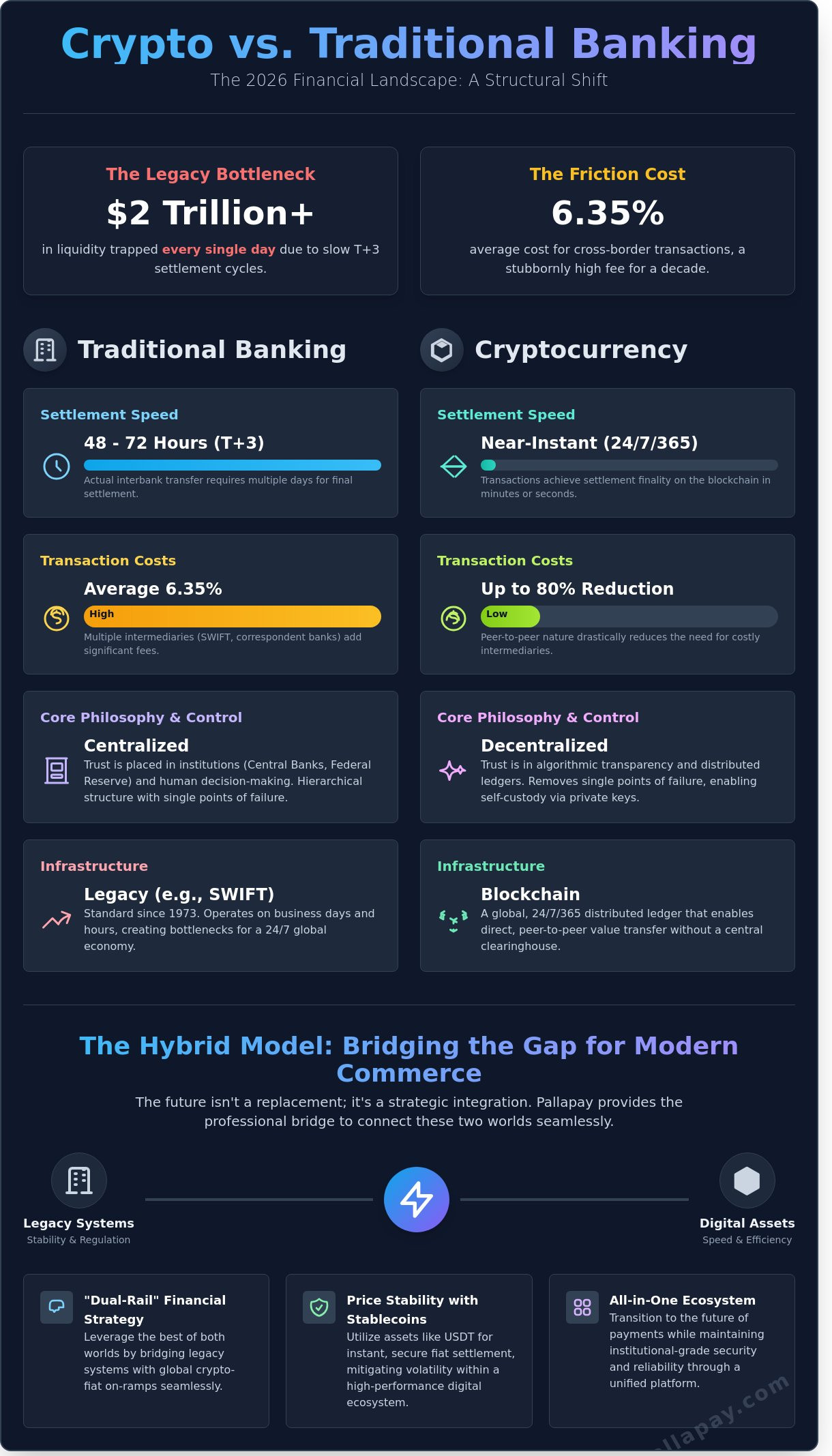

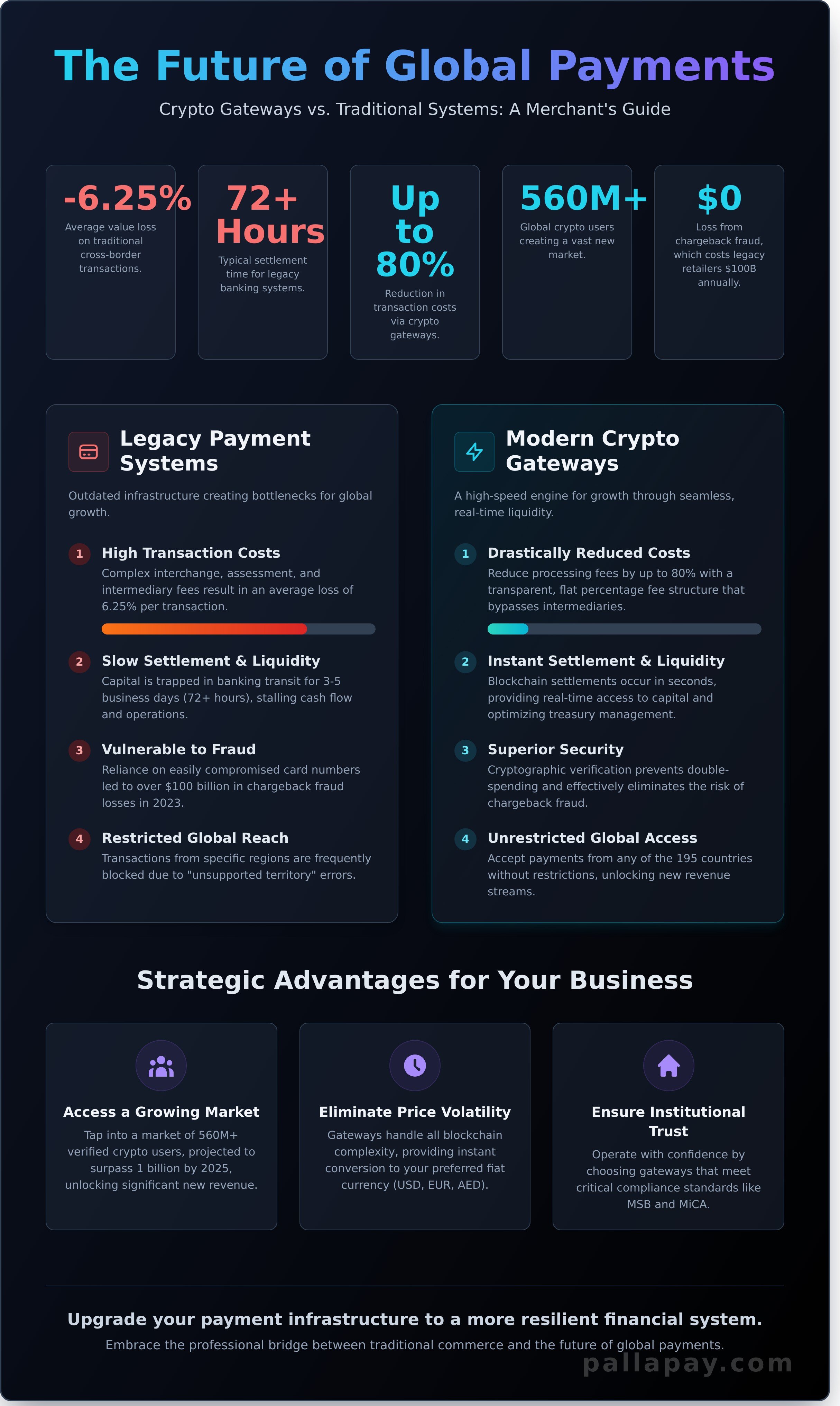

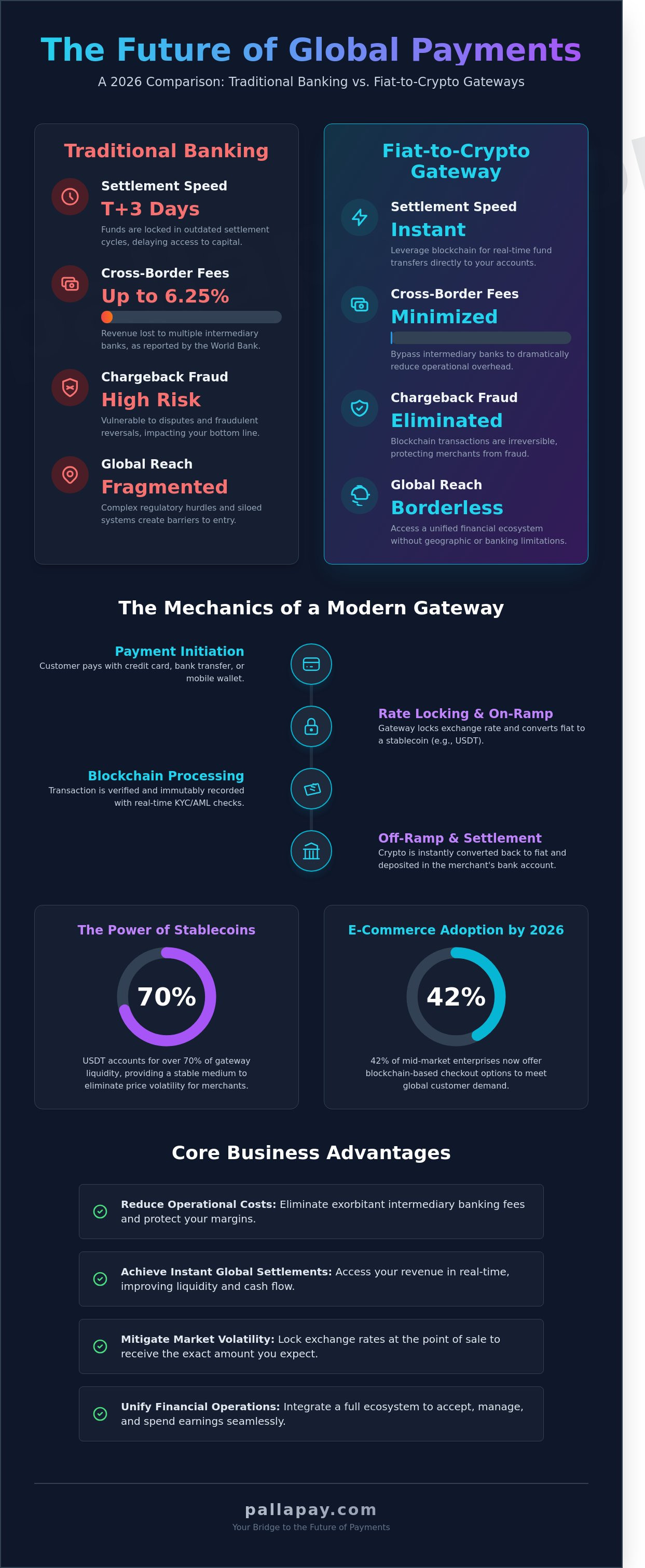

The era of accepting a three day wait for international settlements ended the moment blockchain technology achieved institutional scale. While traditional banking systems still rely on outdated T+3 settlement cycles, a modern fiat to crypto payment gateway allows your business to bypass these legacy bottlenecks entirely. You’ve likely felt the frustration of watching up to 6.25% of your cross-border revenue vanish into intermediary bank fees, a figure the World Bank’s 2023 report highlights as a persistent drain on merchant liquidity.

It’s clear that the friction of high transaction costs and complex regulatory hurdles shouldn’t dictate your growth potential. This 2026 guide provides the roadmap to bridge your existing bank accounts with the speed of decentralized finance. You’ll discover how to achieve instant global settlements, eliminate chargeback risks, and maintain a compliant bridge to the future of payments. We’ll examine the technical infrastructure of liquidity and the strategic shift toward a borderless financial ecosystem that prioritizes your bottom line.

Key Takeaways

- Understand how a fiat to crypto payment gateway serves as the essential bridge between traditional banking and blockchain networks to facilitate seamless global settlements.

- Learn the technical process of locking exchange rates in real-time to protect your business from market volatility during the transaction cycle.

- Discover how to significantly reduce operational costs by eliminating legacy banking fees and the risk of chargeback fraud through secure blockchain processing.

- Identify the critical compliance standards and “all-in-one” features required to choose a secure, institutional-grade provider for your global business needs.

- Explore how integrating a comprehensive ecosystem allows you to spend business earnings instantly via specialized Mastercard solutions, unifying your financial operations.

What is a Fiat-to-Crypto Payment Gateway in 2026?

A fiat to crypto payment gateway functions as the sophisticated bridge between traditional banking systems and decentralized blockchain networks. It allows businesses to accept digital assets while managing their books in local currencies like USD, EUR, or AED. This infrastructure isn’t just a simple converter anymore; it’s a comprehensive financial engine. By early 2026, these gateways have transitioned from niche experimental tools into essential components for global e-commerce, where 42% of mid-market enterprises now offer blockchain-based checkout options. Unlike the fragmented tools of the past, a modern fiat to crypto payment gateway operates as a unified financial engine that handles compliance, security, and settlement in real time.

The core utility lies in its dual nature. It manages the complex “heavy lifting” of converting government-issued money into digital tokens and vice versa. While a simple “buy” widget might suffice for an individual user, a professional merchant processor provides a full-scale API. This integration ensures that a business can scale without worrying about the underlying volatility of the crypto market. It transforms a volatile asset into a stable, usable form of capital for the merchant.

The Evolution of Digital Payment Bridges

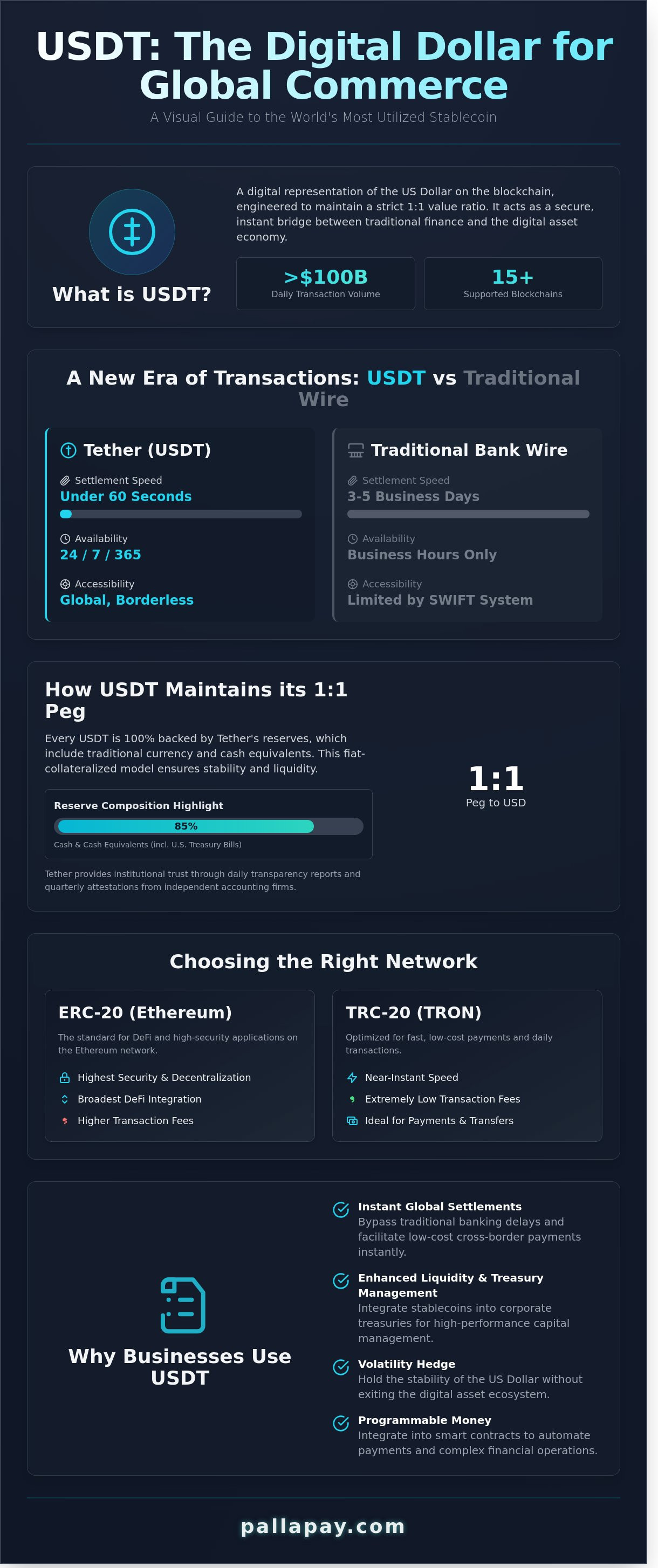

Standards in 2026 differ drastically from the high-friction converters used in 2021. Early systems often required 24 to 48 hours for verification and settlement. Today, the industry has shifted toward instant processing. Stablecoins, specifically USDT, play a pivotal role here. USDT accounts for over 70% of gateway liquidity, providing a stable medium that eliminates the price swings typically associated with Bitcoin or Ethereum. Businesses are moving away from “crypto-only” solutions because they don’t want to hold volatile assets on their balance sheets. Hybrid models are the new standard. These models allow a customer to pay in Bitcoin while the merchant receives an instant settlement in their local fiat currency, combining blockchain efficiency with institutional reliability.

On-Ramp vs. Off-Ramp: Understanding the Flow

The gateway operates through two distinct channels that ensure money moves seamlessly across the digital divide. The customer-facing on-ramp allows a buyer to use a debit card, credit card, or bank transfer to purchase the crypto needed for a transaction. This process happens behind the scenes in seconds. The merchant-facing off-ramp is where the business realizes its profit. It involves taking the received crypto and converting it back into fiat for bank deposit or operational use. Reliability in this flow depends on liquidity providers. By maintaining deep pools of capital, a gateway ensures that conversion rates remain locked the moment a customer clicks “pay.” This prevents slippage and ensures the merchant receives the exact amount expected.

- On-Ramp: Converts fiat into digital assets to initiate a transaction.

- Off-Ramp: Converts digital assets back into fiat for business settlement.

- Liquidity: Ensures instant conversion without price drops.

- Settlement: The final transfer of funds into a merchant’s traditional bank account.

The Future of Payments is defined by this lack of friction. Merchants no longer need to be blockchain experts to benefit from global reach. They simply need a partner that provides the professional infrastructure to bridge the old world with the new.

The Mechanics of Fiat-to-Crypto Processing

A fiat to crypto payment gateway functions as a high-speed financial bridge; it translates traditional currency into digital assets within seconds. This process is a logical sequence designed to eliminate technical friction for the end-user while maintaining institutional-grade security for the merchant. By automating the conversion path, businesses can accept global payments without managing the underlying blockchain complexities themselves.

- Step 1: Payment Initiation. The customer selects their preferred payment method, such as a credit card, instant bank transfer, or a mobile wallet. In 2026, mobile wallet adoption has reached over 60% of the global consumer base, making multi-channel support essential.

- Step 2: Rate Locking. To prevent losses from market volatility, the gateway locks the exchange rate for a specific window. This ensures the merchant receives the exact value expected, regardless of price fluctuations during the transaction.

- Step 3: Automated Verification. Integrated KYC and AML protocols scan the transaction in real-time. This compliance layer is essential for institutional reliability and protects the business from fraudulent activity.

- Step 4: Instant Settlement. The gateway completes the conversion and routes the funds. The merchant receives the assets in their digital wallet or chooses to move them via fiat settlement services to their local bank.

Integration Methods: API and Widgets

Modern gateways offer flexible deployment options to suit different business scales. Small retail websites often opt for “no-code” widgets. These are plug-and-play solutions that require zero development time and provide a secure, hosted checkout page. For enterprise-level customization, a payment API provides the necessary flexibility. It allows businesses to build a bespoke checkout experience that mirrors their brand identity perfectly. Maintaining a seamless UI/UX is vital; a 2025 industry study showed that inconsistent checkout flows lead to a 32% increase in cart abandonment. Professional gateways handle the heavy lifting of backend logic while keeping the frontend interface clean and intuitive.

Real-Time Liquidity and Exchange Rates

Reliable gateways source liquidity from multiple institutional exchanges simultaneously to ensure the best possible rate. This multi-source approach minimizes “slippage,” which is the difference between the expected price and the executed price. Top-tier providers aim for slippage rates below 0.1% even for large volume orders. The term “Instant” serves as the anchor of modern commerce. It represents the shift from legacy T+3 settlement cycles to immediate global value transfer. By utilizing a robust fiat to crypto payment gateway, merchants can access the future of payments where capital moves at the speed of the internet. This efficiency allows businesses to reinvest their revenue faster, accelerating growth in a competitive global market.

Strategic Benefits of Moving Beyond Traditional Gateways

Traditional payment rails are becoming a bottleneck for modern enterprises. By integrating a fiat to crypto payment gateway, merchants bypass the high costs and slow speeds of legacy banking. Legacy systems typically demand a 3% to 5% commission on every transaction. Blockchain alternatives often lower these fees to under 1%, which directly boosts profit margins for high-volume businesses. This shift isn’t just about saving money; it’s about reclaiming control over your revenue streams.

Chargeback fraud caused $100 billion in losses for merchants globally in 2023. This is a primary pain point that traditional credit card processors fail to solve. Cryptocurrency transactions are cryptographically secured and irreversible. Once a customer completes a payment, the funds are final. There’s no middleman to reverse a transaction after you’ve shipped the product. This finality provides a level of financial certainty that credit cards simply cannot match.

Expanding into new territories no longer requires the administrative burden of opening local bank accounts in every country. A single gateway allows you to accept payments from any customer with a digital wallet, regardless of their geographic location. This accessibility is one of the core strategic benefits of accepting cryptocurrency for long-term growth in the 2026 economy.

Instant Global Settlements

Banking cycles often operate on a T+3 basis, meaning your funds are locked for 72 hours or more. High-volume retail and gaming industries require faster liquidity to maintain operational momentum. Blockchain technology enables settlements in minutes rather than days. By utilizing fiat settlement options, businesses receive their local currency quickly while avoiding the price swings of the digital asset market. It’s the most efficient way to manage cash flow in a 24/7 global market.

Security and Fraud Prevention

Security is built into the protocol, not added as an afterthought. Every transaction is a final, verified event on a public ledger, making identity theft and payment spoofing nearly impossible. Gateways serve as a protective buffer, shielding merchant bank accounts from direct exposure to the crypto ecosystem. These platforms also integrate automated AML monitoring that satisfies 2026 financial regulators. You get the benefit of disruptive technology backed by institutional-grade compliance and safety protocols.

- Reduced Overhead: Transaction costs drop by up to 80% compared to traditional processors.

- Zero Chargebacks: Eliminates the risk of friendly fraud and forced reversals.

- Borderless Trade: Sell to anyone, anywhere, without local banking infrastructure.

- Enhanced Liquidity: Move from multi-day waiting periods to near-instant capital access.

How to Choose a Compliant Gateway Provider

Selecting a fiat to crypto payment gateway requires a rigorous evaluation of technical infrastructure and legal standing. You aren’t just choosing a software tool; you’re selecting a financial partner that bridges traditional banking with digital assets. Merchants should consult this guide on choosing a gateway to understand the specific criteria necessary for long-term scalability. A provider’s ability to handle high-volume liquidity while maintaining instant settlement is the hallmark of institutional-grade service. You need a partner that views compliance as a foundation, not an afterthought.

Regulatory Compliance and MSB Status

Trust begins with licensing. Prioritize providers that maintain official Money Services Business (MSB) registrations in major jurisdictions like the United States and Canada. This status ensures the provider adheres to strict anti-money laundering (AML) protocols. Regional expertise is equally vital. For example, a crypto payment gateway in Dubai must navigate specific VARA (Virtual Assets Regulatory Authority) frameworks to ensure local compliance. The right provider manages the complex KYC (Know Your Customer) requirements for your end-users, protecting your business from legal friction. They handle the heavy lifting of identity verification, so you focus on growth.

Support and Reliability

Global markets never close, and your infrastructure shouldn’t either. Your gateway must offer 24/7 technical support to address issues across different time zones. Reliability is measured by a 99.9% uptime guarantee and access to redundant liquidity sources. This redundancy prevents transaction failures during periods of high market volatility. A sophisticated merchant dashboard is non-negotiable for 2026. It must provide real-time reporting and automated tax reconciliation tools. This level of transparency eliminates hidden network or gas surcharges, ensuring the fee you see is the fee you pay. Efficiency drives profitability in the digital age.

A truly all-in-one ecosystem supports every touchpoint of your business. Whether you need a crypto POS machine for physical retail or a robust API for ecommerce, the integration must be seamless. This versatility allows you to accept payments via web, mobile, or physical card without switching providers. It’s about creating a unified financial experience that scales with your ambition. By consolidating these services, you reduce technical debt and simplify your financial operations.

This concept of a cohesive, all-in-one platform is a major trend in the broader payment processing industry. Providers like Strictly specialize in creating this kind of unified omni-channel experience, helping businesses manage web, mobile, and in-person sales seamlessly.

Ready to integrate the future of payments into your business model? Explore our professional fiat settlement solutions today.

Implementing the Pallapay Ecosystem for Your Business

Pallapay functions as the Global Enabler for enterprises ready to master the digital economy. We offer a sophisticated bridge between traditional banking and blockchain innovation. By integrating our fiat to crypto payment gateway, your business secures a competitive edge in a market where a growing percentage of global consumers now prefer digital asset transactions. Our ecosystem transforms crypto-receipts into usable capital. The Pallapay Mastercard allows you to spend business earnings instantly at millions of global merchants. You don’t have to wait for traditional bank clearances to access your funds. This is the professional standard for liquidity in the modern era.

Your physical and digital sales channels shouldn’t operate in silos. The Crypto POS machine unifies your revenue streams, allowing retail managers to accept digital payments as easily as credit cards. This hardware is designed for the modern storefront, providing a secure and regulated way to handle transactions. It’s about providing choice to your customers while maintaining the stability of your balance sheet. Whether you are operating a boutique or a multi-national retail chain, the integration is seamless. We handle the heavy lifting of the technology so your staff can focus on the customer experience.

A Unified Merchant Dashboard

Visibility creates confidence. Our dashboard provides a single point of truth for all cross-border sales, settlements, and card balances. You can generate instant reports for tax compliance or internal audits with a few clicks. This level of transparency is essential for maintaining institutional financial reliability. For organizations with complex structures, the platform supports multiple user permissions. This ensures your accounting team has the data they need while your security protocols remain intact. It is an all-in-one destination for your crypto-financial needs.

From Integration to First Settlement

Efficiency is our priority. The setup for the Pallapay API and Merchant account is streamlined to get you operational quickly. You select your settlement currency, such as USD, EUR, or AED, to ensure your liquidity remains predictable. For corporate clients moving significant volume, our global OTC desks offer deep liquidity and institutional-grade execution. We manage the underlying blockchain architecture, leaving you free to drive your business growth. Getting started with a secure, regulated account today means you are prepared for the future of payments. The process is direct, benefit-driven, and built for scale.

- Instant Access: Spend earnings immediately via the Pallapay Mastercard.

- Global Reach: Settle in major fiat currencies including USD, EUR, and AED.

- Institutional Security: Operate within a regulated, secure financial environment.

- Omnichannel Readiness: Connect online gateways with physical POS hardware.

Pallapay represents more than just a tool; it is a visionary partner for your financial evolution. By bridging the gap between fiat and crypto, we provide the stability your business requires to thrive. Every transaction is a step toward a more efficient, borderless future.

Master the Future of Global Commerce

Integrating a fiat to crypto payment gateway isn’t just a technical upgrade; it’s a strategic move to capture a market of over 420 million digital currency users worldwide. By 2026, the ability to accept diverse payment forms will separate industry leaders from those left behind. Merchants today require more than just a processor. They need a partner that eliminates the standard 72 hour settlement wait times and provides instant access to capital. Moving your operations onto a blockchain-backed infrastructure allows you to bypass the inefficiencies of legacy banking while reaching customers in 180 countries.

Pallapay provides this institutional-grade stability through our status as a regulated MSB in the USA and Canada. We’ve designed our ecosystem to handle the heavy lifting of compliance and technical integration so you can focus on expansion. You’ll benefit from a secure, all-in-one platform that turns the complexity of digital assets into a standard business operation. It’s time to bridge the gap between traditional finance and the decentralized economy with a visionary partner.

Scale your business globally with Pallapay’s secure payment gateway and start your journey toward borderless growth today.

Frequently Asked Questions

What is the difference between a crypto gateway and a standard payment processor?

Crypto gateways bridge the gap between blockchain networks and traditional banking, while standard processors handle fiat-only networks like Visa or Mastercard. Traditional systems rely on centralized bank ledgers that often take 3 to 5 days to clear. A fiat to crypto payment gateway utilizes decentralized ledgers to facilitate instant settlement and global accessibility. This removes the friction found in legacy systems and provides a more efficient financial infrastructure for modern commerce.

Is it legal for my business to use a fiat-to-crypto payment gateway?

Using a crypto gateway is legal in over 130 countries, provided the business complies with local AML and KYC regulations. In the United States, FinCEN classifies these service providers as Money Services Businesses. Merchants must verify that their chosen provider holds the necessary licenses for the specific jurisdictions where they operate. This ensures all financial activities remain within the bounds of international law and institutional standards, protecting the business from regulatory risk.

How much are the typical transaction fees for fiat-to-crypto processing?

Typical transaction fees for these services range from 0.5% to 2% per transaction, based on 2024 industry benchmarks. This is significantly lower than the 3% or 4% often charged by credit card networks for international sales. Businesses also avoid the hidden costs of currency conversion and traditional wire fees. These savings directly impact the bottom line by preserving higher profit margins on every global transaction processed through the gateway.

Can I receive fiat currency in my bank account if the customer pays in crypto?

Yes, you can receive fiat currency directly into your bank account through an instant conversion process. The gateway captures the crypto at the current market rate and settles the equivalent amount in USD, EUR, or AED. This eliminates the risk of price volatility for the merchant. It’s a seamless way to embrace the future of payments without the need to hold digital assets on your corporate balance sheet.

What is MSB registration and why should I look for it in a provider?

MSB stands for Money Services Business, which is a legal designation required by FinCEN for entities that transmit or convert currency. Providers with this registration adhere to strict anti-money laundering protocols and regular audits. Choosing an MSB-registered partner protects your business from legal risks and ensures institutional-grade security. It’s a hallmark of a reliable partner that prioritizes regulatory compliance and global trust in every transaction.

How long does it take to integrate a crypto payment gateway into my website?

Integration typically takes between 24 hours and 5 business days, depending on the complexity of your current digital infrastructure. Most modern providers offer plug-and-play extensions for platforms like Shopify or WooCommerce that can be activated in minutes. For custom enterprise solutions, developers use robust APIs to create a tailored checkout experience. This rapid deployment allows businesses to scale their global reach without facing extensive technical delays or downtime.

Are crypto payments subject to chargebacks like credit cards?

No, crypto transactions are final and immutable once they’re confirmed on the blockchain. This eliminates the risk of fraudulent chargebacks, which cost global merchants an estimated $100 billion in 2023. While you can still issue manual refunds to maintain customer satisfaction, the power to reverse a transaction doesn’t rest with a third-party bank. This provides merchants with absolute certainty and significantly improved cash flow management.

Does the customer need to own crypto to use a fiat-to-crypto on-ramp?

No, customers don’t need to own digital assets beforehand to use a fiat-to-crypto on-ramp. They can use their standard credit card or bank transfer to purchase the required amount of crypto at the point of sale. The gateway handles the conversion instantly, making the process as simple as a traditional online purchase. It’s an all-in-one solution that bridges the gap for users who are new to the digital economy.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.