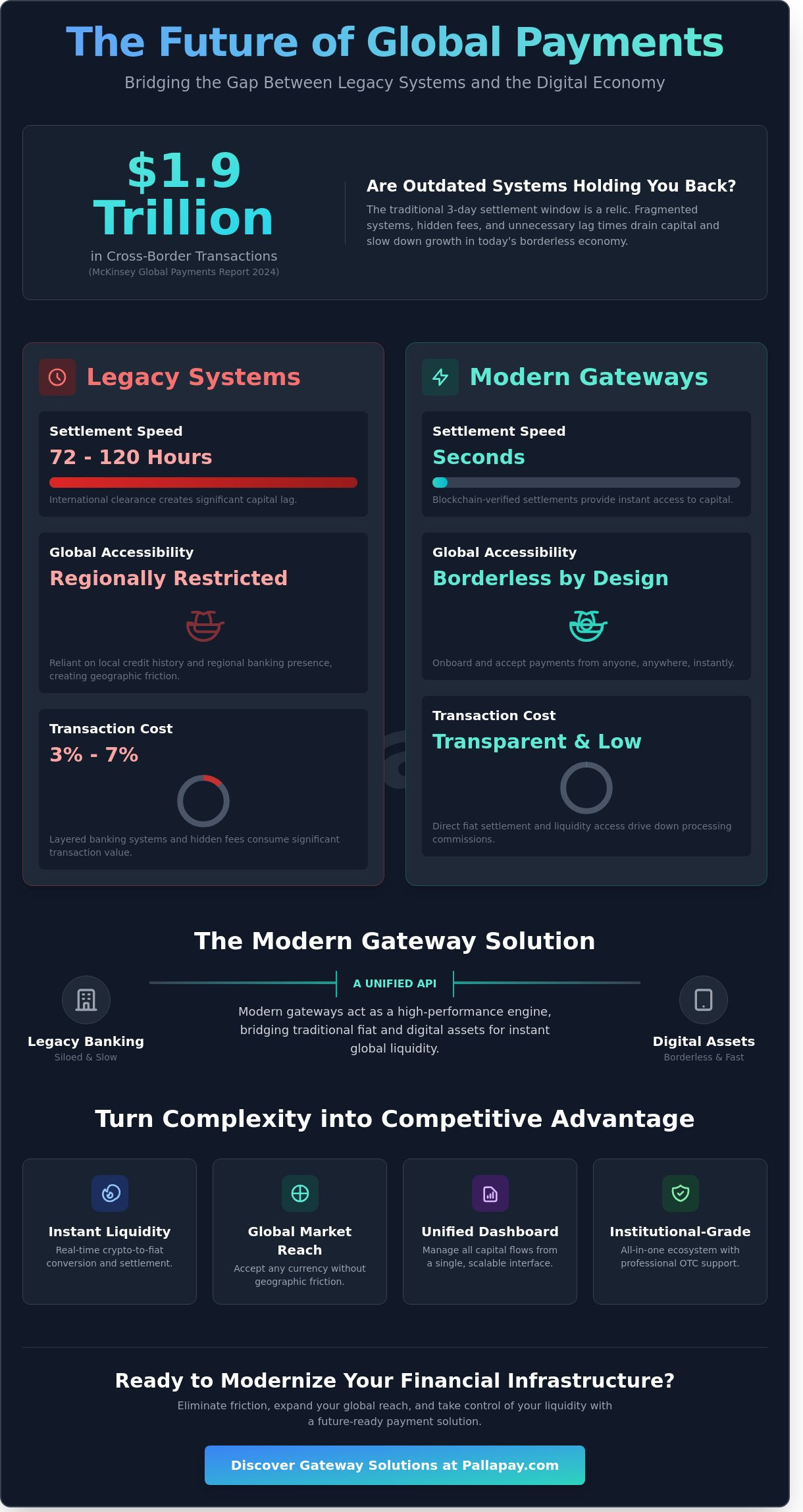

By 2026, the traditional three day settlement window will be viewed as a financial relic. While the 2024 McKinsey Global Payments Report highlighted that cross-border transaction volumes reached $1.9 trillion, many enterprises still struggle with fragmented systems that drain capital through hidden fees and unnecessary lag times. You likely feel the daily friction of managing separate silos for traditional banking and digital assets, especially when your expansion depends on rapid, reliable liquidity. It’s clear that the old ways of moving money can’t keep pace with a borderless economy, and finding efficient gateway financial solutions is now a requirement for survival.

This guide demonstrates how modern financial infrastructure bridges the gap between legacy systems and digital assets for the future of payments. You’ll discover how to transition from complex, slow settlement processes to a unified environment that offers instant settlement in fiat and absolute control over global liquidity. We’ll preview the technical shift toward scalable dashboards that simplify crypto-fiat integration, allowing your business to expand without the heavy lifting of legacy banking constraints. This is the roadmap for turning technological complexity into a clear competitive advantage.

Key Takeaways

- Understand how modern infrastructure connects global liquidity to your business, moving beyond legacy systems to embrace the future of payments.

- Learn the technical mechanics behind fiat-to-crypto bridging that allow for secure, real-time conversion of digital assets into local currency.

- Discover how to eliminate transaction friction and expand your global market reach by instantly accepting payments in any currency.

- Master the criteria for selecting gateway financial solutions that align with your business goals, focusing on optimized fee structures and geographic coverage.

- Explore the advantages of an all-in-one financial ecosystem that provides instant USDT-to-fiat conversion and professional OTC support for institutional growth.

What Are Gateway Financial Solutions in the 2026 Digital Economy?

The 2026 digital economy requires more than simple transaction processing; it demands a sophisticated infrastructure that links merchants directly to global liquidity pools. While historical references to gateway financial solutions often pointed toward 20th-century auto lending models, the modern definition has pivoted entirely. Today, these solutions represent the essential bridge between merchant storefronts and institutional-grade financial tools. This shift ensures that even small-scale enterprises can access the same settlement speeds as global conglomerates.

A modern Payment service provider functions as a global enabler. It removes the friction inherent in traditional banking by providing a unified entry point for diverse capital flows. By 2026, the integration of blockchain technology has made cross-border efficiency a standard requirement rather than a premium feature. Businesses don’t accept the limitations of siloed financial systems anymore. They seek an all-in-one ecosystem that handles everything from crypto-fiat conversion to instant liquidity management. This is the core of modern gateway financial solutions, where technology handles the heavy lifting of global commerce.

The Evolution of Financial Gateways

The transition from 1995-era credit models to 2026-style instant settlement marks a total paradigm shift. Early financial solutions focused on localized credit scoring and manual verification. Digital assets have completely rewritten this playbook. Modern gateways prioritize real-time verification and decentralized security protocols. This evolution has moved the industry away from fragmented service providers toward comprehensive platforms. These ecosystems offer a single payment API that connects a business to the entire global market instantly, ensuring that growth is never hindered by technical debt.

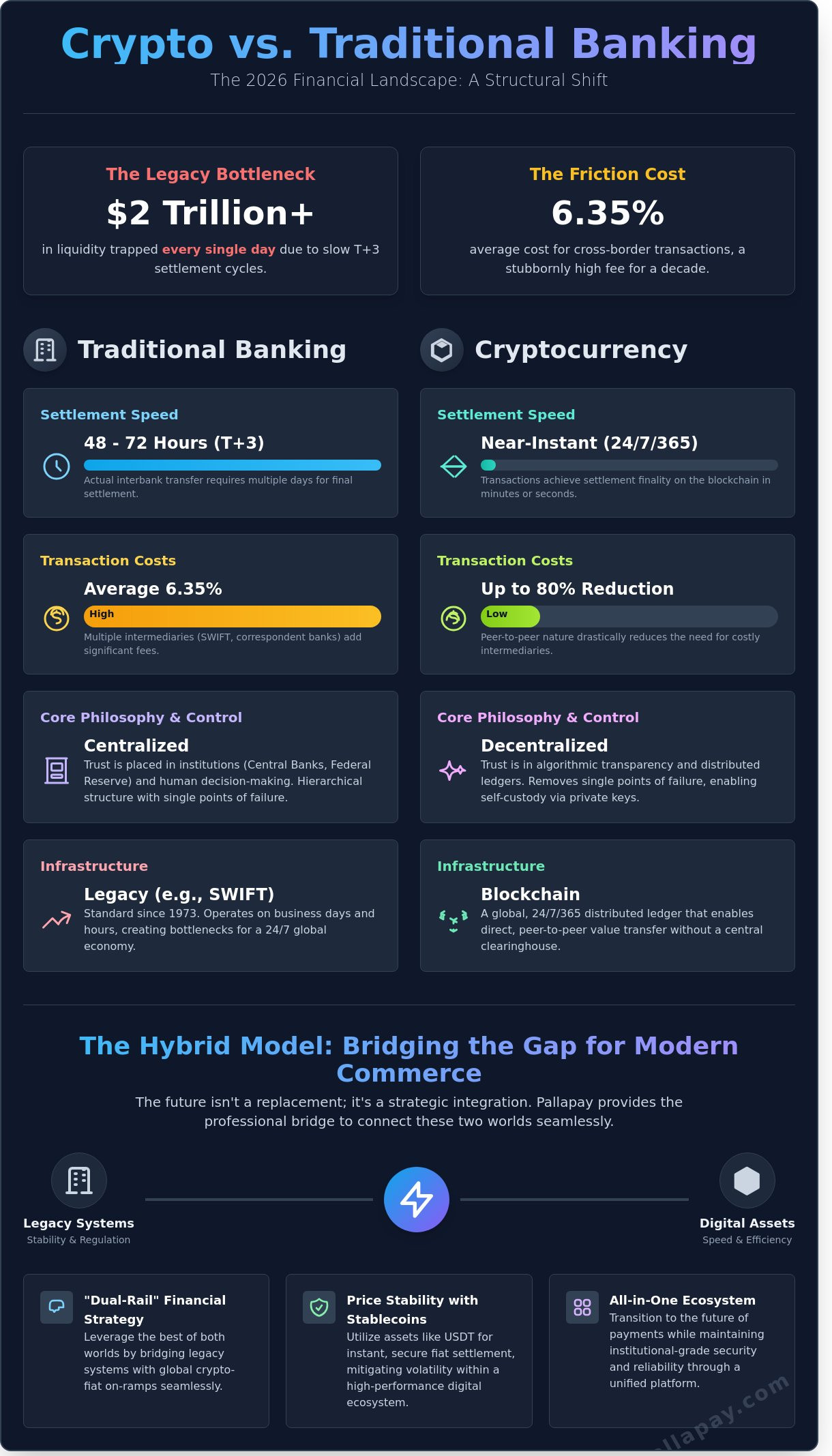

Legacy vs. Modern Gateways: A Comparison

The gap between legacy systems and modern infrastructure is defined by three critical metrics: speed, accessibility, and cost structure. Modern gateways provide a level of utility that 20th-century banks simply cannot match.

- Speed: Legacy bank transfers typically require 72 to 120 hours for international clearance. Modern gateways utilize blockchain-verified settlements to achieve results in seconds, providing instant access to capital.

- Accessibility: Traditional models rely on local credit history and regional banking presence. Modern solutions offer global merchant onboarding, allowing a business in Dubai to accept payments from London or Tokyo without geographic friction.

- Cost: Layered banking fees often consume 3% to 7% of cross-border transaction value. Modern processing commissions are transparent and significantly lower, driven by direct fiat settlement and direct liquidity access.

This efficiency is the hallmark of the Future of Payments. By democratizing access to these tools, fintech leaders ensure that institutional reliability is available to every merchant on the planet. The result is a more inclusive economy where the size of a company doesn’t dictate the quality of its financial tools.

The Technical Architecture of Modern Payment Gateways

Modern gateway financial solutions require more than just a simple connection to a banking network; they demand a high-performance engine capable of processing thousands of transactions every second. A robust architecture in 2026 is defined by its ability to handle immense load without compromising security or speed. This infrastructure relies on a modular design where each component, from the user interface to the ledger, operates independently to prevent systemic failure. To maintain resiliency in digital payment systems, industry leaders now prioritize redundant server clusters and real-time data mirroring across multiple geographic regions.

The mechanism of fiat-to-crypto bridging is the core of this evolution. When a customer pays in cryptocurrency, the gateway must execute a real-time conversion to fiat currency to protect the merchant from market volatility. This process happens in milliseconds. By 2026, API-first design has become the gold standard, allowing businesses to embed these complex financial tools directly into their existing software. Merchants need global accessibility, so the infrastructure must support MSB (Money Services Business) registrations in jurisdictions like the US and Canada. Compliance with FinCEN and FINTRAC regulations ensures that every transaction is backed by institutional-grade oversight.

Fiat Settlement and Liquidity Management

High-volume fiat settlement is achieved through a sophisticated network of liquidity providers. To prevent slippage on large transactions, gateways utilize institutional OTC desks that provide deep liquidity pools. This ensures a 1:1 value preservation during the conversion process, meaning the price the customer sees is the exact amount the merchant receives. Instant settlement has become the baseline expectation for global commerce. If a business processes $500,000 in a single day, the gateway manages the treasury flow behind the scenes to keep capital moving without delays.

Security Protocols and Compliance

Security is the foundation of The Future of Payments. Modern gateways employ AES-256 encryption standards to protect customer data during transit. Compliance is no longer a manual burden; KYC and AML automation now verify identities across 180+ countries in under 60 seconds. To secure the underlying funds, 98% of digital assets are held in cold storage. Multi-sig wallets require multiple authorized signatures before any significant transfer occurs, which effectively eliminates the risk of internal or external theft. This multi-layered approach creates a secure environment where merchants can focus on growth rather than fraud prevention.

Strategic Benefits for Global E-commerce and Retail

Modern commerce demands a borderless approach. Implementing robust gateway financial solutions allows merchants to capture value from a global audience without the traditional hurdles of currency conversion. By 2026, cross-border e-commerce is projected to reach $3.3 trillion according to Statista. This growth relies on the ability to accept payments in any currency, including digital assets, while ensuring immediate liquidity. Businesses that fail to adapt to these shifting consumer preferences risk losing market share to more agile competitors.

Speed defines the winner in the digital economy. We use “Instant” as our rhythmic anchor because delays represent lost revenue. Transaction friction is the primary cause of cart abandonment, which averaged 70% across industries in 2023. Efficient gateways remove these barriers, providing a “problem-solution” flow that satisfies the customer’s need for speed. Real-time reporting through merchant dashboards provides the visibility needed to optimize cash flow, allowing for smarter inventory and staffing decisions based on live data. Secure, branded checkout experiences reinforce customer trust, ensuring that the final step of the buyer journey is as professional as the first.

Empowering Modern E-commerce

Forward-thinking e-commerce businesses are moving toward crypto-integrated gateways to bypass legacy banking delays. Chargeback fraud remains a significant threat, costing merchants nearly $100 billion in 2023 according to Juniper Research. Blockchain-verified finality eliminates this risk by making transactions irreversible once confirmed. Developers use our payment APIs to build custom checkout flows that match their brand identity perfectly. This technical flexibility ensures a seamless transition from cart to completion, making the complex world of crypto-fiat conversion feel like a standard business operation. It’s the definitive way to secure global revenue.

This transition is not limited to consumer retail; specialized B2B providers in the scientific sector, such as peakhaven.com.au, utilize these advanced payment structures to facilitate the global distribution of high-purity research peptides and laboratory supplies without the friction of traditional banking.

Bridging the In-Store Experience

The digital-physical divide is closing rapidly. The adoption of the crypto POS machine allows physical retail locations to accept digital assets at the counter as easily as credit cards. This is particularly vital for luxury retailers and hotels and hospitality groups handling high-value bookings. For example, a luxury hotel can process a $50,000 suite reservation instantly without the 3% to 5% fees often associated with international wire transfers or premium credit cards. These gateway financial solutions simplify the complex logistics of high-net-worth tourism, providing a sophisticated experience for the guest and guaranteed settlement for the provider. It’s a clear manifestation of The Future of Payments in a physical environment.

Implementation: Choosing the Right Gateway for Your Business

Selecting a gateway financial solutions provider is a critical infrastructure decision that dictates your operational scale. In 2026, the distinction between a standard processor and a strategic partner lies in the fee structure. High-volume merchants often find subscription models more predictable for long-term forecasting, while startups might prefer commission-based pricing to align costs with early-stage revenue. Beyond the ledger, geographic presence remains a decisive factor. A provider with physical operations in financial hubs like Dubai or Singapore offers local regulatory alignment and jurisdictional stability that remote-only entities cannot match.

Integration speed defines your time-to-market. Modern payment API solutions allow dev teams to deploy functional checkouts in under six hours, whereas legacy systems often require weeks of manual configuration. This technical agility must be backed by 24/7 institutional-grade support. When a transaction hangs at 3:00 AM in a different time zone, a chatbot isn’t enough; you need immediate access to a dedicated account manager who understands the nuances of cross-border liquidity.

The Checklist for Gateway Selection

Verification starts with compliance. Ensure your partner holds active MSB registrations and regional licenses from authorities like Dubai’s VARA or Singapore’s MAS. Your chosen gateway financial solutions must support a diverse asset pool, including USDT, BTC, ETH, and local fiat currencies, to capture global demand. Evaluate the developer documentation before signing any contracts. A robust API sandbox is essential for testing “The Future of Payments” without risking live capital, ensuring that 99.9% of technical friction is resolved before the first customer arrives.

Avoiding Common Integration Pitfalls

Efficiency is often lost in the fine print of settlement times. Many providers advertise instant processing but hide 48-hour withdrawal delays or tiered withdrawal fees that erode margins. Another frequent oversight is the quality of the merchant dashboard. If your finance team can’t generate real-time reports or manage liquidity with one click, the system becomes a bottleneck. Finally, always stress-test for scalability. A gateway that handles 100 transactions per minute might fail during a 500% traffic surge on peak shopping days, making high-traffic testing a non-negotiable step.

The Pallapay Advantage: An All-in-One Financial Ecosystem

Pallapay serves as the definitive bridge between traditional banking structures and the decentralized future. It eliminates the friction typically associated with digital asset management by providing comprehensive gateway financial solutions that cater to both retail users and institutional entities. The platform facilitates instant USDT-to-Fiat conversion, supported by a global Over-the-Counter (OTC) desk network. This infrastructure ensures that high-volume transactions remain stable and secure, even during periods of market volatility. Businesses no longer need to wait days for settlement; they receive liquidity when they need it most.

Institutional-scale operations require more than just software; they demand a regulated environment where security is the baseline. Pallapay meets this need by adhering to strict compliance standards across multiple jurisdictions, ensuring that every transaction is documented and safe. The Pallapay Mastercard extends this utility into the physical world. It allows users to access instant liquidity, converting digital holdings into spendable currency at millions of points of sale worldwide. This ecosystem doesn’t just store value; it makes value mobile and functional for the modern executive.

Global Presence, Local Expertise

Trust is built through physical presence and transparent operations. Pallapay operates strategic offices in Dubai, NYC, and Singapore to provide localized support for a global client base. This physical footprint allows for unique services, such as the ability to sell USDT for cash in Dubai through secure, face-to-face transactions. By combining global reach with local regulatory expertise, Pallapay ensures every transaction follows the specific legal requirements of the region. It’s a level of accountability that digital-only platforms simply can’t match.

The Future of Payments is Here

The next decade of commerce will be defined by speed and borderless access. Pallapay is actively redefining crypto payment gateways by removing the technical barriers that once hindered mass adoption. The network currently supports merchants in 180+ countries, providing a unified standard for gateway financial solutions in the digital age. This global reach ensures that businesses can scale without worrying about the limitations of legacy banking systems. Every tool in the Pallapay suite is designed for instant execution, reflecting the real-time nature of 2026’s economy.

Integration is the final step toward financial modernization. Join a network that prioritizes security, speed, and institutional reliability. Start your integration today and position your business at the forefront of the financial evolution.

Mastering Global Commerce in the 2026 Digital Economy

Success in the 2026 digital landscape depends on a business’s ability to bridge the gap between traditional fiat and blockchain innovation. Modern gateway financial solutions must provide instant settlement to eliminate the friction typically associated with cross-border trade. By implementing a unified technical architecture, companies can scale operations across 180+ countries while maintaining institutional security. These systems don’t just process payments; they provide the liquidity and stability required for sustainable global growth.

Pallapay delivers this professional bridge as an MSB registered entity in both the USA and Canada. Our award-winning crypto POS and gateway infrastructure empower merchants to accept digital assets with the same ease as standard currency. With physical OTC desks providing real-time support, we handle the technical complexity so you can focus on expansion. It’s the most efficient way to modernize your financial stack and ensure your business remains a leader in an evolving market.

Experience the Future of Payments with Pallapay

We look forward to helping you build a faster, more secure financial future today.

Frequently Questions and Answers

What exactly is a gateway financial solution in a business context?

A gateway financial solution is the digital infrastructure that authorizes and processes payments between a merchant and their customers. In 2026, this technology acts as a bridge that connects traditional banking systems with decentralized blockchain networks. It ensures that sensitive data is encrypted and transmitted securely to the relevant financial institutions. This “all-in-one” approach provides a single point of entry for diverse payment methods, streamlining global commerce for modern enterprises.

How does a crypto payment gateway differ from a traditional merchant account?

A crypto gateway facilitates the transfer of digital assets directly on the blockchain, whereas a traditional merchant account relies on legacy banking rails like ACH or SWIFT. Traditional accounts often involve 3 to 5 intermediaries, which can delay settlement for up to 72 hours. In contrast, a crypto gateway reduces these touchpoints to a single protocol. This efficiency allows for near-instant verification and significantly lower operational overhead for international trade.

Is it secure to use a third-party gateway for high-volume transactions?

Yes, third-party gateways are highly secure because they utilize PCI DSS Level 1 certification and advanced AES-256 encryption. Modern solutions in 2026 incorporate Multi-Party Computation to eliminate single points of failure in private key management. According to the 2025 Cybersecurity Ventures report, businesses using specialized fintech gateways reduced their fraud exposure by 45% compared to legacy systems. This architecture ensures high-volume traffic remains protected against evolving digital threats.

What are the typical fees associated with gateway financial solutions?

Fees for gateway financial solutions generally consist of a per-transaction percentage and a fixed processing fee. While individual provider rates vary, the 2025 Nilson Report indicates that average global processing fees for digital gateways range between 0.5% and 3.5%. Some platforms also apply a monthly maintenance fee or a setup cost for specialized enterprise features. These costs cover the infrastructure, security updates, and regulatory compliance necessary for global operations.

Can I receive fiat currency in my bank account when a customer pays in crypto?

You can receive fiat currency directly into your bank account even if the customer pays with Bitcoin or Ethereum. The gateway acts as a liquidity provider, converting the digital asset to your preferred currency at the current market rate. This instant conversion removes the risk of price volatility for the merchant. It allows businesses to tap into the $2 trillion crypto market without needing to hold or manage digital assets themselves.

What legal regulations apply to payment gateways in 2026?

Payment gateways must comply with the Markets in Crypto-Assets (MiCA) regulation in the EU and updated FinCEN guidelines in the United States. These 2026 standards require strict Know Your Customer and Anti-Money Laundering protocols for every transaction. Gateways are also bound by the Travel Rule, which mandates the sharing of sender and receiver information for transfers exceeding $1,000. These regulations ensure that the Future of Payments remains transparent and legally sound.

How long does it take to integrate a payment gateway API into my website?

Integrating a modern payment gateway API typically takes between 24 hours and 5 business days. Professional platforms provide comprehensive SDKs and documentation that allow developers to connect the service with just a few lines of code. This rapid deployment enables businesses to start accepting global payments almost immediately. The “all-in-one” nature of these APIs means you don’t need to build separate modules for different currencies or regions.

Do I need a separate wallet to use a financial gateway solution?

You don’t necessarily need a separate external wallet because most professional gateways include an integrated custodial solution. This built-in infrastructure manages your incoming funds and facilitates instant withdrawals to your linked bank account. By using a unified platform, you simplify your financial stack and reduce the complexity of managing multiple private keys. It’s a streamlined approach that makes digital finance accessible and efficient for every global merchant.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.