Why let your digital assets sit idle when the XAU/USD market is moving in real-time? You’ve likely experienced the frustration of missing a perfect entry point because your capital was stuck in a slow exchange or a risky, unregulated transaction. Finding a reliable way to sell bitcoin for cash in dubai shouldn’t feel like a gamble; it should be a professional, seamless bridge to your next strategic investment.

We understand that in the high-stakes world of Forex and Gold CFDs, speed is just as critical as security. This article shows you how to transform your Bitcoin into immediate cash liquidity to capitalize on high-leverage opportunities without the typical friction of market slippage or settlement delays. You’ll discover a secure path to the global markets by partnering with an MSB-registered institution that prioritizes institutional-grade reliability and rapid execution.

Key Takeaways

- Discover how to unlock stagnant digital wealth by converting Bitcoin into active trading capital for high-potential Gold and Forex markets.

- Learn the professional OTC mechanics required to securely sell bitcoin for cash in dubai while minimizing market slippage and settlement delays.

- Understand the strategic advantages of XAU/USD CFDs, allowing you to hedge your portfolio and profit from both rising and falling price trends.

- Follow a clear, step-by-step roadmap to transition from your digital wallet to a fully funded trading account through a regulated MSB provider.

- Explore why partnering with a global leader offering services in over 180 countries provides the necessary reliability for high-volume institutional trades.

Beyond Digital Holding: Leveraging Bitcoin Liquidity for Market Participation

Bitcoin has evolved from a speculative digital experiment into a cornerstone of modern financial strategy. While many retail investors focus on long-term holding, professional traders view their holdings as dynamic capital. Stagnant assets in a digital wallet often represent missed opportunities in other high-velocity sectors. By choosing to sell bitcoin for cash in dubai, investors can transition from passive exposure to active market participation in Gold and Forex CFDs. This shift isn’t just about exiting a position; it’s about reallocating resources to markets that offer different types of leverage and structural advantages.

The Opportunity Cost of Stagnant Crypto

Holding Bitcoin during periods of consolidation often leads to significant opportunity costs. While Bitcoin’s price discovery remains a long-term play, the Forex market offers daily structured opportunities based on geopolitical events and interest rate shifts. A professional trader prioritizes Bitcoin liquidity because it allows them to pivot when global market signals demand immediate action. If a major currency pair shows a clear trend, having your capital locked in a volatile crypto asset prevents you from executing a high-conviction trade. Liquidity is the lifeblood of institutional-grade performance. Without it, you’re merely a spectator in a fast-moving global economy. Professional traders don’t wait for the market to come to them; they ensure their capital is positioned where the most significant moves are happening in real-time.

Bridging the Gap Between Crypto and Commodities

The synergy between digital assets and traditional commodities like Gold (XAU) is becoming the standard for sophisticated portfolios. Using a professional crypto off-ramp is the most efficient way to bridge this gap. Physical cash remains the preferred medium for funding high-leverage CFD accounts because it provides the most direct route to traditional brokerages and specialized trading desks. When you sell bitcoin for cash in dubai through a regulated institution, you bypass the friction of standard banking delays and avoid the slippage common on retail exchanges. This strategic move fuels long-term financial transformation by allowing you to hedge crypto volatility with the relative stability of Gold or the high-leverage potential of USD-based currency pairs. It’s about moving from a single-asset mindset to a comprehensive trading ecosystem that utilizes the best of both worlds.

Professional traders use this method to maintain a diversified edge. They recognize that while crypto offers massive growth potential, the Forex and Gold sectors provide the liquidity and depth needed for consistent, high-leverage execution. By transforming digital holdings into immediate cash, you gain the agility required to capitalize on market inefficiencies as they arise.

The Mechanics of the Off-Ramp: Selling Bitcoin for Cash Securely

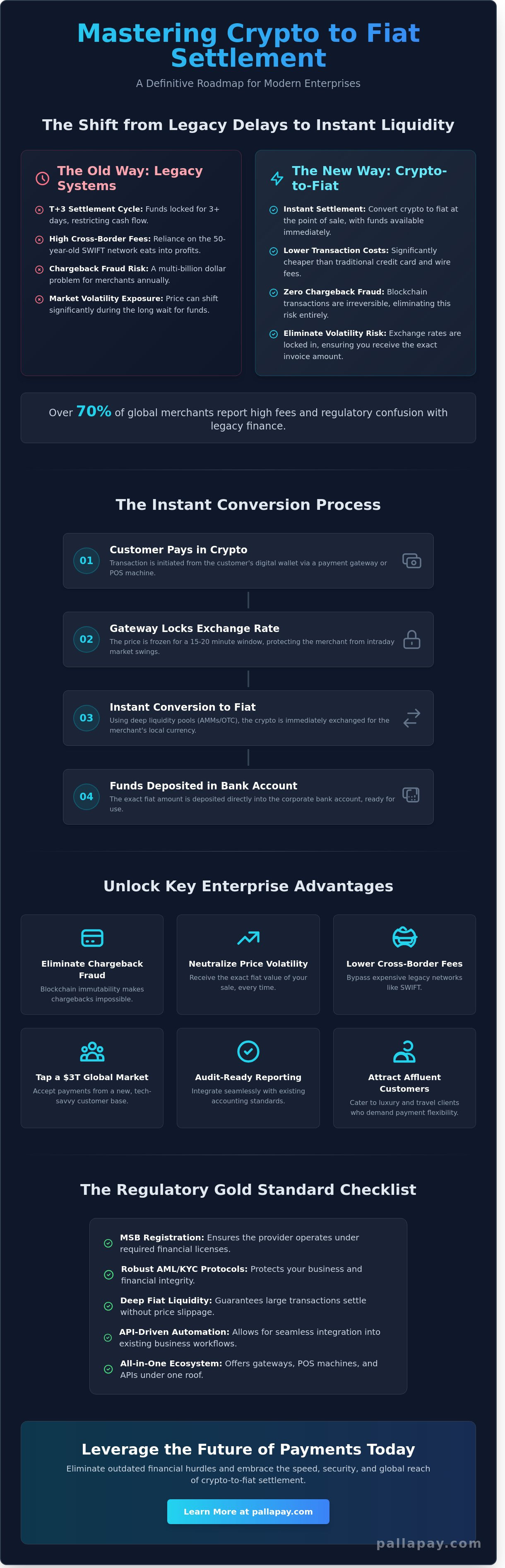

The transition from digital assets to physical liquidity requires more than just a simple transaction; it demands a structured, institutional-grade process. For traders targeting high-leverage markets, the standard online exchange often fails to provide the necessary speed and depth. This is where the Over-the-Counter (OTC) desk becomes essential. Unlike public exchanges that rely on a visible order book, an OTC desk facilitates private, direct transactions between the buyer and the service provider. This method is the preferred choice for those who need to sell bitcoin for cash in dubai without alerting the broader market or suffering from the price volatility inherent in smaller retail platforms.

The Importance of Regulatory Compliance

Security in the crypto-to-fiat space isn’t an accident; it’s the result of rigorous adherence to global financial standards. When you use a professional off-ramp, you’re engaging with a provider that holds MSB (Money Services Business) registrations in major jurisdictions like the US and Canada. This status isn’t just a label. It signifies that the institution follows strict Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols. These regulations protect your capital by ensuring every transaction is transparent and legally sound. Choosing to sell bitcoin for cash in dubai through a registered provider ensures that your digital wealth is converted into a utility-focused asset without the friction of unregulated gray-market exchanges.

OTC Desk vs. Standard Exchanges

Professional traders avoid standard exchanges for large settlements because of slippage. When a large sell order hits a public order book, it can drive the price down before the entire trade is executed, resulting in a lower final payout. A professional OTC desk eliminates this issue by offering a locked-in price for the entire volume of the trade. This efficiency is vital when your ultimate goal is to fund accounts for Gold and USD CFDs, where every dollar of initial capital counts toward your margin and leverage potential.

Transparency is another hallmark of the professional off-ramp. While retail apps often hide fees within skewed exchange rates, a dedicated OTC desk provides a clear breakdown of spreads and commissions. You know exactly what you’re paying before the transaction begins, which is crucial for maintaining precise financial records. Privacy also plays a key role in the OTC experience. High-volume traders often prefer the discretion of a physical office where they can finalize settlements in a secure environment. This process ensures that funds are available instantly, allowing for immediate reinvestment into traditional assets. If you’re looking for a streamlined way to manage your liquidity, you can explore professional OTC services to see how institutional-grade execution can improve your market entry timing.

Gold and USD CFDs: Unlocking Financial Potential Through Leverage

Transitioning from Bitcoin’s inherent volatility to the structured depth of commodities and Forex markets offers a unique strategic advantage. When you choose to sell bitcoin for cash in dubai, you aren’t simply exiting the digital ecosystem; you’re acquiring the necessary fuel for high-leverage trading. Gold (XAU) and major currency pairs like the USD provide a different risk profile and liquidity depth, allowing for more precise capital management. This shift marks a transition from being a passive holder to becoming an active market participant who can navigate diverse economic cycles with institutional-grade tools.

XAU/USD: A Cornerstone of Sophisticated Trading

Gold remains the ultimate diversifier for portfolios heavily weighted in digital assets. While Bitcoin often moves based on tech adoption and speculative sentiment, Gold reacts to inflation, interest rate shifts, and geopolitical stability. By liquidating a portion of your holdings to sell bitcoin for cash in dubai, you can enter XAU positions at key technical levels during market pullbacks. This strategy allows you to hedge against dollar weakness while maintaining the potential for capital growth. It’s a calculated move that balances the disruptive growth of crypto with the centuries-old reliability of precious metals, providing a stabilized foundation for your broader investment strategy.

The Power of Contracts for Difference (CFDs)

Contracts for Difference (CFDs) revolutionize how traders interact with global markets by providing exceptional capital efficiency. Instead of owning the underlying asset, you trade on price movements, which allows you to profit from both market rises and falls. This flexibility is essential in the Forex market, where currency values fluctuate constantly in response to global news. Leverage is the primary tool here, amplifying your trading reach so you can control larger positions with a smaller initial cash outlay. However, professional trading requires using this power responsibly. Successful execution relies on rigorous technical analysis and a disciplined approach to risk management to protect your newly acquired liquidity.

The psychological shift from “holding” to “actively trading” is where true financial transformation occurs. Holding Bitcoin involves waiting for the market to move in your favor. Trading CFDs involves making the market work for you regardless of its direction. By utilizing an institutional-grade off-ramp, you ensure that your transition from digital wealth to active trading capital is fast and secure. This agility is what separates professional traders from retail investors, providing the momentum needed to capitalize on global market signals as they happen. It’s about turning stagnant digital value into a dynamic tool for wealth generation.

Step-by-Step Guide: From Bitcoin Wallet to Trading Capital

Moving capital from the digital realm to a professional trading floor requires a methodical approach. It isn’t a casual exchange; it’s an institutional protocol designed to protect your wealth while ensuring rapid deployment. When you decide to sell bitcoin for cash in dubai, you’re initiating a sequence that prioritizes asset protection and transaction transparency. By following a structured path, you eliminate the risks associated with unregulated peer-to-peer transfers and gain the immediate liquidity needed for high-leverage market entries.

Preparing for a Professional OTC Transaction

The first step involves consolidating your assets into a secure environment. Storing your holdings in a Pallapay wallet ensures that your funds are ready for institutional-grade settlement without the delays often found on retail platforms. Before visiting the OTC desk, it’s essential to understand the current exchange spread and lock in your rate. This preparation prevents the slippage that typically erodes capital during high-volume transfers. A smooth transaction relies on clear documentation and compliance with global KYC standards, which a regulated provider will require to ensure the legality of your liquidity. Once your digital assets are verified, you can proceed to the physical settlement office to finalize the conversion in a secure, professional setting.

Immediate Deployment of Trading Capital

Securing your cash is only half the objective; the ultimate goal is market participation. Once you’ve finalized the transaction to sell bitcoin for cash in dubai, you possess the physical liquidity required to fund your Forex or Gold trading accounts. Professional traders often utilize these funds to meet margin requirements for high-leverage CFD positions. The speed of this transition is vital. In the XAU/USD market, a few hours can be the difference between catching a trend and missing it entirely.

Managing large-scale trading deposits requires a partner that understands the logistics of high-volume finance. Using Pallapay fiat settlement solutions allows you to bridge the gap between your digital profits and your traditional trading capital effortlessly. This ecosystem is built for speed, allowing you to move from a blockchain confirmation to a live trade in the shortest time possible. By treating your off-ramp as a strategic business operation, you maintain the agility needed to capitalize on global economic shifts as they happen. If you’re ready to transform your digital holdings into active market power, you can start your professional OTC exchange today and secure the liquidity your portfolio demands.

Strategic Advantage: Why Pallapay is the Professional Choice for Liquidity

Pallapay serves as the definitive destination for traders who demand more than just a simple exchange. While generic providers offer basic conversion, we provide a sophisticated ecosystem designed to support the high-velocity requirements of modern commerce. Choosing to sell bitcoin for cash in dubai through our institutional-grade OTC desks ensures you’re partnering with a global industry leader. With a presence serving over 180 countries, we offer the stability and reach necessary for large-scale financial maneuvers. Our infrastructure isn’t just about moving assets; it’s about providing the reliability required to sustain long-term growth in the competitive Gold and Forex markets. This commitment to excellence is reflected in our advanced POS solutions and secure crypto-to-fiat gateways, which are built to handle institutional volumes with ease.

Integrated Financial Solutions for Traders

Advanced trading needs require technical precision that standard retail platforms can’t provide. The Pallapay Payment API allows for seamless integration into broader financial systems, ensuring that your liquidity flows exactly where it’s needed most. As an MSB-registered provider in the US and Canada, we represent the future of global commerce by bridging the gap between disruptive tech and institutional reliability. This integrated approach allows you to leverage our entire ecosystem, from secure storage to rapid fiat settlement, as a foundation for your trading success. By adopting these solutions, a business can accelerate its own progress and maintain a competitive edge in the global marketplace. We focus on removing the friction that traditionally exists between digital holdings and traditional market participation.

Your Partner in Financial Transformation

We don’t just facilitate transactions; we empower individuals by providing unprecedented market accessibility. Our commitment to transparency ensures you receive competitive global pricing without the hidden costs associated with unregulated exchanges. When you sell bitcoin for cash in dubai with us, you’re choosing a partner that prioritizes your security and operational efficiency. We handle the complex background processes so you can focus on executing your strategy in the XAU/USD and Forex sectors. Our team is dedicated to continuous innovation, ensuring that our gateway services remain the most efficient path for digital wealth conversion.

The personality of our brand is that of a strategic facilitator, grounded in the practicalities of modern commerce while looking forward to technological advancements. We don’t position ourselves as a rebel against traditional systems, but as the professional bridge that connects established practices with modern digital assets. If you’re ready to elevate your trading capabilities and secure the liquidity your strategy demands, you can contact a Pallapay specialist today to discuss your specific high-volume requirements. Our forward-thinking approach ensures that your current tools are essential components of your inevitable financial evolution.

Bridging Digital Wealth with Global Markets

Transforming your portfolio from a passive digital holding into a dynamic trading asset is the hallmark of a sophisticated financial strategy. By choosing to sell bitcoin for cash in dubai through a regulated partner, you eliminate the friction of settlement delays and market slippage. This transition allows you to capitalize on the high-leverage opportunities found in Gold and Forex CFDs with the speed that professional markets demand.

Pallapay provides the institutional-grade OTC security necessary for high-volume transactions. As an MSB-registered entity in the USA and Canada serving clients in over 180 countries, we offer the stability and global reach required for modern capital deployment. You don’t have to navigate unregulated gray markets; you can rely on a proven fintech leader to handle your liquidity needs with professional precision. Our infrastructure is built to ensure that your move from digital assets to physical cash is seamless and secure.

The path to financial evolution is built on agility and trust. It’s time to move beyond simple holding and start leveraging your capital in the world’s most liquid markets. Secure your liquidity and start trading today with Pallapay.

Frequently Asked Questions

Is it legal to sell Bitcoin for cash through an OTC desk?

Yes, selling Bitcoin for cash is legal in Dubai when conducted through an exchange licensed by the Virtual Assets Regulatory Authority (VARA). Professional OTC desks operate within this comprehensive regulatory framework to ensure all transactions meet strict anti-money laundering and consumer protection standards. This structure provides a secure environment for both individual and institutional traders to liquidate their digital assets.

How long does the Bitcoin-to-cash exchange process take?

The exchange process is designed for immediate execution once the underlying blockchain transaction receives the necessary network confirmations. Most traders find that the entire cycle, from initiating the digital transfer to receiving physical cash, is completed within a single professional appointment. This speed is essential for those who need to act quickly on global market signals.

Why should I trade Gold CFDs instead of just holding Bitcoin?

Trading Gold CFDs provides the flexibility to profit from both rising and falling markets, which is a significant advantage over the passive “buy and hold” strategy used for Bitcoin. Gold (XAU/USD) often acts as a strategic hedge against crypto volatility. By using leverage, you can control a larger market position with less initial capital, allowing for more efficient portfolio diversification.

What is MSB registration and why does it matter for my security?

MSB stands for Money Services Business, a regulatory designation in jurisdictions like the USA and Canada that requires firms to follow rigorous financial reporting and capital security protocols. When you partner with an MSB-registered provider, you’re choosing an institution that adheres to global standards for transparency. This registration serves as a hallmark of reliability and institutional-grade safety for your funds.

Can I fund my Forex trading account directly with the cash from my sale?

Yes, once you sell bitcoin for cash in dubai, you have immediate liquidity that can be used to fund traditional brokerage accounts. Physical cash remains a highly efficient medium for making deposits into Forex or commodity trading platforms. This off-ramp process ensures that your digital profits are quickly transformed into active capital for high-leverage opportunities.

What are the fees associated with selling Bitcoin for cash?

Fees for cash settlements are typically composed of a transparent exchange spread and the standard blockchain network fee required for the transfer. Unlike retail exchanges that may have hidden costs, professional OTC desks provide a clear breakdown of the transaction value before you finalize the trade. This transparency allows you to calculate your exact trading margin with precision.

Are there limits on the amount of Bitcoin I can sell for cash in one day?

Professional OTC desks are specifically engineered to facilitate institutional-grade volumes that far exceed the daily limits found on standard retail apps. While specific caps depend on current liquidity and compliance requirements, these desks are the preferred destination for high-net-worth individuals who need to move significant capital. This capacity makes them ideal for traders funding large-scale CFD positions.

How does leverage work in Gold and USD CFD trading?

Leverage acts as a multiplier for your trading capital, allowing you to control a large position using only a small percentage of the total value as a deposit. In Gold and USD CFD trading, this means a small price movement can result in a larger profit or loss relative to your initial cash outlay. It’s a powerful tool that, when used with a disciplined risk management strategy, maximizes your market reach.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.