Traditional banking delays cost high-volume traders significant capital in missed opportunities every year. When you’re managing XAU/USD positions or complex Forex CFDs, waiting days for a wire transfer to clear isn’t just frustrating; it’s a structural liability that prevents you from capturing market momentum. You know that speed is the ultimate currency in finance, yet legacy systems continue to throttle your growth with slow settlement and high slippage. By integrating a professional crypto payment gateway dubai, traders can finally bypass these hurdles to maintain a competitive advantage in volatile markets.

Discover how advanced infrastructure is revolutionizing high-volume Forex and Gold CFD trading by providing seamless liquidity and institutional-grade security. By adopting a sophisticated digital bridge, you can move beyond the limitations of traditional finance to achieve instant settlement in stablecoins and access global liquidity for your most critical pairs. This article explores the secure, regulated systems that are turning digital asset efficiency into a fundamental component of a trader’s success. We’ll examine how these tools empower individuals to navigate the XAU/USD markets with the precision and speed required to fundamentally change their financial future.

Key Takeaways

- Learn how instant stablecoin settlements eliminate the capital delays that often disrupt high-volume Forex and Gold trading strategies.

- Understand the mechanics of XAU/USD CFD trading and how it’s used as a sophisticated hedge against traditional currency volatility.

- Discover why a professional crypto payment gateway dubai is essential for achieving the low latency and high throughput required by modern brokers.

- Explore the strategic advantages of using secure APIs to automate deposit confirmations and streamline institutional digital asset management.

- See how a comprehensive ecosystem of OTC desks and gateway tools provides a reliable bridge for scaling your global trading operations.

The Role of Crypto Payment Gateways in Global Financial Markets

Modern finance requires a bridge that moves as fast as the markets themselves. While a traditional payment gateway handles basic authorizations for retail transactions, high-stakes trading demands a far more rigorous infrastructure. A crypto payment gateway acts as a sophisticated translator between the decentralized world of blockchain and the established stability of fiat currencies. It’s no longer just a tool for simple checkouts; it’s the engine that provides institutional-grade liquidity for high-volume financial operations. By converting digital assets into usable capital in real time, these gateways ensure that brokers and traders don’t lose precious seconds to legacy banking delays.

Bridging Digital Assets and Traditional Finance

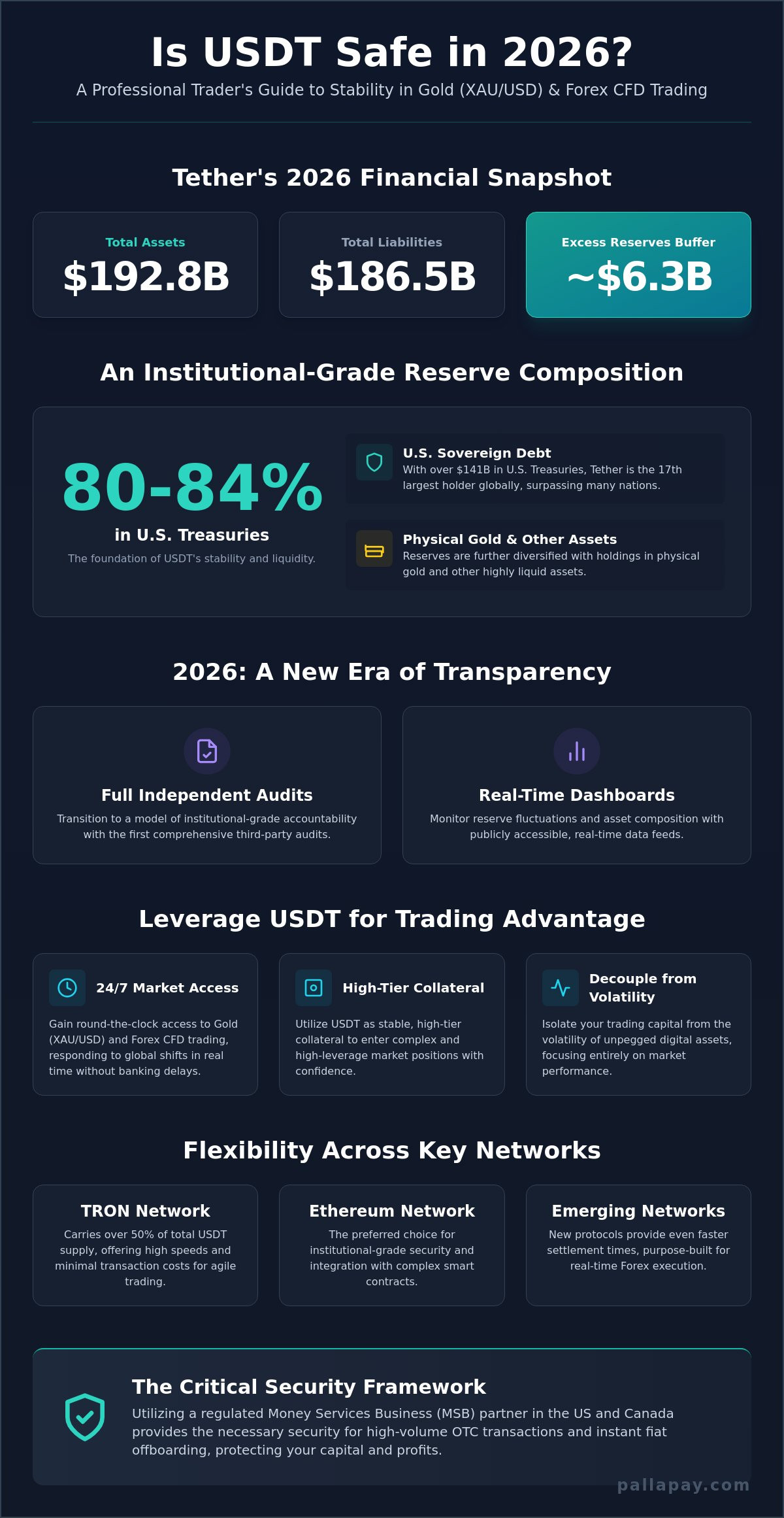

The mechanism behind real-time crypto-to-fiat conversion is what allows professional traders to maintain their edge. When capital is locked in a blockchain, it’s effectively sidelined from traditional markets until it’s converted. Professional gateways solve this by offering instant fiat settlement, allowing funds to be deployed into Gold or Forex pairs without waiting for multi-day wire transfers. This transition is built on a foundation of trust and regulatory compliance. For instance, Pallapay maintains MSB registrations in the US and Canada, providing the institutional oversight necessary for large-scale capital movement. This regulated approach reduces the friction of cross-border transfers, making it possible to manage assets across 180+ countries with the same ease as a local transaction.

The 2026 Landscape of Digital Payments

By 2026, the perception of digital assets has shifted from speculative tokens to essential financial utility. Industry projections suggest that over 25% of cross-border trade settlements in leading financial hubs will involve some form of digital asset. Stablecoins like USDT have become the primary medium for these settlements because they combine the 24/7 availability of blockchain with the price stability of the US dollar. Integrating a high-performance crypto payment gateway dubai into a trading ecosystem isn’t just about keeping up with trends; it’s a strategic move to secure future-proof infrastructure. As gatekeeper technology evolves, the focus has moved toward systems that are decentralized in execution yet strictly regulated in oversight. This evolution allows brokers to offer their clients a secure path for funding high-volume accounts, turning complex technical conversions into standard, effortless business operations.

Transforming Financial Lives through Gold and USD CFD Trading

CFD trading represents a fundamental shift in how capital is deployed within global markets. By utilizing Contracts for Difference, traders can capitalize on the price fluctuations of high-value assets without the friction of physical delivery. This is particularly transformative for those focused on the XAU/USD pair, where Gold serves as a critical hedge against global economic shifts. Successful trading isn’t just a technical skill; it’s a strategic evolution that can redefine an individual’s financial trajectory. When you master the mechanics of USD-based pairs, you gain the ability to navigate complex macroeconomic trends with precision and confidence.

The Power of Gold and USD CFD Markets

Leverage is the primary catalyst for growth in these markets. It allows professional traders to control larger positions with a fraction of the total value, effectively scaling their potential for financial independence. While leverage requires disciplined risk management, it remains a preferred tool for high-net-worth individuals who understand market psychology. These participants don’t just trade; they use Gold CFDs to protect wealth and capture momentum during periods of currency instability. This institutional approach to trading is supported by recent research on cryptocurrency in banking, which highlights how digital assets are providing more efficient alternatives to traditional financial structures. Navigating global economic shifts requires this deep understanding of USD pairs, as the US Dollar dictates the rhythm of international trade and provides a stable benchmark for commodity valuation.

Gateway Synergy: Funding Your Trading Account

The most significant hurdle in high-frequency trading is the speed of capital movement. Traditional banking systems often impose delays that can lead to missed entry points or forced liquidations during margin calls. Integrating a professional crypto payment gateway dubai solves this operational bottleneck by allowing for near-instant account funding. Using USDT as a settlement currency provides a stable, dollar-pegged medium that perfectly mirrors the CFD environment. This synergy ensures that your liquidity is always where it needs to be, regardless of market volatility. You can Streamline your trading with fiat settlement solutions to bridge the gap between your digital wallet and the live trading floor. For those ready to optimize their infrastructure, utilizing a dedicated API for crypto payments can further automate these critical processes, ensuring that your trading desk operates with institutional efficiency around the clock.

Evaluating Gateway Performance for High-Frequency Forex Markets

High-frequency Forex trading operates on the razor’s edge of execution speed. For a broker, the infrastructure supporting capital inflows is just as critical as the trading engine itself. When evaluating a crypto payment gateway dubai, three metrics dictate operational success: latency, uptime, and throughput. Latency determines how quickly a deposit is recognized and credited; uptime ensures the gateway is available during the 24/7 cycle of digital markets; and throughput manages the volume of concurrent transactions without bottlenecking. In the fast-moving world of currency pairs, settlement speed is the most important factor. It’s the difference between a client entering a position at the desired price or losing the opportunity to market slippage.

Choosing between custodial and non-custodial gateway architectures is a strategic decision for institutional entities. Custodial gateways often provide superior speed by handling internal ledger transfers, which allows for near-instant fiat conversion. This architecture is particularly effective when backed by deep liquidity pools. These pools act as a buffer, ensuring that even large-scale conversions from Bitcoin to USDT occur at stable rates. Without this depth, high-volume transfers can trigger significant slippage, eroding the capital efficiency that professional traders rely on to maintain their margins.

Latency and Execution Speed

Millisecond delays are not merely inconveniences; they’re financial liabilities. In CFD trading, entry prices move constantly, and a delay in account funding can force a trader into a sub-optimal position. Real-time price oracles are the technical heart of a high-performance gateway, providing the accurate data feeds necessary for instant conversion. Pallapay optimizes this process through a high-speed transaction engine designed to handle institutional loads. By minimizing the time between a blockchain confirmation and account crediting, the system ensures that liquidity is ready for deployment exactly when the market presents an opening.

Regulatory Stability and Security

Security is the bedrock of institutional trust. Global MSB standards, such as those followed by Pallapay in North America, provide a framework for reliability that goes beyond simple encryption. Protecting institutional assets requires multi-signature security protocols, ensuring that no single point of failure can compromise the ecosystem. This rigorous approach to safety is what allows a crypto payment gateway dubai to serve as a professional bridge for high-stakes trading. For a deeper understanding of how these systems evolve to meet new threats, you should Explore the 2026 guide to institutional crypto security. Maintaining this level of protection is essential for any broker looking to scale their digital asset operations while keeping client funds secure and accessible.

Strategic Implementation: API Integration for Commodity Trading

Successful commodity trading desks rely on more than just market analysis; they require a robust technical backbone. Integrating a payment API into a trading platform involves a precise series of steps to ensure seamless capital flow. Developers first establish a secure connection using API keys. The system is then configured to listen for webhook notifications, which are essential for instant deposit confirmation. This automation allows a trader’s balance to update the moment a blockchain transaction is verified. To ensure data integrity, every communication must be protected by secure cryptographic signatures. This prevents unauthorized access and ensures that only legitimate transactions are processed. Implementing a crypto payment gateway dubai requires this level of technical rigor to protect high-value institutional accounts and ensure that liquidity is always available for Gold and Forex positions.

Optimizing API Performance for High Volume

High-frequency environments demand high availability. Rate limiting and load balancing are critical best practices that prevent system degradation during peak market volatility. When Gold prices move sharply, transaction volume can spike. Your API must handle these surges without latency. Additionally, automating the withdrawal process is vital. By utilizing efficient crypto off-ramp solutions for businesses, brokers can ensure that successful traders access their capital in fiat or stablecoins without manual intervention. This efficiency is what allows a trading desk to scale alongside its most successful clients.

Customizing the Trader Experience

Brand consistency builds trust. White-labeling allows brokers to integrate the gateway seamlessly into their existing interface, making the funding process feel like a native part of the platform. Custom dashboards provide real-time transaction monitoring, which is crucial for transparency. When trading global Forex pairs, multi-currency support is a non-negotiable requirement. A versatile crypto payment gateway dubai supports various digital assets, allowing traders from diverse backgrounds to fund their accounts and pursue financial independence through XAU/USD and major currency pairs. This level of customization transforms the user experience from a simple transaction into a professional financial partnership.

Ready to upgrade your infrastructure? Access the Pallapay Payment API documentation to begin your integration today.

Scaling with Pallapay: An Institutional Ecosystem for Digital Assets

Pallapay isn’t just a standalone utility; it’s a comprehensive suite of tools designed for the modern trader. While many providers offer basic plugins for retail use, this ecosystem bridges the gap between disruptive innovation and institutional reliability. By integrating a crypto payment gateway dubai into your financial workflow, you gain access to a unified platform where gateway services, OTC desks, and card solutions operate in perfect tandem. This integrated approach is vital for managing high-volume Gold and USD transactions without the friction of disparate systems. It’s about providing a definitive destination for all technical needs, ensuring that your capital moves with the same speed as the global markets.

The brand’s personality is that of a strategic partner, deeply grounded in the practicalities of modern commerce. We don’t just facilitate transactions; we provide the professional bridge that connects established practices with modern advancements. With MSB registrations in the US and Canada and a presence in over 180 countries, the infrastructure is built to instill absolute trust. This global reach ensures that whether you’re settling a Forex position or funding a large-scale commodity trade, the background processes are handled with the efficiency of a world-class facilitator.

Comprehensive Liquidity Solutions

Large-scale capital movement requires deep liquidity to avoid the pitfalls of slippage. By combining the crypto payment gateway dubai with global OTC desks, Pallapay supports high-volume CFD operations that traditional exchanges simply can’t match. This synergy ensures that even the most significant conversions from digital assets to fiat occur at stable, predictable rates. The Pallapay Mastercard provides instant access to your assets, allowing for real-time spending or rapid capital deployment. For those managing institutional portfolios, it’s essential to consult the institutional guide to high-volume OTC trading to understand how these liquidity layers function together to protect your bottom line.

Your Path to Financial Evolution

Trading Forex and Gold CFDs has the transformative potential to redefine your financial trajectory. It offers a clear path to independence through the strategic use of leverage and a deep understanding of market volatility. However, achieving this level of success in 2026 depends entirely on the strength of your underlying infrastructure. Moving beyond the limitations of legacy banking isn’t just an option; it’s the first step toward institutional-grade trading performance. By adopting a partner that prioritizes speed, security, and regulatory clarity, you secure your position in an inevitable global evolution. It’s time to transition from traditional friction to a future-proof ecosystem. Join the Pallapay ecosystem today and experience the professional standard of digital asset management.

Securing Your Competitive Edge in Modern Finance

The evolution of Forex and Gold CFD trading is inextricably linked to the efficiency of your underlying technology. We’ve explored how institutional-grade gateways solve the chronic issues of settlement delays; they provide the real-time liquidity required for high-stakes XAU/USD positions. By integrating a secure API and leveraging deep liquidity pools, you can move beyond legacy banking limitations to capture market movements with millisecond precision. Utilizing a professional crypto payment gateway dubai is a strategic necessity for building a reliable bridge between digital innovation and traditional financial stability.

Pallapay supports this transition as a regulated MSB in the US and Canada, serving professional clients across more than 180 countries. Our ecosystem provides the real-time liquidity for Gold and USD pairs that modern trading desks demand. Empower your trading infrastructure with Pallapay and take the definitive step toward a more efficient financial future. It’s time to elevate your operational standards and embrace the inevitable evolution of global commerce.

Frequently Asked Questions

What is a crypto payment gateway for Forex trading?

A crypto payment gateway for Forex trading is a specialized technical infrastructure that allows brokers to accept digital assets for account funding. It facilitates the immediate conversion of cryptocurrencies into fiat or stablecoins to maintain constant trading liquidity. Utilizing a professional crypto payment gateway dubai ensures that capital moves at the speed of global markets, allowing traders to fund accounts and enter positions without the delays associated with legacy wire transfers.

How does Gold CFD trading differ from traditional gold investment?

Gold CFD trading focuses on speculating on the price movements of the XAU/USD pair rather than acquiring physical bullion. This method provides significant capital efficiency through leverage, allowing you to control larger positions with a smaller initial deposit. Unlike traditional investment, CFDs enable you to profit from both rising and falling markets, making it a more versatile tool for active wealth management and tactical hedging.

Why is USDT preferred for trading settlements in 2026?

USDT is the preferred settlement medium because it combines the 24/7 technical agility of blockchain with the price stability of the US Dollar. By 2026, it’s become the institutional standard for reducing volatility during the funding process. It eliminates the risk of asset devaluation during the transfer period, ensuring that the exact amount sent is the amount credited to your trading desk for immediate market deployment.

How long does it take to settle crypto-to-fiat through a gateway?

Settlement through a high-performance gateway typically occurs within minutes, depending on the specific blockchain confirmation times. Professional systems provide near-instant fiat conversion once a transaction is verified on the network. This speed is a critical advantage over traditional banking, which often requires three to five business days for international settlements to clear and become usable for high-volume trading operations.

Is a crypto payment gateway secure for high-volume transactions?

Yes, institutional-grade gateways are specifically engineered to handle high-volume transactions with absolute security. These systems utilize multi-signature protocols and advanced encryption to protect large-scale capital movements from end to end. When you choose a regulated MSB, you’re adopting an infrastructure that meets rigorous global standards for asset protection and operational reliability, ensuring that your trading capital remains secure throughout the conversion process.

What are the benefits of using an API for crypto payments in trading?

An API for crypto payments automates the entire funding and withdrawal lifecycle, significantly reducing human error and operational overhead. It allows for real-time webhook notifications, so your trading platform can credit accounts the moment a deposit is confirmed. This seamless integration is essential for maintaining a professional, white-labeled user experience that builds trust with high-net-worth traders who require instant access to their funds.

Do I need a special license to accept crypto for my trading platform?

Regulatory requirements vary by jurisdiction, but most platforms partner with a licensed provider to handle the technical and legal complexities of digital asset processing. By utilizing a crypto payment gateway dubai, brokers can leverage the provider’s existing MSB registrations and compliance frameworks. You should always verify the specific licensing needs for your operational region to ensure full regulatory alignment while maintaining a secure bridge to traditional finance.

How can CFD trading change my financial life?

CFD trading offers a path to financial independence by allowing you to capitalize on global economic shifts with limited initial capital. Mastering the XAU/USD and Forex markets enables you to build a diversified portfolio that’s resilient to inflation and currency devaluation. It’s a transformative skill that provides the freedom to manage your own wealth with professional precision, using institutional-grade tools to secure your financial future.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.