broader business case for accepting crypto payments extends into your ability to expand operations into 180+ countries without a complex web of local bank accounts. Cryptocurrency acts as a universal financial layer, allowing you to accept payments from anywhere in the world without suffering from currency conversion loss or regional banking delays. This is a strategic advantage for the hotel industry and luxury retail, where international guests often encounter issues with credit card authorizations or high foreign transaction fees. By offering a digital payment option, you provide a premium, white-glove experience that simplifies the “last mile” of the customer journey, ensuring that your global expansion remains unhindered by geographic borders.

Mitigating Risk: Compliance, Security, and Volatility

The most common objection to digital assets is market volatility, yet this concern is largely obsolete for the modern merchant. By 2026, the business case for accepting crypto payments is reinforced by the widespread availability of instant fiat conversion. This technological bridge ensures that the merchant receives the exact fiat amount at the moment of sale, regardless of subsequent market movements. By using a sophisticated fiat settlement process, businesses can lock in exchange rates immediately, effectively removing the “volatility myth” from their operational risk profile.

Compliance is the second pillar of risk mitigation in the current landscape. Regulatory frameworks like MiCA in the European Union and the FSMA in the United Kingdom have established clear, enforceable rules for digital asset service providers. Working with a partner that adheres to these standards is essential for maintaining institutional financial reliability. Integrated gateway solutions now handle the heavy lifting of AML/KYC requirements, acting as a filter that protects the business from illicit actors while ensuring that every transaction meets global anti-money laundering standards.

Institutional-Grade Security Standards

Modern gateways handle private key management with institutional-grade rigor, removing the burden of technical custody from the merchant. This setup allows your team to focus on core operations while the underlying technology secures the assets. Multi-signature wallets have become the standard for corporate governance, requiring multiple authorizations for high-value transfers to prevent unauthorized access. Implementing crypto security best practices ensures that your digital treasury remains as secure as any traditional bank vault, providing a calm and stable environment for growth.

Regulatory Peace of Mind

Working with a regulated Money Services Business (MSB) in the US and Canada is non-negotiable for businesses that prioritize long-term stability. These entities provide the necessary oversight to ensure that your payment rails remain open and functional. Automated reporting tools now simplify the complexities of tax and compliance audits by providing a transparent, immutable record of every transaction. A crypto payment gateway serves as a compliance shield, protecting your operations from the shifting sands of global regulation and ensuring you remain on the right side of financial evolution. To secure your revenue streams and ensure absolute regulatory alignment, consider integrating a regulated settlement solution today.

Implementation: Future-Proofing with the Pallapay Ecosystem

Deploying a digital asset strategy requires a platform that bridges the gap between technical complexity and operational simplicity. The final pillar of the business case for accepting crypto payments is the ease of execution within a unified ecosystem. By using a sophisticated Payment API, you can connect your existing e-commerce storefront to global liquidity pools in a single integration. This setup allows your business to maintain its current checkout flow while adding a high-performance payment rail that settles in the currency of your choice.

Managing global operations becomes effortless through a centralized merchant dashboard. This interface provides real-time visibility into every transaction, from the initial wallet confirmation to the final fiat deposit. The transition from registration to your first crypto-to-fiat settlement is designed to be a streamlined procedural flow. Once your account is verified, you can immediately begin accepting assets like USDT or Bitcoin, with the system handling all background conversions to ensure your balance sheet remains stable and predictable.

The Omnichannel Advantage

Modern commerce isn’t limited to a single screen. To achieve true market penetration, businesses must integrate digital payments into their physical retail stores. By deploying specialized hardware like Crypto POS machines, you can accept in-person payments with the same speed and security as your online sales. This hybrid approach enables mobile payments for field services and pop-up commerce, ensuring you never miss a revenue opportunity. Synchronizing online and offline digital asset accounting within one platform eliminates the administrative burden of manual reconciliation, allowing your finance team to focus on higher-value growth initiatives.

Scaling with Professional OTC Services

As your volume grows, your infrastructure must scale accordingly. Enterprise-level merchants often require specialized handling for high-value transactions to avoid market slippage and ensure deep liquidity. Utilizing a professional OTC crypto exchange provides the necessary environment for large-scale settlements without disrupting the broader market. This service allows for customized settlement schedules that match your specific business liquidity needs, whether you require daily transfers or weekly consolidations. By partnering with a strategic facilitator that offers dedicated global support, you ensure that your transition to modern financial rails is both secure and highly efficient.

Securing Your Position in the Future of Global Commerce

The evolution of digital finance has transformed payments from a background utility into a powerful driver of organizational growth. By eliminating the friction of legacy banking and capturing the demand of over 560 million global users, you’re not just adding a payment method; you’re future-proofing your entire operational model. The business case for accepting crypto payments is built on the pillars of instant liquidity, zero chargeback fraud, and seamless cross-border expansion. These strategic advantages allow you to reclaim lost margins and scale without the geographic constraints of traditional financial systems.

Transitioning to these high-performance rails requires a partner that balances innovation with institutional reliability. As a regulated MSB in the USA and Canada, Pallapay provides the security and compliance necessary for enterprise-scale operations. We serve merchants in 180+ countries, offering instant fiat settlement in USD, EUR, and other major currencies to ensure your cash flow remains uninterrupted. Empower your business with Pallapay’s secure crypto gateway and start leveraging the efficiency of real-time commerce. Your journey toward a more agile, borderless financial future begins today.

Frequently Asked Questions

Is it legal for my business to accept cryptocurrency payments in 2026?

Accepting digital assets is legal in most major global economies, provided you comply with local financial regulations. In 2026, frameworks like the EU’s Markets in Crypto-Assets (MiCA) and the UK’s Financial Services and Markets Act provide clear guidelines for commercial use. To ensure absolute compliance, businesses should partner with a regulated Money Services Business (MSB) that is registered with authorities like FinCEN in the United States or FINTRAC in Canada.

How do I avoid the risk of Bitcoin price volatility when selling products?

You can eliminate market risk entirely by utilizing instant fiat conversion at the point of sale. Modern payment gateways lock in the exchange rate the moment a customer completes their checkout. This ensures your business receives the exact fiat amount in your preferred currency, such as USD or EUR. By converting digital assets to fiat instantly, you bypass the volatility of the underlying asset while still offering a modern payment experience.

What are the tax implications of accepting crypto for my business?

Tax authorities generally treat cryptocurrency as property or a financial asset, meaning transactions are subject to standard corporate tax and capital gains rules. It’s essential to maintain accurate records for every sale. A professional gateway simplifies this process by providing automated reporting tools and immutable ledgers for tax audits. You should always consult with a qualified tax professional to ensure your reporting aligns with current regional requirements.

Do I need a special bank account to receive fiat settlements from crypto sales?

No, you don’t need a specialized bank account to receive your funds. You can continue using your existing corporate bank account to accept fiat settlements. The gateway acts as the technical bridge, converting the customer’s digital payment into your local currency. Once the conversion is complete, the funds are transferred to your bank via standard rails, making the entire process feel like a traditional merchant settlement.

How much are the transaction fees compared to traditional credit cards?

Transaction fees for digital assets are significantly lower, typically ranging from 0.5% to 1%. Traditional credit card processing often costs merchants between 1.5% and 3.5% per transaction. Reducing these overheads is a central part of the business case for accepting crypto payments. By switching to blockchain rails, you can recover significant margins that were previously lost to intermediaries and legacy network fees.

What happens if a customer wants a refund for a crypto payment?

Refunds are handled by initiating a new “push” transaction from your merchant dashboard to the customer’s wallet address. Because blockchain transactions are irreversible, you have total control over the refund process. Most businesses calculate the refund amount based on the fiat value at the time of the original purchase. This ensures the customer receives the correct value while protecting your business from fluctuations in the asset’s market price.

Can I accept multiple cryptocurrencies like USDT, Ethereum, and Bitcoin simultaneously?

Yes, a sophisticated payment gateway allows you to accept a diverse range of assets through a single integration. You can simultaneously offer stablecoins like USDT for price stability and high-market-cap assets like Bitcoin or Ethereum for tech-savvy consumers. This flexibility ensures you don’t alienate potential customers. It also allows you to tap into the $3 trillion global market cap without managing multiple technical setups or separate wallet infrastructures.

How long does it take for the funds to reach my bank account?

While the blockchain confirmation is nearly instant, the final transfer to your bank account typically takes 24 hours. This T+1 settlement is a vast improvement over the T+3 cycles common in traditional finance. By accelerating your cash flow, you gain immediate access to capital for reinvestment. The speed of these operations mirrors the real-time nature of modern commerce, giving your business a distinct edge in liquidity management.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.