In a financial landscape where over $158 billion was lost to illicit crypto-linked activities in 2025, the difference between a high-risk gamble and a professional portfolio often comes down to a single regulatory credential. Securing an msb license crypto designation is no longer just a legal formality. It is the essential institutional bridge that connects the rapid innovation of digital assets with the reliability of global markets. You’ve likely felt the frustration of navigating a fragmented space where bridging your digital liquidity into traditional assets like Gold or USD CFDs feels unnecessarily complex and risky.

You deserve a trading environment where security is a standard feature instead of a compromise. This guide reveals how MSB-regulated frameworks provide the foundation for a total financial transformation, allowing you to move beyond simple asset swaps into sophisticated, high-volume commodity and Forex markets. We will explore the latest 2026 compliance requirements, the mechanics of secure CFD trading, and how identifying a regulated partner can accelerate your progress in the global economy.

Key Takeaways

- Understand why a verified msb license crypto is the definitive requirement for maintaining regulatory compliance and institutional trust in the 2026 digital economy.

- Discover how robust AML and KYC protocols act as a professional bridge, securing your transition from crypto liquidity into traditional fiat environments.

- Learn to unlock the transformative potential of trading by using compliant gateways to access global Forex and XAU/USD gold markets.

- Explore the mechanics of CFD and leverage trading as essential tools for achieving strategic financial growth and portfolio diversification.

- Identify the benefits of a comprehensive ecosystem that integrates OTC settlements with real-world utility through secure payment solutions.

Understanding the MSB License for Crypto Businesses in 2026

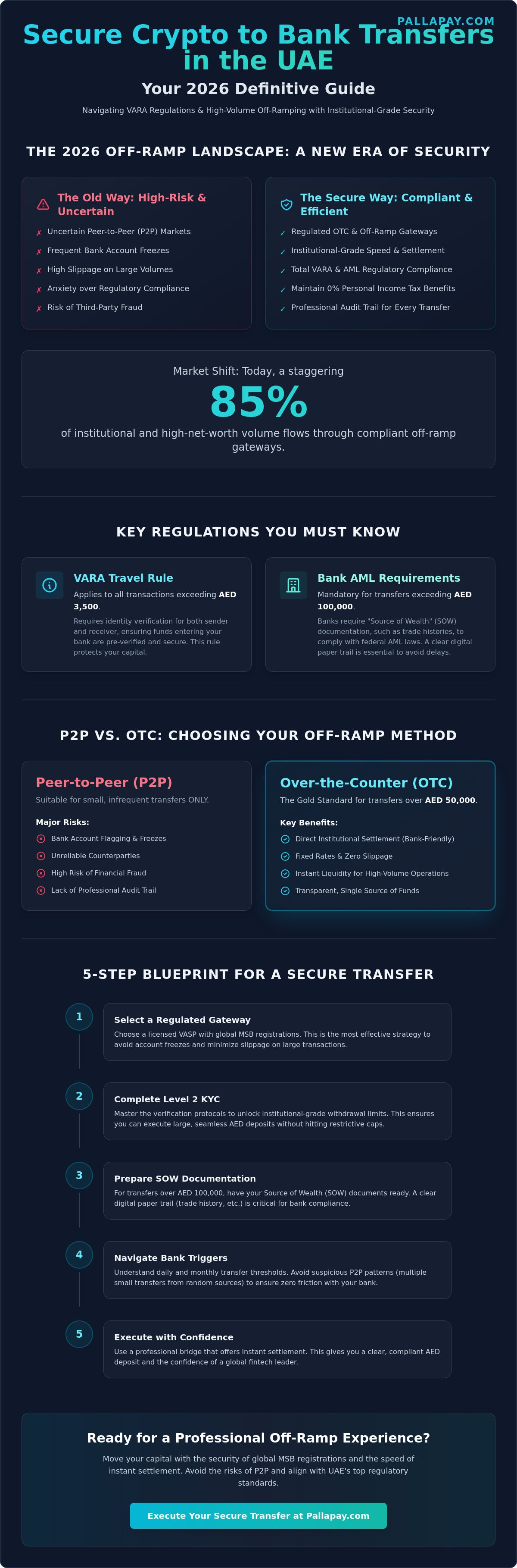

The year 2026 represents a definitive shift in how digital assets integrate with global finance. At the center of this evolution is the Money Services Business (MSB) designation. In the context of digital assets, an MSB is a financial entity that facilitates the exchange or transmission of virtual currency. For any trader looking to bridge crypto liquidity into the high-stakes world of Forex or Gold trading, an msb license crypto credential is the primary indicator of institutional reliability. It ensures that the platform isn’t just a speculative hub but a regulated gateway capable of handling high-volume fiat settlements.

Registration with federal bodies like FinCEN in the United States and FINTRAC in Canada provides a foundational layer of oversight. By 2026, global regulatory reciprocity has matured, meaning that licensed entities must adhere to standardized reporting that protects users from market volatility and platform insolvency. This status effectively separates institutional-grade ecosystems from high-risk, unregulated exchanges that often lack the liquidity or legal standing to support transformative financial operations. Choosing a licensed partner is the first step toward securing a stable financial future.

The Legal Scope of Crypto MSBs

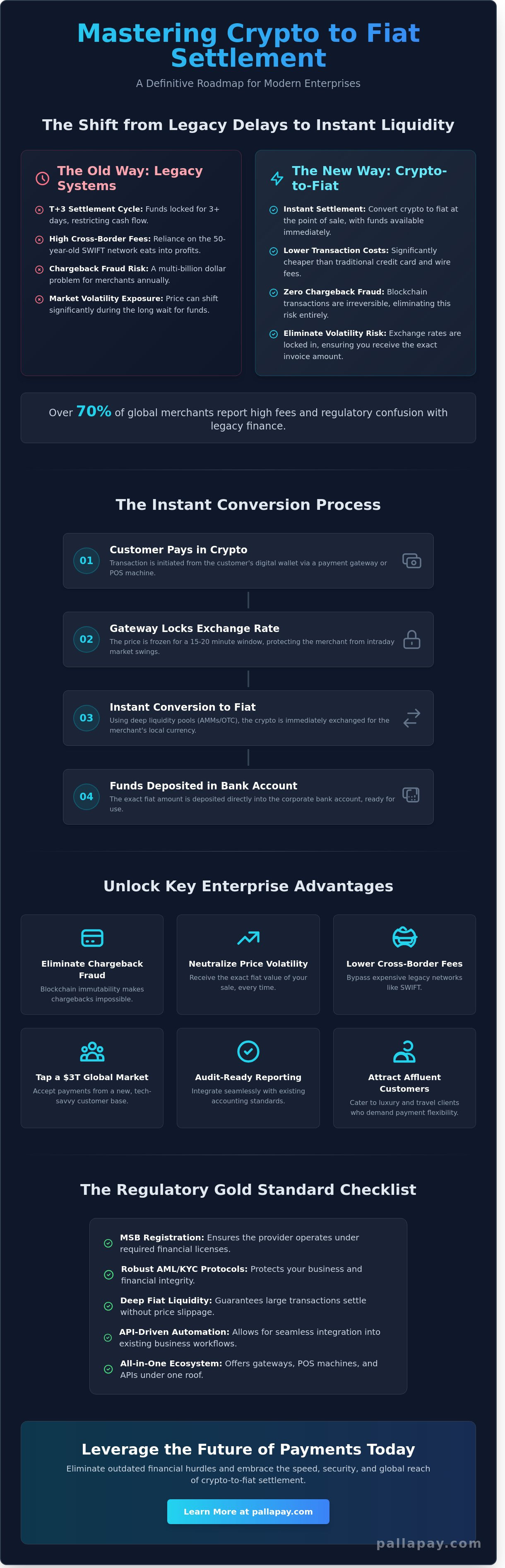

Modern regulations now distinguish clearly between simple currency exchange and complex money transmission. Under the 2026 framework, Virtual Asset Service Providers (VASPs) must operate within strict MSB boundaries to facilitate seamless crypto off-ramp services. This legal clarity is vital for traders who require instant conversion of Bitcoin or USDT into USD for CFD trading. In 2026, the MSB scope for crypto-to-fiat off-ramps specifically mandates real-time transparency and immediate liquidity provision for all registered entities, ensuring that your capital moves as fast as the markets.

FinCEN vs. State-Level Licensing

While federal registration with FinCEN is mandatory for any msb license crypto holder, it’s only one half of the security equation. State-level Money Transmitter Licenses (MTL) add a second layer of protection, often requiring specific surety bonds that vary by jurisdiction. For example, Illinois requires bonds capped at $2,000,000, while Florida’s requirement reaches up to $250,000. Having both federal and state-level credentials is the gold standard for financial reliability.

Pallapay maintains this rigorous standard through its official MSB registrations in the US and Canada. This dual compliance ensures that when you fund a Forex account or enter the XAU/USD gold markets, your capital is managed by a partner that prioritizes legal integrity as much as technological speed. This compliant structure allows you to focus on market strategy while the underlying regulatory mechanics are handled with professional precision.

The Regulatory Framework: AML, KYC, and Investor Protection

Compliance is the ultimate shield for any professional trader. With an estimated $158 billion in crypto-linked funds laundered globally in 2025, the industry’s shift toward rigorous oversight is a necessary evolution. An msb license crypto status isn’t just a badge; it’s a commitment to Anti-Money Laundering (AML) protocols that prevent illicit actors from compromising the integrity of the market. These frameworks ensure that your liquidity remains untainted by the high-stakes risks found on unlicensed platforms. By following FinCEN’s official guidance, regulated entities create a secure environment where institutional reliability meets technological innovation.

Know Your Customer (KYC) requirements often spark debates about privacy, yet in 2026, they serve as the primary balance between personal anonymity and financial safety. These protocols don’t just verify identity; they protect you from the market manipulation and fraud that led to over $1 billion in global fines during 2025. This risk is significantly mitigated when working with a provider holding an msb license crypto. The implementation of the “Travel Rule” further enhances this security by requiring the transparent sharing of information for cross-border transfers. This ensures that every high-volume move, whether funding a Forex account or settling a Gold trade, is documented and protected under international standards.

Automated Compliance Systems in 2026

Technology has transformed compliance from a bottleneck into a competitive advantage. Modern MSBs now utilize AI-driven monitoring to analyze transactions in real time, identifying suspicious patterns without slowing down legitimate trades. It’s a shift that significantly reduces friction during the onboarding process, allowing professional users to verify their accounts in minutes rather than days. As 2026 regulatory updates adjust reporting thresholds, these systems ensure that your operations remain compliant without requiring constant manual intervention.

Building Trust Through Transparency

Transparency is the only way to prove long-term solvency in the digital asset space. Leading platforms now undergo annual third-party audits to verify that their reserves match their liabilities. This level of openness is essential for anyone looking to bridge significant capital into commodity markets. Understanding the technical side of these protections is vital for any serious investor, and you can explore more about these safeguards in our guide to Crypto Security. Securely managing your capital starts with a partner that offers reliable fiat settlement services, ensuring your wealth transition is both compliant and effortless.

Why Licensed MSBs are Essential for Forex and Commodity Trading

The convergence of digital and traditional markets has created a unique opportunity for high-volume traders. By utilizing an msb license crypto provider, you can transition digital liquidity into the $7.5 trillion-a-day Forex market without the friction of traditional banking delays. This compliant infrastructure acts as a secure conduit, allowing you to fund high-leverage commodity positions while knowing your capital on-ramp is fully regulated. In a sector where “exit scams” have historically plagued unregulated CFD platforms, MSB oversight provides the institutional-grade security necessary for professional wealth building.

Oversight is the best defense against systemic risk. When you trade through a compliant gateway, you aren’t just moving numbers; you’re operating within a framework that requires segregated accounts and verified liquidity. This level of protection is vital when managing large-scale positions in Gold or USD pairs, where market volatility demands a partner that can’t simply disappear with your collateral. An msb license crypto status ensures that the platform is held to the same rigorous standards as established financial institutions, bridging the gap between innovation and reliability.

Forex Trading: The Power of USD Pairs

Trading the global USD Forex market requires precision and speed. Many traders now bridge USDT or USDC into traditional USD pairs to capitalize on 24/7 liquidity. This transformation allows you to move between volatile digital assets and the relative stability of major currency pairs in seconds. Professional traders prefer MSB-backed fiat settlement because it guarantees that their trading gains can be off-ramped into the traditional banking system without the risk of frozen accounts or compliance hurdles. It’s a strategic move that turns crypto holdings into a functional tool for global currency speculation.

Gold as a Digital Asset Hedge

Gold remains the definitive hedge against global inflation and market volatility. Trading XAU/USD CFDs using crypto-derived capital offers a sophisticated way to diversify your portfolio. Stablecoins provide a unique buffer, allowing you to lock in profits from commodity trades and preserve wealth during periods of high volatility. When your XAU/USD positions reach their target, utilizing a professional Fiat Settlement service ensures your gold profits are converted and transferred with the efficiency of a modern fintech ecosystem.

The impact of this integration on an individual’s financial life is profound. It moves the user from a speculative retail mindset into the role of a strategic asset manager. By leveraging the security of a regulated gateway, you can execute trades on the world’s most liquid assets with the same ease as a standard crypto swap. This is the essence of financial transformation: the ability to access institutional-grade markets with the agility of the digital age.

Strategic Wealth Building: Navigating CFD and Gold Markets

Transitioning from simple asset ownership to active market participation is the hallmark of a sophisticated investor. Contracts for Difference (CFDs) represent a powerful mechanism for this evolution, allowing you to speculate on the price movements of Forex and Gold without the logistical burden of physical settlement. To execute these trades with institutional-grade security, an msb license crypto provider is required to bridge your digital capital into the regulated liquidity pools of the global USD and commodity markets. This infrastructure ensures that your entry into high-leverage environments is backed by a partner that adheres to strict solvency and reporting standards.

Leverage trading in 2026 remains a double-edged sword that demands precision. While it offers the potential to amplify returns on XAU/USD and major currency pairs, it also requires a psychological shift from “HODLing” to active risk management. This is the essence of financial transformation: moving beyond the erratic cycles of crypto speculation into the structured, data-driven world of strategic commodity trading. By mixing digital assets with precious metals through an msb license crypto gateway, you create a diversified portfolio that can withstand market volatility while capitalizing on global economic shifts.

Steps to Financial Transformation

Achieving a professional trading status requires a logical, step-by-step progression. Success isn’t found in guesswork; it’s built on a foundation of secure funding and disciplined execution. Follow these core steps to begin your journey:

- Step 1: Identify a partner with a verified msb license crypto status to ensure your initial funding is compliant and protected.

- Step 2: Analyze XAU/USD and major USD trends using institutional-grade data to identify optimal market entry points.

- Step 3: Implement rigorous risk management protocols, including stop-loss orders and asset diversification, to protect your capital.

- Step 4: Utilize the Pallapay Wallet for efficient profit management and real-time access to your trading gains.

The Impact of Global Economic Shifts on Trading

In 2026, inflation and fluctuating interest rates continue to drive significant volatility in the Gold and Forex markets. CFDs are uniquely suited for this environment because they allow you to profit in both rising and falling markets. Whether the USD is strengthening or Gold is acting as a safe haven, your ability to pivot quickly is your greatest asset. Accessing real-time market data through a sophisticated Payment API ensures that your trading decisions are based on current movements rather than delayed signals. This technological edge allows you to navigate complex economic shifts with the confidence of a global industry leader.

Your path to wealth building should be as secure as it is ambitious. Start your financial transformation by integrating your digital liquidity with the world’s most stable commodity markets today.

Pallapay: Your Licensed Partner for Global Financial Evolution

Pallapay isn’t just a service provider; it’s a strategic facilitator for those seeking to bridge the gap between digital innovation and institutional reliability. By maintaining a dual msb license crypto registration in both the United States and Canada, the platform provides a secure, audited foundation for high-volume traders. This regulatory standing ensures that whether you’re converting Bitcoin for cash or funding a complex XAU/USD CFD position, your assets are managed within a framework of absolute transparency. It’s the professional answer to the operational needs of modern commerce, providing a calm and secure environment for significant capital movements.

The Pallapay ecosystem is designed to handle every stage of your financial journey. From the high-touch service of our OTC desks to the real-world utility of the Pallapay Mastercard, every feature serves the goal of institutional-grade security. We don’t just provide tools; we offer a comprehensive destination for all your technical and financial needs. This integrated approach ensures that retail and business clients alike can scale their operations without the friction typically associated with cross-market transfers. By adopting these solutions, you can accelerate your own progress in an increasingly complex global economy.

A Global Bridge for Modern Commerce

With a presence spanning over 180 countries, Pallapay prioritizes institutional-grade reliability for every user. While many platforms operate purely in the digital ether, we believe that multi-jurisdictional compliance is essential for building long-term trust. This global reach allows for seamless fiat settlement across various currency markets, ensuring that your liquidity is always where you need it. For those managing significant capital, our OTC Crypto Exchange provides the specialized liquidity and personalized service required for professional market entry.

The Future of Financial Freedom

Financial transformation is achieved when the barriers between digital assets and traditional wealth are removed. Pallapay facilitates this by providing an integrated ecosystem that includes everything from an API for Crypto Payments to secure crypto off-ramp services. This comprehensive approach empowers the next generation of global traders to move fluidly between crypto liquidity and the stability of Gold or USD Forex markets. We remain committed to continuous regulatory adaptation, ensuring that as the 2026 landscape evolves, your path to growth remains protected. The true power of a compliant msb license crypto partner lies in the peace of mind it provides, allowing you to focus entirely on the strategic execution of your trades. Embracing a compliant trading framework is the definitive step toward securing a resilient and transformative financial future.

Securing Your Position in the Global Financial Evolution

Achieving true financial transformation requires a transition from speculative digital holdings to a structured, institutional-grade strategy. We’ve explored how a verified msb license crypto status acts as the definitive bridge, allowing you to access the liquidity of global Forex and Gold markets with absolute confidence. By prioritizing compliant frameworks, you protect your capital from the inherent risks of unregulated platforms while gaining the agility to capitalize on shifting USD and XAU trends. This strategic integration is the foundation of long-term wealth building in a rapidly evolving economy.

Your journey toward professional trading excellence depends on the reliability of your underlying infrastructure. As a partner registered in the US and Canada with a presence in over 180 countries, Pallapay provides the secure environment and 24/7 professional support you need to scale your operations. It’s time to move beyond the limitations of traditional systems and embrace a more efficient, regulated future. Start your financial journey with Pallapay’s secure, MSB-regulated ecosystem today. We are here to facilitate your progress every step of the way.

Frequently Asked Questions

What is an MSB license in the cryptocurrency industry?

A Money Services Business (MSB) license is a regulatory designation for entities that facilitate the transmission or exchange of virtual currency. It classifies a crypto business as a financial institution under the Bank Secrecy Act, requiring it to implement robust AML and KYC protocols. This framework ensures that the platform operates with a high level of transparency and legal accountability in the global market.

Why is FinCEN registration important for crypto exchanges?

FinCEN registration is a mandatory federal requirement that establishes a crypto exchange as a legitimate financial entity in the United States. It requires the platform to report suspicious activities and maintain a comprehensive compliance program. This oversight is vital for protecting the broader financial system from money laundering while providing users with the assurance that they are trading on a regulated and monitored platform.

Can I trade Forex and Gold using a crypto MSB platform?

You can bridge your digital liquidity into traditional Forex and commodity markets through a regulated MSB platform. These gateways provide the necessary infrastructure to trade XAU/USD gold and USD currency pairs using CFD mechanics. This allows you to leverage your crypto holdings for strategic wealth building in the world’s most liquid markets without the delays associated with traditional banking systems.

Is an MSB license different from a banking license?

An msb license crypto designation is fundamentally different from a banking license because it focuses on the movement and exchange of value. While banks are permitted to take deposits and offer lending services, an MSB is restricted to currency transmission and conversion. This specific focus allows MSB platforms to provide more efficient, real-time settlement services that are optimized for modern digital asset trading.

How does an MSB license protect my funds during trading?

Regulated MSB status protects your funds by mandating strict adherence to international financial standards and reporting requirements. These platforms are required to maintain detailed transaction records and undergo periodic audits to ensure their operational integrity. This level of oversight acts as a safeguard against fraud and platform insolvency, providing a secure foundation for high-stakes trading in the Forex and commodity sectors.

What are the requirements for a crypto company to obtain an MSB license in 2026?

Securing an msb license crypto in 2026 involves a rigorous application process that includes federal registration and the implementation of a comprehensive AML program. Companies must also appoint a qualified compliance officer and establish automated systems for real-time transaction monitoring. Depending on the jurisdiction, businesses may also need to secure state-level money transmitter licenses and provide surety bonds to protect consumer interests.

Does Pallapay have an MSB license for its operations?

Pallapay holds official MSB registrations in both the United States and Canada, ensuring it meets the highest standards of financial compliance. This dual-registration allows the platform to offer secure OTC desks and fiat-to-crypto settlements to a global audience. By operating as a regulated entity, Pallapay provides the institutional reliability required for professional traders to manage high-volume positions across 180 countries.

How does CFD trading work with cryptocurrency liquidity?

CFD trading works by using your cryptocurrency as collateral to speculate on the price movements of assets like Gold or USD pairs. You don’t take physical delivery of the asset; instead, you profit from the price difference between the opening and closing of the trade. This method provides the transformative potential of leverage, allowing you to amplify your market exposure and achieve strategic financial growth.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.