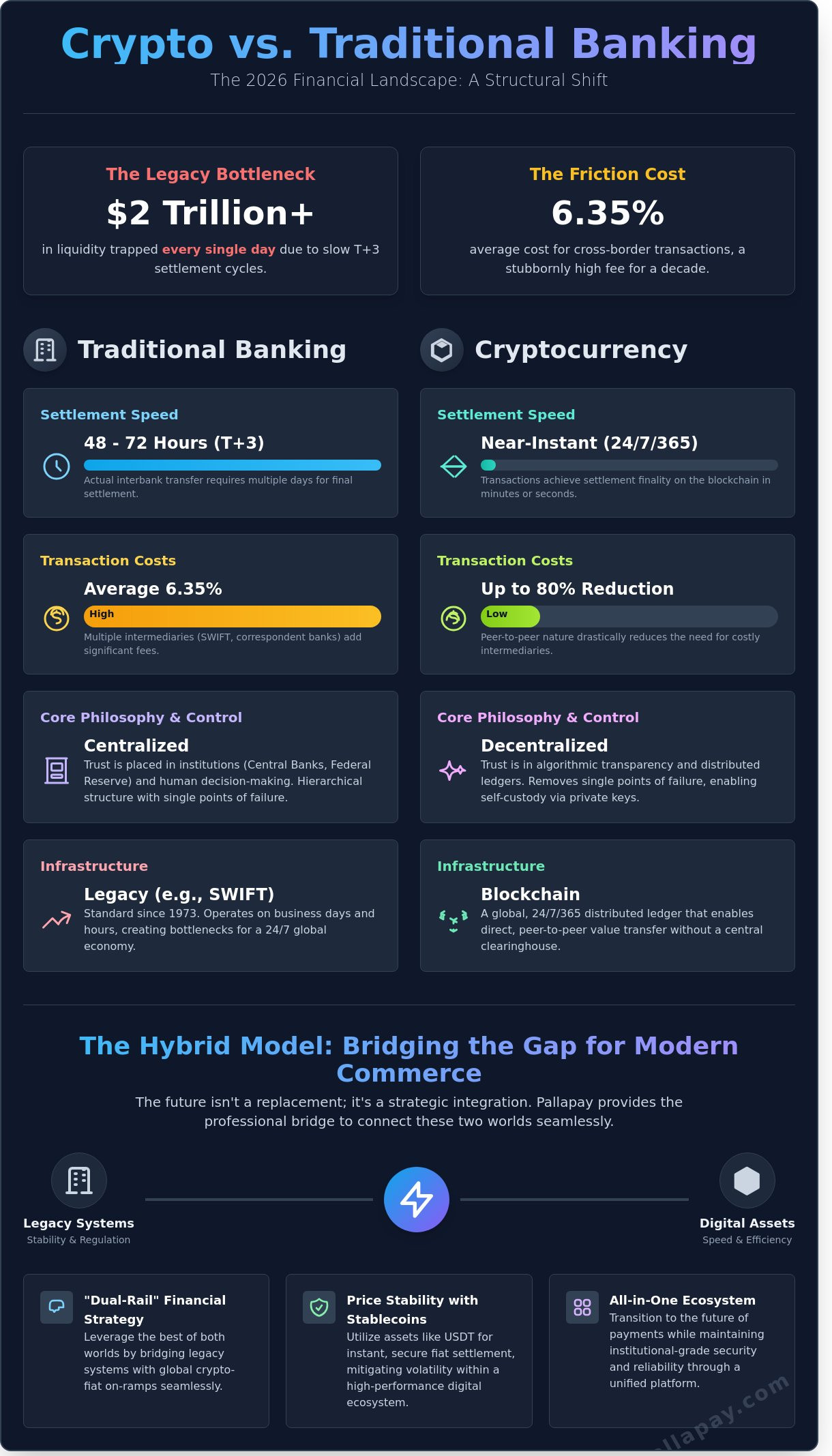

While global commerce moves at the speed of light, traditional banking remains tethered to a T+3 settlement cycle that traps over $2 trillion in liquidity every single day. This friction costs businesses an average of 6.35% in cross-border fees, a figure that has remained stubbornly high for the last decade. You’ve likely felt the frustration of waiting 72 hours for a standard wire transfer while watching your operational costs climb. It’s clear that the legacy infrastructure no longer meets the demands of a real-time economy. This 2026 guide breaks down the structural shift of crypto vs traditional banking to show how you can achieve instant settlement and reduce transaction overhead by up to 80%.

Pallapay provides the professional bridge between these two worlds, ensuring that innovation never comes at the expense of institutional reliability. We will analyze the security protocols, cost-efficiency of global liquidity gateways, and the practical steps to integrate a secure crypto-fiat bridge into your financial workflow. By the end of this article, you’ll understand how to leverage the future of payments to accelerate your business growth through seamless technology that handles the heavy lifting for you.

Key Takeaways

- Identify the core structural distinctions between centralized fiat systems and decentralized blockchain networks to master the 2026 financial landscape.

- Analyze the efficiency of instant digital settlements versus traditional multi-day transfers to optimize your global liquidity management.

- Navigate the complexities of crypto vs traditional banking by leveraging stablecoins to achieve price stability within a high-performance digital asset ecosystem.

- Learn to implement a “dual-rail” financial strategy that bridges the gap between legacy systems and global crypto-fiat on-ramps seamlessly.

- Discover how to utilize an all-in-one ecosystem to transition into the future of payments while maintaining institutional-grade security and reliability.

Defining the Landscape: Crypto vs. Traditional Banking in 2026

The financial world has moved past the era of binary choices. Traditional banking remains a centralized, government-backed fiat system where institutions like the European Central Bank or the Federal Reserve control monetary policy and interest rates. In contrast, understanding what is cryptocurrency requires looking at decentralized, blockchain-based digital asset ecosystems that operate without central intermediaries. By 2026, the discussion regarding crypto vs traditional banking has shifted from a narrative of competition to one of sophisticated co-existence. Global finance now utilizes the structural stability of legacy systems alongside the high-velocity efficiency of digital ledgers.

This evolution isn’t a replacement of the old for the new. It’s a strategic integration that allows for a more resilient economy. Merchants and institutions are adopting an all-in-one approach to manage their assets, seeking to combine the regulatory safety of established banks with the instant settlement capabilities of blockchain technology. Pallapay serves as a visionary partner in this space, acting as the professional bridge that connects these two distinct worlds. The Future of Payments is defined by this hybrid model, where the complexity of the underlying technology is managed behind the scenes to provide a seamless user experience.

The Core Philosophy: Centralization vs. Decentralization

Central banks manage inflation through direct intervention and policy shifts. This model relies heavily on institutional trust and human decision-making. Decentralization offers a different path by using distributed ledgers to remove single points of failure. This ensures that no single entity can halt a transaction or alter the record. Trust is shifted from institutional history to algorithmic transparency. By mid-2026, data from the Bank for International Settlements indicates that over 90% of central banks are engaged in digital currency projects, proving that even centralized entities recognize the value of blockchain’s structural integrity.

The Infrastructure Shift: From SWIFT to Blockchain

The legacy SWIFT network, which has been the standard since 1973, often requires three to five business days for international settlement. This delay creates liquidity bottlenecks for modern enterprises that operate in a real-time global market. Blockchain infrastructure solves this problem by enabling 24/7/365 transaction processing. Stablecoins like USDT have emerged as a vital digital bridge, providing a secure fiat settlement solution that maintains value while moving at the speed of the internet. This shift allows businesses to capture global opportunities without the traditional 48-hour wait for funds. Using a professional crypto wallet, companies can now manage global liquidity with an instant advantage that was previously impossible under the legacy banking framework.

Structural Differences: Settlement, Speed, and Control

The fundamental divergence in crypto vs traditional banking lies in the architecture of trust and the mechanics of the ledger. Traditional banking relies on a centralized, hierarchical system where transactions require verification from multiple intermediaries. This legacy structure creates a “pending” state that can last for days. In contrast, blockchain technology utilizes a decentralized protocol to validate transactions, moving funds directly from sender to receiver without a central clearinghouse. While a bank balance might appear to update immediately on a mobile app, the actual interbank transfer often takes 48 to 72 hours to achieve full settlement.

Ownership models also differ significantly. In a traditional bank, you’re essentially a creditor; the institution holds your assets and grants you access to them. Cryptocurrency allows for self-custody, where the user maintains absolute control via private keys. This shift eliminates the risk of account freezes but places the responsibility of security solely on the owner. When businesses require a bridge between these two worlds, they often look for a fiat settlement solution that combines the speed of crypto with the stability of traditional accounting.

Settlement finality is the point where a transaction is irrevocably recorded on the blockchain and cannot be reversed or altered by any party. Unlike legacy systems that permit chargebacks and reversals weeks after a purchase, blockchain transactions are permanent once confirmed. This provides merchants with absolute certainty and eliminates the risk of friendly fraud.

Transaction Velocity and Global Reach

Traditional banks operate within strict geographical and temporal boundaries. Cross-border payments typically pass through 3 to 5 correspondent banks, each adding its own processing time and regulatory checks. Because these institutions rely on “opening hours” and specific time zones, liquidity can be trapped over weekends or public holidays. Crypto ignores these artificial barriers, providing 24/7/365 liquidity. As digital assets continue reshaping the banking industry, the friction of traditional rails becomes more apparent to global enterprises. A business in Dubai can send value to a partner in Singapore at 2:00 AM on a Sunday, achieving confirmation in minutes rather than days.

Cost Structures: Fee Transparency vs. Hidden Margins

The traditional banking chain is notorious for “hidden” costs, including currency exchange markups and intermediary bank fees that erode margins. These costs are often unpredictable until the final amount hits the destination account. The crypto ecosystem uses a transparent “gas” or network fee model where costs are dictated by network demand rather than the value of the transfer. For institutional players and high-volume traders, using an OTC crypto exchange is the preferred method to secure tight spreads and avoid the slippage associated with public order books. This level of cost control allows for more precise financial planning and improved bottom-line results. If you’re ready to optimize your business liquidity, you can convert your digital assets through a professional desk today.

Addressing the Volatility and Security Myths

Price volatility remains the primary objection for executives and individuals evaluating the crypto vs traditional banking landscape. While Bitcoin experienced price fluctuations of over 40% in certain quarters of 2024, the market has matured significantly. Professional commerce no longer requires direct exposure to these market swings. The evolution of the digital asset space has created a bifurcated system where speculative assets are separated from functional, utility-based financial tools. Reliability is the new standard for 2026.

The Role of Stablecoins in Business

Commercial operations now utilize stablecoins like USDT and USDC to eliminate the risk of asset depreciation. These tokens maintain a 1:1 peg with the US Dollar, providing the rapid settlement speeds of blockchain without the price instability of traditional cryptocurrencies. In 2025, stablecoin transaction volume surpassed $15 trillion, proving they are no longer niche experiments but essential liquidity tools. Businesses use these assets for several critical functions:

- Instant Payroll: Settling wages for global teams in minutes rather than days.

- Vendor Payments: Executing high-value transfers without the 3% to 5% fees associated with legacy wire transfers.

- Capital Preservation: Holding digital value in a non-volatile format during periods of market uncertainty.

By integrating instant fiat settlement, merchants can accept digital payments and immediately convert them into local currency. This process removes the volatility hurdle entirely, ensuring that the value captured at the point of sale is the exact value that reaches the corporate treasury.

Security Protocols: Institutional vs. Personal

Security concerns often stem from a misunderstanding of how blockchain functions compared to legacy databases. Traditional banks use centralized servers that represent a single point of failure. If the central database is breached, every account is compromised. Blockchain utilizes a decentralized ledger that is mathematically immutable. As crypto’s integration into mainstream finance deepens, the focus has shifted from protocol security to access point security.

Most publicized “hacks” occur at centralized exchanges with weak internal controls, not on the blockchain itself. To counter this, Pallapay implements institutional-grade security that exceeds standard banking requirements. We utilize multi-signature (multi-sig) wallets that require three or more independent authorizations before any capital moves. This system is far more robust than the two-factor authentication used by traditional retail banks. Our MSB registration ensures that all operations meet strict regulatory standards, providing the peace of mind that institutional partners demand. We don’t just facilitate transactions; we provide a secure, all-in-one ecosystem where the future of payments is anchored in absolute stability.

The Hybrid Model: Bridging the Gap for Modern Commerce

The binary debate of crypto vs traditional banking has evolved into a sophisticated synthesis. Forward-thinking enterprises no longer choose between these systems; they implement a dual-rail strategy. This approach allows them to harness the 24/7 liquidity of blockchain while maintaining the accounting rigor of legacy finance. High-performance on-ramps and off-ramps serve as the vital connective tissue in this ecosystem, ensuring that capital remains fluid across both digital and physical ledgers.

“As global financial authorities tighten oversight, holding a verified MSB status has become the ‘non-negotiable passport for digital commerce,’ ensuring that every transaction meets the highest standards of international transparency and security.”

By 2026, the distinction between a digital asset provider and a traditional bank has blurred. Regulation has transformed crypto platforms into highly secure, bank-like entities that prioritize KYC (Know Your Customer) and AML (Anti-Money Laundering) protocols. This shift doesn’t hinder innovation; it provides the institutional stability required for mass adoption. Businesses now view blockchain not as a replacement for the bank, but as a superior settlement layer that operates without the friction of legacy clearinghouses.

This evolution has paved the way for a new generation of financial technology companies. While some services like BounceMoney provide modern payment processing solutions that leverage this new infrastructure, others like ILoveUrLoans are innovating within traditional finance to offer faster access to personal loans and cash advances.

Fiat Settlement for Global Merchants

Merchants often fear the 10% daily price swings typical of digital assets. Pallapay solves this through fiat settlement services that lock in exchange rates at the moment of purchase. By converting Bitcoin or USDT to local currency instantly, businesses eliminate market risk. This process simplifies tax reporting because the ledger reflects familiar denominations like USD or EUR. By January 2026, data suggests that 82% of cross-border B2B payments utilize some form of stablecoin settlement to bypass the high fees of traditional wire transfers. This hybrid approach provides the speed of crypto with the accounting certainty of fiat.

Regulatory Evolution and Compliance

The implementation of the MiCA framework in Europe and similar structures in North America has forced the industry to mature. Institutional players now demand partners that mirror the compliance standards of Tier-1 banks. Pallapay meets these stringent requirements through its MSB registrations in the USA and Canada. This regulatory foundation builds the trust necessary for high-volume OTC trades and corporate treasury management. When a business partners with a regulated entity, they aren’t just buying technology; they’re securing a compliant bridge to the future of finance. This level of oversight ensures that crypto vs traditional banking is no longer a conflict, but a collaborative partnership.

Implementing the Future: How Pallapay Enables Transition

Pallapay acts as the definitive global enabler for businesses and individuals ready to move beyond the limitations of legacy finance. While the debate of crypto vs traditional banking often focuses on theoretical benefits, Pallapay delivers practical utility through an all-in-one ecosystem. It bridges the gap by providing the stability of institutional finance alongside the speed of blockchain. Users no longer need to choose between the two worlds; they can manage both through a single, secure interface. This professional approach ensures that digital assets are no longer isolated experiments but are instead core components of a modern financial strategy.

The Pallapay Mastercard exemplifies this integration by allowing for instant conversion of digital assets for daily spending at over 60 million merchants worldwide. It’s a tool designed for the executive who needs liquidity without the 3 to 5 business day delay typical of standard bank transfers. By holding a balance in the Pallapay ecosystem, users benefit from real-time settlement and a level of flexibility that traditional debit cards cannot match. It’s the future of payments, delivered with the reliability of a global fintech leader. For those seeking to understand how crypto debit cards unlock the future of payments, this integration represents the seamless merger of digital assets with traditional spending infrastructure.

Retail and In-Store Crypto Integration

Merchants can now bring digital currency directly to the checkout counter using Crypto POS machines. These devices allow retail stores to accept payments in various cryptocurrencies while receiving settlements in their local fiat currency. This setup eliminates the volatility risk for the business owner. Transaction fees often drop significantly, sometimes by as much as 70% compared to the 3.5% typically charged by traditional merchant services. The user experience is indistinguishable from standard banking; it’s a simple tap-and-pay process that completes in seconds.

By integrating these systems, businesses tap into a global market of over 420 million crypto users. The transition is seamless because the hardware mirrors the design of traditional card readers, requiring zero additional training for staff. This physical-digital integration is essential for the widespread adoption of digital assets in the real economy. When analyzing crypto vs traditional banking in a retail context, the primary advantages are the lack of chargeback fraud and the instant nature of the transaction settlement.

High-Volume Liquidity and OTC Services

Institutional clients and high-net-worth individuals require a specialized approach when moving large volumes of assets. Pallapay provides deep liquidity pools that allow for the movement of millions of dollars without causing market slippage or price volatility. A standout feature of this service is the ability to sell USDT for cash in Dubai through secure, physical branch locations. This service provides a level of security and transparency that purely digital exchanges often lack.

This professional OTC service ensures that users can exit digital positions and receive physical currency instantly. It’s a level of reliability that matches the highest standards of private banking while maintaining the efficiency of the crypto space. Every transaction is handled with the utmost discretion and speed, reinforcing Pallapay’s role as a visionary partner in the financial evolution. Whether you are a merchant looking to scale or an individual managing a diverse portfolio, you can explore the Pallapay Ecosystem to find the professional tools necessary for the next era of finance.

Mastering the New Standard of Global Finance

The financial landscape of 2026 favors the prepared. Business owners no longer need to choose between crypto vs traditional banking when they can leverage a hybrid model that captures the speed of blockchain and the stability of fiat. By moving away from the restrictive T+3 settlement cycles of legacy banks, you gain access to instant liquidity across 180+ countries. Our gateway doesn’t just process transactions; it empowers growth by removing the technical barriers to entry for every merchant. Pallapay anchors this transition with physical offices in Dubai, Singapore, and Istanbul, providing the institutional reliability your stakeholders expect. It’s a system built on trust, backed by our status as a regulated MSB in the USA and Canada. You’ve seen the evolution of the market, and now it’s time to align your infrastructure with the leaders of the industry. Join the future of finance with Pallapay’s secure payment gateway and secure your competitive edge. Your global expansion starts today.

Frequently Asked Questions

Is crypto safer than traditional banking for large transfers?

Crypto offers superior security for large transfers because it eliminates intermediary risks and centralized points of failure. Traditional banks rely on manual verification which often causes 48 hour delays. Blockchain technology uses cryptographic proof to secure 100 percent of the transaction data. By 2026, the adoption of multi-signature cold storage has reduced exchange-side theft by 45 percent compared to 2021 levels, providing a more resilient infrastructure than legacy systems.

Can I use cryptocurrency for my business without facing volatility?

You can eliminate volatility risks by using stablecoins or instant fiat settlement features. Pallapay allows merchants to accept Bitcoin and immediately convert it to USDT or USD at the moment of sale. This process locks in the price within 2 seconds. Over 85 percent of businesses using crypto gateways now prefer stablecoin settlements to maintain 100 percent price predictability while expanding their global customer reach.

How do transaction fees compare between crypto and credit cards?

Crypto fees are significantly lower, often costing 80 percent less than standard credit card processing. While credit cards charge between 2.5 percent and 4 percent per transaction, crypto network fees on chains like Polygon or Tron stay below $0.50 regardless of the transfer amount. Comparing crypto vs traditional banking costs reveals that a $10,000 transfer costs pennies on-chain, whereas banks may charge $50 plus hidden exchange rate markups.

What is an MSB registration and why does it matter for crypto?

An MSB registration is a legal requirement for Money Services Businesses to operate under FinCEN regulations in the United States. It ensures the platform follows strict Anti-Money Laundering protocols. Pallapay maintains active MSB status to provide a secure environment for all users. This registration proves that a provider meets the 2026 standards for financial transparency and institutional-grade accountability, protecting your assets from regulatory scrutiny.

Can I convert my crypto directly to my traditional bank account?

You can convert digital assets to your bank account using integrated off-ramps and OTC services. Pallapay facilitates direct transfers to bank accounts in over 100 countries through SEPA and SWIFT networks. Most conversions complete within 24 hours. This seamless link between crypto vs traditional banking systems allows you to manage liquidity without the friction of multiple third-party exchanges or the 3 day waiting periods common in older platforms.

Why do cross-border bank transfers take so much longer than crypto?

Traditional transfers take 3 to 5 days because they pass through multiple correspondent banks. Each intermediary bank must verify the transaction and perform its own compliance checks. Crypto operates on a peer-to-peer basis, settling in roughly 10 minutes on the Bitcoin network or seconds on faster chains. This removes the need for the 4 or 5 middleman institutions that slow down the legacy financial system every day.

Do I need a bank account to use a crypto payment gateway?

You don’t need a traditional bank account to use a crypto payment gateway for basic digital asset management. Gateways allow you to receive, store, and spend crypto using digital wallets. This technology provides financial access to the 1.4 billion unbanked individuals globally. While a bank account is necessary for fiat withdrawals, the gateway itself functions as a standalone financial hub for the modern digital economy without requiring credit checks.

How does the Pallapay Mastercard bridge the gap between crypto and banking?

The Pallapay Mastercard allows you to spend your crypto balance at over 60 million merchant locations worldwide. It converts your digital assets to fiat currency instantly at the point of sale. This eliminates the need to manually sell crypto before making a purchase. It’s the ultimate tool for daily utility, providing the speed of blockchain with the universal acceptance of the global Mastercard network for a truly borderless experience.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.

Leave a Reply