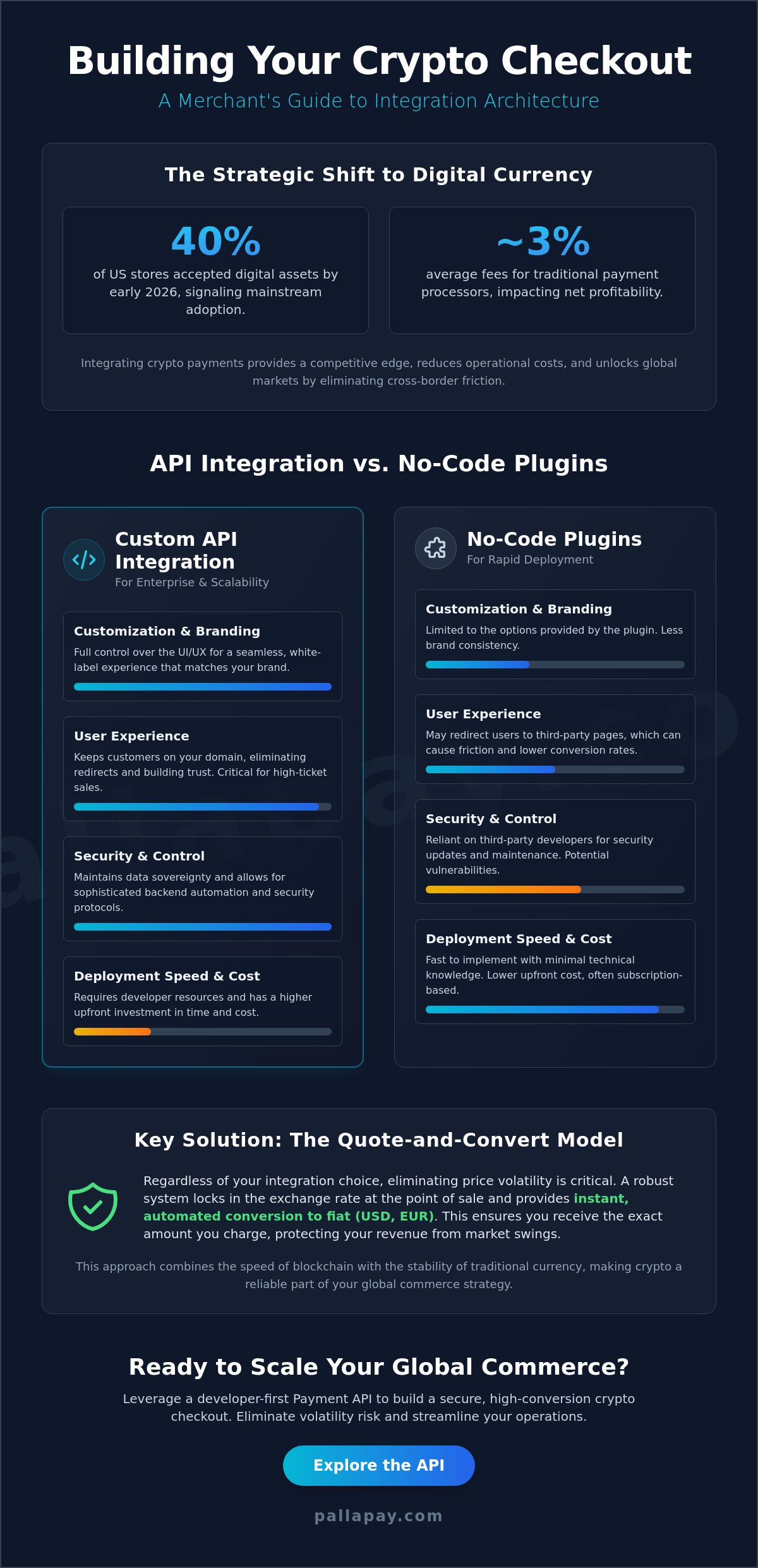

With 40% of stores in the US now accepting digital assets according to market research from early 2026, the competitive landscape has shifted toward merchants who can offer the most efficient payment experience. You likely recognize that while customers demand flexibility, the technical hurdles of designing a crypto checkout flow often lead to revenue loss through friction or price volatility. It’s frustrating to watch a transaction stall because of slow confirmation times or complex wallet connections. We understand that your priority is a system that feels as reliable as a traditional credit card processor but operates with the speed of the blockchain.

This guide provides the technical and strategic framework to build a secure, high-converting checkout that eliminates price risk through instant fiat conversion. You’ll learn how to implement a quote-and-convert model that locks in rates, ensuring you receive the exact USD or EUR amount regardless of market swings. We’ll also cover how to integrate an API for crypto payments that simplifies accounting and maintains compliance with the 2025 GENIUS Act and FATF Travel Rule requirements. By the end of this article, you’ll have a clear roadmap for turning crypto into a standard, effortless part of your global commerce operations.

Key Takeaways

- Understand the shift toward mainstream crypto adoption and how to capture global demand from tech-savvy demographics and unbanked populations.

- Master the core principles of designing a crypto checkout flow to reduce friction using QR codes, automated network selection, and WalletConnect integrations.

- Evaluate the technical trade-offs between bespoke API integrations and streamlined no-code plugins for major CMS platforms like Shopify and Magento.

- Eliminate volatility risk by implementing automated fiat settlement that locks in exchange rates at the point of sale for instant conversion.

- Scale your operations by connecting online gateways with physical crypto POS machines and high-volume OTC settlement services for a unified commerce experience.

The Strategic Shift: Why Your Website Needs a Crypto Checkout in 2026

The landscape of global commerce has fundamentally altered as digital assets move from speculative holdings to functional currency. Merchants now view understanding digital currencies as a core competency for maintaining a competitive edge in a digital-first economy. When you are designing a crypto checkout flow, you are effectively installing a high-speed liquidity bridge that bypasses the friction of legacy financial systems. This shift is driven by a consumer base that increasingly values the privacy, security, and autonomy inherent in blockchain-based transactions.

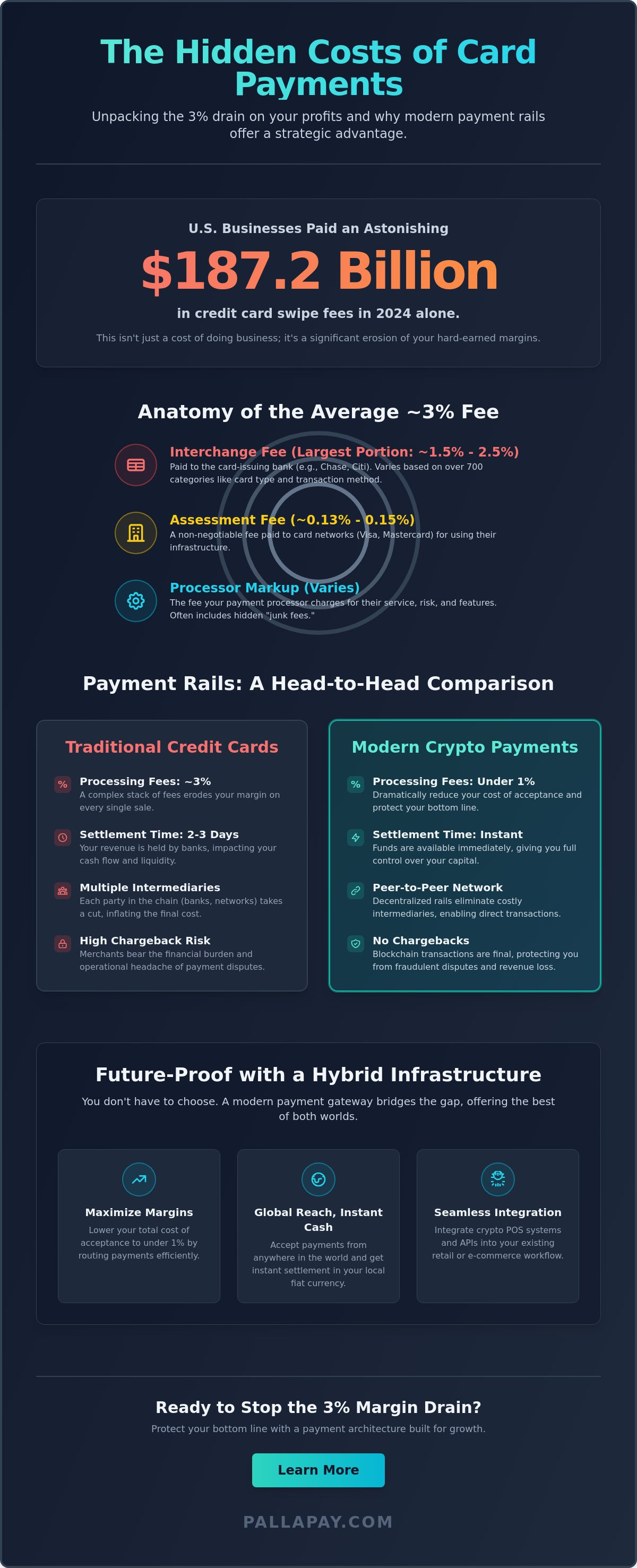

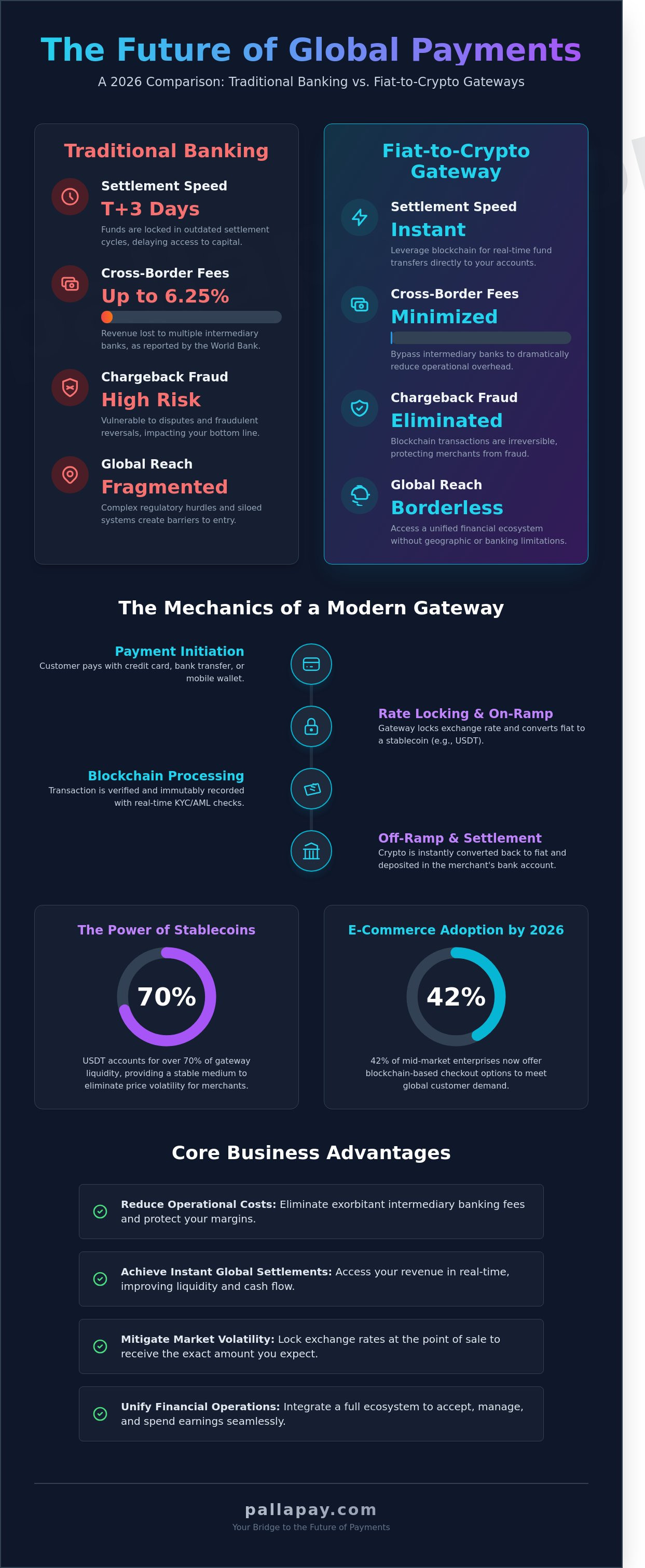

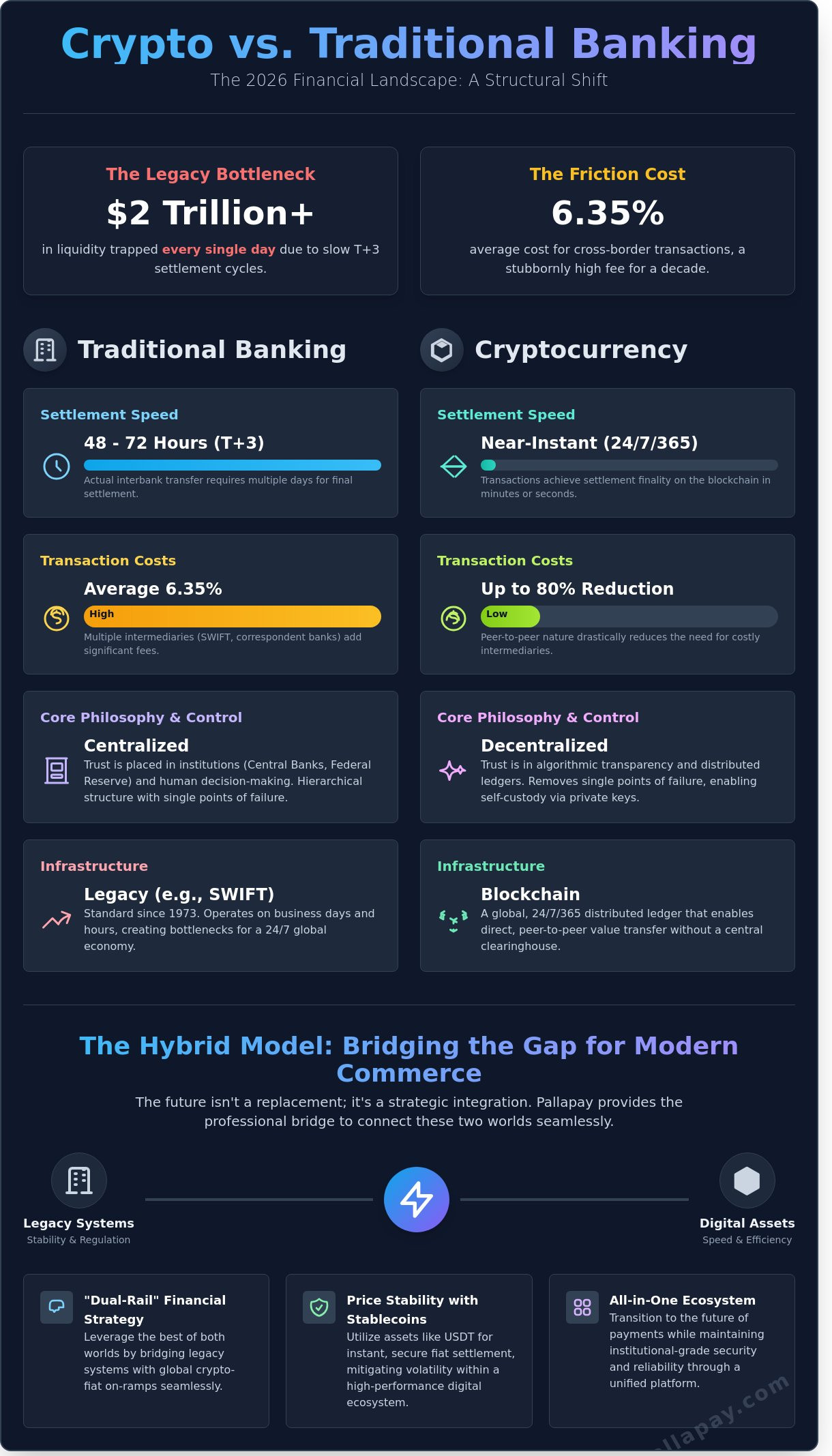

Operational costs remain a primary driver for this transition. Traditional payment processors often levy merchant fees that average 3%, which significantly impacts the net profitability of high-volume businesses. In contrast, optimized crypto gateways offer a much leaner cost structure, allowing organizations to retain a larger portion of their revenue. Industry data from early 2026 indicates that nearly 90% of sellers have received direct requests for crypto options, signaling that consumer preference has reached a critical tipping point for mainstream adoption.

Global Market Reach and the New Consumer

Integrating crypto payments allows e-commerce brands to engage with a global audience without the traditional barriers of cross-border banking. This includes high-net-worth individuals who prefer spending their digital assets directly to maintain financial fluidity. By offering these options, you provide a frictionless experience for international customers who would otherwise face high currency exchange fees or transaction declines. It is a strategic expansion into a borderless market that operates beyond the limitations of traditional geography.

Operational Efficiency: Speed and Security

The speed of blockchain finality offers a distinct advantage over the multi-day settlement cycles of traditional banking. Once a transaction is confirmed on the ledger, the funds are secure and the risk of chargeback fraud is effectively eliminated. This is particularly critical for high-ticket retail where fraudulent disputes can cause significant financial disruption. Designing a crypto checkout flow also provides a reliable contingency against traditional processor outages, ensuring your storefront remains operational at all times. It is a professional bridge to a more resilient financial future.

Choosing Your Integration Architecture: API vs. No-Code Plugins

Decisions regarding technical architecture determine the long-term scalability of your digital storefront. When you’re designing a crypto checkout flow, the primary conflict often lies between the speed of deployment and the depth of customization. Small to mid-sized retailers frequently opt for ready-made solutions to minimize upfront development costs. Conversely, enterprise-level organizations require bespoke integrations to maintain brand consistency and data sovereignty. This choice dictates how your business will handle future volume increases and network upgrades.

E-commerce Plugins for Rapid Deployment

CMS plugins for platforms like WordPress, Shopify, and Magento provide a streamlined path to market. These third-party scripts handle the heavy lifting of wallet connectivity and transaction monitoring. However, security remains a paramount concern. It’s essential to ensure your checkout environment is isolated from core customer data to prevent cross-site scripting vulnerabilities. While plugins offer ease of use, they require regular maintenance to remain compatible with evolving blockchain network updates. If a plugin fails to update alongside a major wallet provider, your conversion rates will suffer.

Custom API Integration for Enterprise Scalability

For businesses that demand full control over the user journey, a developer-first approach is the definitive choice. Leveraging a Payment API allows you to build a white-label checkout that keeps the customer entirely on your domain. This eliminates the psychological friction caused by redirecting users to external payment pages. You can design every pixel of the interface to align with your brand’s aesthetic, which is a critical factor for building trust in the high-ticket retail sector.

Custom integrations also allow for sophisticated backend automation through webhooks. These tools provide real-time order status updates, enabling your system to trigger automated fulfillment the moment a transaction reaches the required number of network confirmations. This level of technical maturity ensures that your operations scale without increasing manual overhead. If you’re ready to build a tailored solution, exploring the API for Crypto Payments can provide the robust infrastructure needed for high-volume commerce.

Hosted payment pages represent a practical middle ground for many growing businesses. They offer a no-code approach where the service provider manages the entire UI, significantly reducing your internal technical and regulatory burden. This is an excellent choice for rapid market entry or for testing crypto demand within a specific product line before committing to a full-scale custom build. Ultimately, the right architecture depends on your internal developer resources and your long-term vision for the customer experience. Selecting the right path early prevents costly migrations later.

Designing a High-Conversion Crypto Checkout Flow (UX/UI Principles)

Designing a crypto checkout flow requires a departure from the static input fields of traditional finance toward an interactive, real-time handshake between digital environments. The primary goal is to minimize cognitive load while ensuring absolute precision. By integrating a ‘WalletConnect’ button alongside a high-resolution QR code, you provide a seamless transition for both mobile and desktop users. This dual-path approach facilitates an immediate connection that feels as intuitive as a standard digital wallet payment. It works because it respects the user’s existing habits.

Transparency is the bedrock of conversion. Your interface must display real-time exchange rates with a clear price-lock countdown, typically lasting 15 to 20 minutes. This prevents the anxiety associated with market volatility during the transaction window. For mobile users, a one-tap payment experience is essential. By deep-linking directly to a secure crypto wallet, you remove the need for manual copying and pasting, which is often where user errors occur. Efficiency in design leads directly to efficiency in settlement.

Handling Wallet Connectivity and User Errors

Effective checkout design prioritizes error prevention through smart address validation and clear network labeling. If a user attempts to send Bitcoin to an Ethereum address, the system should flag the incompatibility immediately. Best practices include using dynamic QR codes that embed both the destination address and the exact payment amount to prevent manual entry mistakes. You should also provide brief explanations of network costs to ensure users include enough for the transaction to confirm. These small details reduce support tickets and protect your revenue.

Optimizing for Trust and Transparency

Because blockchain transactions aren’t always instantaneous, maintaining a feedback loop is vital for customer retention. A live status bar showing confirmation progress, such as ‘1 of 3 confirmations received,’ keeps the user engaged and reduces the urge to refresh the page. Once the transaction is finalized, an automated email receipt should follow. This receipt must contain the transaction hash for the customer’s records. This level of technical detail provides peace of mind and establishes your brand as a professional entity. Finally, ensure your refund policy is explicitly stated. Clarify how returns are calculated in fiat terms to avoid disputes over price fluctuations. Clear communication builds long-term loyalty.

Navigating Fiat Settlement and Regulatory Compliance

Institutional reliability in the digital asset space depends on two critical factors: price stability and regulatory adherence. When you are designing a crypto checkout flow, the primary objective is to convert digital volatility into predictable fiat revenue. This process ensures that the amount your customer pays in Bitcoin or USDT matches the exact value you receive in your business account. By removing the need for merchants to hold volatile assets, the system functions as a professional bridge between innovative payment rails and traditional financial reporting.

Regulatory clarity has reached a new peak following the 2025 GENIUS Act, which brought payment stablecoins under the Bank Secrecy Act (BSA). As of 2026, 85 out of 117 jurisdictions have implemented the FATF Travel Rule, requiring the sharing of sender and recipient information for transactions. Utilizing a provider with MSB registration in the USA and Canada ensures your operations remain compliant with these evolving standards. This infrastructure provides the “regulatory peace of mind” required for enterprise-level commerce.

Fiat Settlement: Protecting Your Profit Margins

Automated fiat settlement is the technological answer to market volatility. The system locks in the exchange rate at the moment of sale, ensuring that a market crash during the transaction confirmation window does not erode your margins. Merchants can choose between threshold-based payouts or scheduled daily and weekly settlements. This flexibility allows for precise cash flow management across multiple currency accounts, including USD, EUR, and GBP. If you need to cover international operational costs, using a crypto off-ramp enables you to move funds directly to your corporate bank account with minimal friction.

Accounting and Reporting for Digital Revenue

Modern commerce requires unified reporting that syncs effortlessly with existing ERP systems. Your checkout flow should generate tax-compliant reports that treat crypto sales with the same rigor as credit card transactions. This includes capturing the transaction hash and the fiat value at the time of execution. Handling refunds is a common operational hurdle; the standard practice is to refund the original fiat value rather than the crypto amount. This protects your business from paying back more than was originally received if the asset’s price has increased. High-volume accounts must also maintain strict KYC and AML protocols to satisfy global banking partners. If you are ready to stabilize your digital revenue, you can convert crypto to fiat instantly through our automated settlement engine.

Scaling with the Pallapay Ecosystem: Beyond the Website

While designing a crypto checkout flow is the definitive first step toward digital transformation, true operational efficiency comes from integrating these digital rails into a broader, unified ecosystem. A siloed web checkout limits your growth potential by creating data fragmentation between different sales channels. Scalable businesses require a comprehensive architecture that connects online revenue with physical retail operations and corporate spending. This holistic approach ensures that your digital assets are not just a payment option, but a core component of your global financial strategy.

Unified Commerce: Connecting Web and Retail

Modern merchants shouldn’t have to manage separate reporting systems for their website and their retail store. By connecting your online gateway with physical Crypto POS machines, you synchronize sales data across all touchpoints in real-time. This centralized approach ensures that inventory levels and revenue tracking remain accurate; it doesn’t matter whether the customer pays via a mobile browser or at a physical counter. You provide a consistent brand experience that builds trust with your global audience while simplifying your internal accounting processes. This level of synchronization is the technological answer to the complexity of omnichannel commerce.

Advanced Liquidity and Corporate Spending

High-volume merchants often face liquidity challenges when they need to convert large digital asset holdings into fiat for operational needs. Utilizing an OTC crypto exchange provides the deep liquidity required for enterprise-level settlements without impacting market prices. This infrastructure is essential for businesses that use digital assets for B2B settlements or employee payroll. The journey from your first API call to a fiat withdrawal is designed to be a streamlined, professional progression:

- Integration: Implement the API for crypto payments to start accepting digital assets on your domain.

- Settlement: Configure automated fiat settlement to lock in exchange rates and eliminate volatility.

- Consolidation: View unified revenue data from both web gateways and physical POS terminals.

- Utilization: Withdraw funds to your corporate bank account or use the Pallapay Mastercard for immediate corporate spending.

Technical complexity shouldn’t be a barrier to global expansion. Professional merchants in over 180 countries have access to dedicated technical assistance to ensure their systems remain operational. By designing a crypto checkout flow that sits at the center of a wider ecosystem, you bridge the gap between disruptive innovation and institutional reliability. This isn’t just about accepting a new form of payment; it’s about adopting a forward-thinking strategic partner that handles complex background processes so you can focus on growth.

Future-Proofing Your Global Commerce Strategy

Adopting digital asset payments is no longer a speculative choice; it’s a strategic necessity for merchants seeking to capture a global, tech-savvy market. By prioritizing a friction-free user experience and implementing automated fiat settlement, you eliminate the traditional barriers of price volatility and technical complexity. Designing a crypto checkout flow is the essential first step in building this professional bridge between innovative financial technology and institutional reliability. You’ve seen how a unified architecture ensures that your online data remains synchronized with your physical retail operations, creating a truly omnichannel business model.

Pallapay provides the robust infrastructure needed to facilitate this evolution. As a regulated MSB in the USA and Canada, we offer the security and compliance required for large-scale operations. Our ecosystem supports global settlements in over 180 countries and includes a Red Dot Award-winning POS system for your physical storefronts. This comprehensive approach allows you to focus on your core business while we handle the background mechanics of secure, real-time conversions. Integrate the Pallapay Payment API today to secure your place in the inevitable global evolution of commerce. Your business is ready for the next level of financial efficiency.

Frequently Asked Questions

How long does it take to integrate crypto payments on a website?

Integration time varies from minutes to days based on your specific technical approach. No-code plugins offer immediate activation for standard e-commerce stores; however, designing a crypto checkout flow with a custom API provides the scalability required for enterprise operations. This flexibility allows you to choose the implementation speed that matches your current resource availability. Most merchants find they can go live with basic functionality in under an hour.

Do I need to hold cryptocurrency on my balance sheet to accept it?

You don’t need to hold cryptocurrency on your balance sheet to accept it as a payment method. Most professional gateways offer automated fiat settlement that converts digital assets into USD, EUR, or other local currencies immediately at the point of sale. This approach eliminates balance sheet volatility and simplifies your tax reporting by treating the transaction like a standard fiat sale. It’s an efficient way to modernize your payment stack.

What are the transaction fees for crypto payments compared to credit cards?

Crypto transaction fees are typically lower than the 3% average associated with traditional credit card processing. By reducing the reliance on legacy banking intermediaries and complex settlement networks, digital payments provide a more cost-effective alternative for global commerce. This reduction in overhead helps merchants preserve their profit margins on every international sale. Lower fees mean your business retains more revenue without sacrificing the speed of transaction confirmation.

Is it safe to accept Bitcoin and USDT on an e-commerce store?

Accepting Bitcoin and USDT is safe when using a gateway that prioritizes institutional-grade security and regulatory compliance. The permanent nature of blockchain records removes the threat of chargeback fraud; this is a significant advantage over traditional credit card systems. Designing a crypto checkout flow through a regulated provider ensures your business stays aligned with the latest global financial standards. It provides a secure environment for both your store and your customers.

Can I automatically convert crypto payments to USD or EUR?

You can automatically convert digital payments to major fiat currencies like USD, EUR, or GBP using an instant settlement feature. This tool locks in the exchange rate the moment the customer completes the transaction at your checkout. It ensures you receive the exact fiat amount regardless of any subsequent market fluctuations or price swings. This functionality provides the stability needed to manage a predictable and reliable business cash flow.

How do I handle customer refunds for crypto transactions?

Refunds are typically processed based on the original fiat value of the transaction rather than the specific amount of crypto sent. This practice protects your business from asset price increases that might occur after the purchase was finalized. Most professional gateways provide a dedicated merchant dashboard to manage these payouts efficiently and transparently. Clear communication with your customers about this policy helps maintain trust and prevents disputes during the return process.

Which cryptocurrencies should my business accept in 2026?

Your business should prioritize high-liquidity assets like Bitcoin, Ethereum, and stablecoins such as USDT in 2026. Stablecoins are particularly effective for everyday commerce because they mirror the value of traditional fiat currencies and minimize price risk. Offering a mix of these assets ensures you reach the widest possible demographic of digital wallet holders globally. This variety allows your customers to choose the asset that best fits their personal financial preferences.

Do I need a special bank account to receive fiat settlements from crypto sales?

You don’t need a special bank account to receive fiat settlements from your crypto sales. Standard business bank accounts are fully compatible with the fiat transfers initiated by your payment gateway provider. The gateway acts as the professional bridge; it converts the crypto and sends the resulting fiat via standard bank transfer rails. This ensures that your digital revenue integrates seamlessly with your existing financial infrastructure without requiring new banking relationships.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.