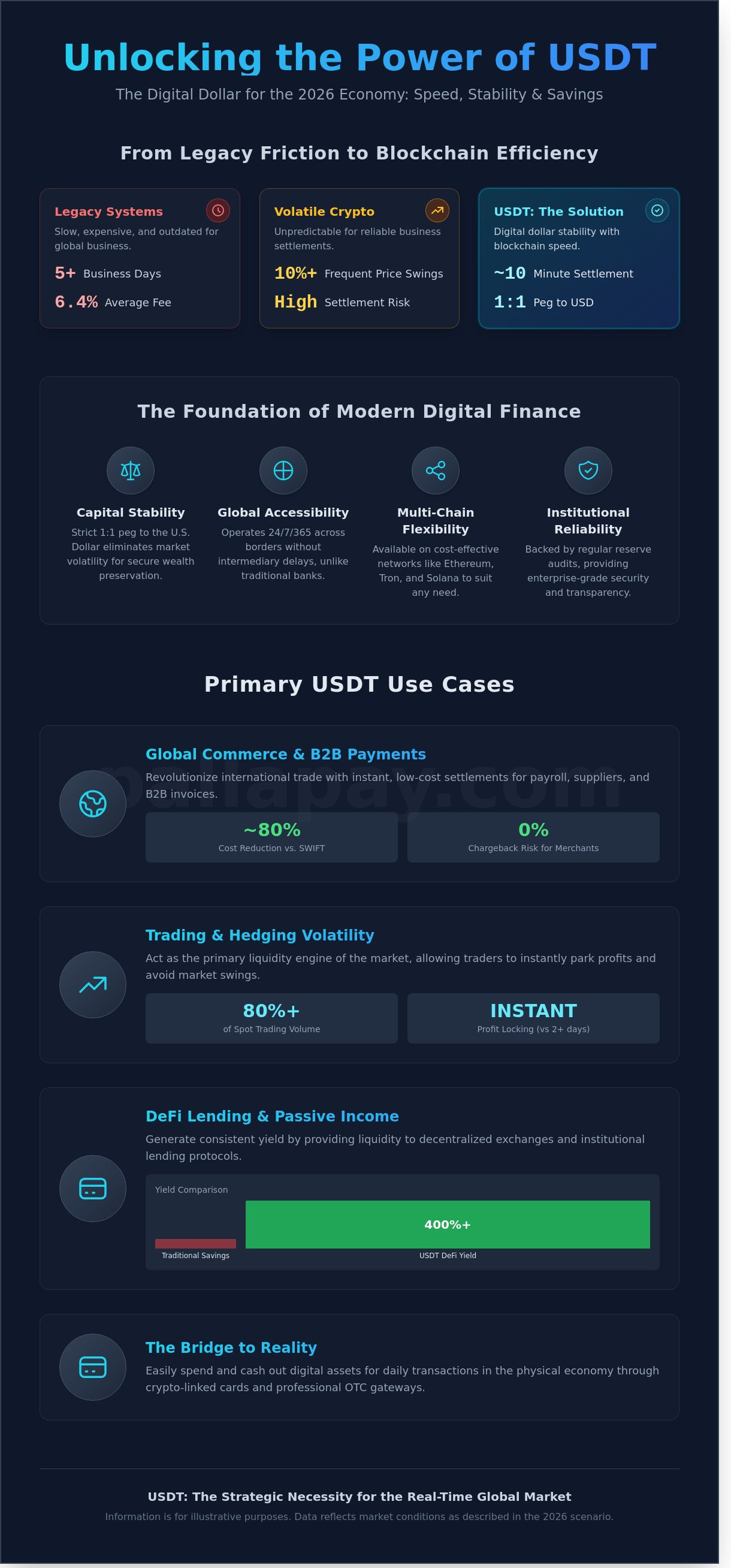

Traditional cross-border wire transfers still take up to 5 business days and cost an average of 6.4% in fees per transaction. In 2026, relying on these legacy systems isn’t just slow; it’s a measurable drain on your company’s bottom line. You’ve likely found that while Bitcoin captures headlines, its frequent 10% price swings make it nearly impossible to use for predictable business settlements. You need the efficiency of the blockchain without the anxiety of market volatility.

Understanding the most impactful usdt use cases allows you to facilitate global commerce, execute instant remittances, and maintain secure wealth preservation within a stable ecosystem. This guide provides a clear roadmap to the future of payments, showing you how to leverage Tether to reduce transaction costs by as much as 80% compared to legacy banking. We’ll explore 10 practical strategies to manage liquidity and spend or cash out your digital assets through professional OTC gateways.

Key Takeaways

- Understand how USDT serves as a stable digital dollar, providing a secure 1:1 peg that eliminates market volatility for reliable wealth preservation.

- Learn to optimize your digital strategy by providing liquidity to DeFi protocols to generate consistent yield in a secure financial ecosystem.

- Explore diverse usdt use cases for modern commerce, including how merchants can eliminate chargeback risks and capture the growing market of global consumers.

- Transition from the inefficiencies of traditional SWIFT transfers to instant, 10-minute global settlements for international payroll and supplier payments.

- Master the process of bridging digital assets to the physical economy by utilizing crypto-linked cards for seamless daily transactions.

What is USDT? The Digital Dollar for the 2026 Economy

USDT is a fiat-collateralized stablecoin engineered to maintain a strict 1:1 peg with the U.S. Dollar. In the 2026 economy, it functions as the critical infrastructure for digital value transfer. While traditional cryptocurrencies often face daily price swings of 10% or more, USDT offers a “Stability Factor” that preserves capital value. It’s the primary liquidity source for the digital asset market; it facilitates trillions in annual transaction volume. By utilizing Tether (USDT), users access a dollar-equivalent asset that moves with the speed of the internet. The token is available across multiple blockchains, including Ethereum, Tron, and Solana, which gives businesses the flexibility to choose the most cost-effective network for their specific needs.

The Evolution of Stablecoins

The industry has moved past the era where stablecoins were only used to park funds between trades. Today, they’re active utility assets. USDT holds its position as the market leader in 2026 because of its deep integration into global trade. Its dominance is supported by a commitment to transparency and regular reserve audits, which provide the institutional-grade security that modern enterprises demand. These developments have significantly widened the scope of usdt use cases, moving the asset from exchange wallets into the hands of everyday consumers and corporate treasuries. The shift represents a fundamental change in how the world perceives digital collateral.

Why USDT is the “Base Asset” of Modern Finance

Traditional banking systems operate on a legacy schedule, often closing on weekends and holidays. USDT operates 24/7, offering a borderless alternative that never sleeps. While a standard SWIFT transfer might require 72 hours to clear, blockchain-based settlements are instant. This efficiency allows a business to manage its fiat settlement needs without the friction of traditional wait times. USDT is also a programmable currency. It can be embedded into smart contracts to automate payments once specific conditions are met. This capability transforms it from a simple medium of exchange into a sophisticated financial tool.

For companies looking to scale, adopting USDT is no longer a niche choice; it’s a strategic necessity for competing in a real-time global market. These usdt use cases demonstrate why the asset is now considered the definitive base asset of the modern financial ecosystem. Key benefits include:

- Instant Settlement: Transactions clear in seconds, not days.

- Global Accessibility: Send and receive value across any border without intermediary delays.

- Programmability: Use USDT within decentralized applications to automate complex business logic.

- Institutional Reliability: Backed by audited reserves to ensure 1:1 redeemability.

This combination of speed and stability makes USDT the preferred choice for merchants and individuals who require the reliability of the dollar with the efficiency of the blockchain.

Trading and Investment Use Cases for USDT

USDT serves as the primary liquidity engine for the global digital economy. By mid-2026, Tether remains the dominant trading pair, accounting for over 80% of all spot trading volume on major exchanges. Its role extends beyond simple transactions; it acts as the functional bridge between volatile crypto assets and institutional-grade stability. Professional traders and retail investors utilize these usdt use cases to maintain capital efficiency in a market that never sleeps.

Hedging Against Market Volatility

Market cycles in 2026 move with unprecedented speed. Traders often encounter 15% price fluctuations within a single hour. USDT provides a secure mechanism to park profits instantly, allowing users to lock in gains without exiting the blockchain ecosystem. This strategy eliminates the 24-hour to 48-hour delay typically associated with traditional bank settlements. It offers a psychological anchor; having a stable unit of account helps investors make rational decisions during periods of extreme fear or greed. When the market stabilizes, they can move back into Bitcoin or Ethereum in seconds.

Passive Income through Staking and Lending

The 2026 DeFi landscape relies on deep liquidity pools to support complex financial products. Users generate consistent yield by lending their USDT to institutional borrowers or providing liquidity to decentralized exchanges. While smart contract risks remain a factor, the rewards for providing USDT liquidity often exceed traditional savings rates by 400% or more. Managing these positions requires a professional interface. Many users rely on the Pallapay Wallet to store their assets securely while exploring diverse yield-generating opportunities across multiple chains.

Beyond passive yield, USDT is the preferred tool for high-frequency trading (HFT) and cross-exchange arbitrage. Arbitrageurs exploit price gaps between global platforms, using USDT’s instant settlement to capture small margins that disappear in milliseconds. This constant movement of capital ensures price parity across the global market.

For users in emerging economies, USDT functions as a critical store of value. In regions where local currency inflation exceeds 40% annually, holding Tether provides a digital dollar equivalent that is easily accessible via a smartphone. It bypasses the restrictive capital controls often found in traditional banking systems, offering a lifeline for wealth preservation. These diverse usdt use cases demonstrate why Tether has evolved from a simple trading tool into a foundational pillar of modern finance.

Effective wealth management starts with the right infrastructure. Consider how a secure digital asset gateway can simplify your daily trading operations and long-term investment strategy.

Business and Retail: Accepting USDT as a Merchant

Consumer behavior has shifted dramatically. By 2026, the number of digital asset users is projected to surpass 1 billion globally, creating a massive demographic of crypto-native shoppers. These individuals seek direct, frictionless payment options that bypass traditional banking delays. For merchants, adopting usdt use cases in retail isn’t just about innovation; it’s about protecting the bottom line. One of the most significant advantages is the total elimination of chargeback fraud. Traditional credit card disputes cost businesses over $100 billion annually. Since Tether transactions are final and immutable on the blockchain, merchants are protected from the “friendly fraud” that plagues standard payment gateways. This security provides a level of institutional reliability that traditional finance struggles to match.

In-Store Payments and Crypto POS Systems

Physical storefronts are rapidly adopting the Crypto POS Machine to bridge the gap between digital wealth and high-street commerce. This hardware functions with the same familiarity as a standard terminal but displays a dynamic QR code for the customer to scan. For Retail Stores and Hotels, the process is seamless and professional. The customer pays in USDT, while the merchant receives an instant settlement in their preferred fiat currency. This setup removes the volatility risk entirely, ensuring that the business receives the exact price listed on the tag without delay. It’s a sophisticated solution for the modern merchant who demands both speed and stability in every transaction.

E-commerce and Global API Integration

Online brands are finding a competitive advantage through a Payment API that automates the entire checkout flow. In the E-commerce sector, traditional processors often take a 3% to 5% cut of every transaction. USDT checkouts reduce these overheads significantly, often costing less than 1%. Because these usdt use cases facilitate instant global transfers, businesses no longer wait 3 to 7 days for international funds to clear. This liquidity allows for faster restocking and more aggressive growth. It transforms the checkout from a hurdle into a streamlined gateway for a global customer base. Pallapay handles the heavy lifting of the technology, ensuring that the future of payments is accessible to every digital brand today. By removing the friction of cross-border currency conversion, merchants can enter new markets with zero local banking infrastructure.

The transition to stablecoin payments represents a fundamental evolution in how value moves. Merchants who integrate these systems now are positioning themselves as leaders in a digital-first economy. They gain access to a global pool of liquidity while benefiting from the security of blockchain technology. This isn’t just a trend; it’s the new standard for global commerce.

Global Remittances and B2B Cross-Border Payments

Traditional banking relies on the SWIFT network, which frequently imposes 3 to 5 day delays on international transfers. These delays often come with hidden intermediary bank fees that can erode up to 7% of the total transaction value. In contrast, USDT provides a 10 minute settlement window that operates 24/7. This speed is critical for businesses managing global supply chains. By utilizing Tether, companies eliminate the volatility of local currencies while ensuring that suppliers receive funds exactly when needed. One of the most impactful usdt use cases in 2026 involves this shift from slow, expensive legacy rails to instant digital liquidity.

The social impact of this technology extends to the individual level. The World Bank reported that the average cost of sending $200 globally reached 6.2% in 2023. USDT reduces these costs to a fraction of a percent. It allows migrant workers to send money home without losing a significant portion of their earnings to predatory fees. This democratization of finance turns a complex international transfer into a simple, secure transaction that happens in real time.

Revolutionizing International Payroll

Remote companies now pay global talent instantly using USDT to bypass the friction of traditional wire transfers. This approach ensures that a developer in Europe or an artist in Asia receives their full salary without the standard 48 hour waiting period. Using regulated gateways helps these businesses maintain tax compliance and provides a clear audit trail on the blockchain. Corporate transfers become transparent and verifiable; this reduces the administrative burden on accounting departments. It’s a system built for the modern, borderless workforce.

Instant Fiat Settlement for Global Trade

High-volume trade requires precision and speed. The Fiat Settlement process allows enterprises to handle large B2B invoices by converting USDT into local bank deposits without the risk of price slippage. For institutional players, accessing an OTC Crypto Exchange is vital for securing deep liquidity during massive transactions. This infrastructure bridges the gap between digital assets and traditional bank accounts. It makes global trade feel as effortless as a domestic transaction.

Ready to accelerate your business operations with the future of payments? Experience instant fiat settlement today.

The Bridge to Reality: Cashing Out and Spending USDT

The ultimate measure of a stablecoin’s value lies in its ability to transition from a digital ledger to the physical world. While early usdt use cases focused primarily on exchange liquidity, the landscape in 2026 centers on direct spending power. Converting Tether into cash or daily goods shouldn’t be a technical hurdle. It’s a standard financial requirement that Pallapay facilitates through a sophisticated suite of tools designed for both speed and reliability. This transition represents the final step of utility, turning digital assets into tangible spending power for everything from corporate investments to personal lifestyle needs.

Selling USDT for Cash in Global Hubs

Professional investors often require immediate access to fiat currency for real estate acquisitions or large-scale business expenses. Traditional banking systems often impose restrictive limits on international transfers, but Pallapay addresses this by offering a secure OTC gateway for high-volume liquidity. In financial centers like the UAE, the ability to Sell USDT in Dubai through physical offices provides a level of trust that digital-only platforms cannot match. These offices handle high-volume settlements in under 10 minutes, offering a secure environment for face-to-face transactions. This model eliminates the uncertainty of peer-to-peer transfers. By providing instant cash liquidity, Pallapay acts as a global enabler for those who need to move between the blockchain and the physical economy without the standard 48-hour banking delays.

The Pallapay Mastercard and Lifestyle Integration

Managing a crypto-centric lifestyle requires tools that feel familiar and efficient. The Pallapay Mastercard bridges this gap by allowing users to spend USDT at any merchant that accepts Mastercard, covering everything from morning coffee to fuel and international flights. This integration removes the friction of manual currency conversion. For those seeking alternative spending routes, the ecosystem includes Gift Cards for major retail, gaming, and travel brands. This provides a versatile, non-banking method to utilize digital assets for everyday needs. Pallapay delivers an all-in-one solution that handles the heavy lifting of technology behind the scenes, ensuring every transaction is seamless and secure. This isn’t just a utility; it’s The Future of Payments, where digital assets and physical reality exist in a single, unified ecosystem.

Mastering the 2026 Global Digital Dollar

The transition toward a digital-first economy is a present-day reality for businesses operating across 180 countries. These usdt use cases demonstrate that Tether has evolved into a critical bridge between traditional fiat and decentralized efficiency. Whether you’re settling B2B invoices with instant finality or managing high-volume liquidity via physical OTC desks in Dubai, Singapore, and Istanbul, the focus remains on frictionless growth. By utilizing a regulated MSB in the USA and Canada, your enterprise gains the security of institutional-grade compliance while bypassing the 5-day settlement delays often found in legacy banking systems.

Success in this landscape requires a partner that handles the technical heavy lifting while you focus on scaling. Pallapay provides the all-in-one ecosystem necessary to transition from speculation to real-world utility. It’s time to embrace the future of payments with a platform built for speed and absolute reliability. You don’t have to navigate this evolution alone when a sophisticated bridge to the new economy is already operational and ready to facilitate your next transaction.

Start your journey with the most secure USDT ecosystem at Pallapay

The global financial landscape is changing fast, and your business is perfectly positioned to thrive in it.

Frequently Asked Questions

What are the most common USDT use cases for individuals in 2026?

Individuals primarily use USDT for cross-border remittances and wealth preservation against local currency devaluation. Data from 2025 indicates that 45% of users in emerging markets leverage Tether to hedge against inflation exceeding 10% annually. These usdt use cases also include instant peer-to-peer transfers that bypass traditional banking holidays. It’s a reliable method to maintain purchasing power while accessing the global digital economy.

Can I pay for my hotel or retail shopping with USDT?

You can pay for travel and retail goods at over 15,000 global merchants that integrated crypto gateways by early 2026. Major booking platforms and luxury retailers now accept Tether through instant POS systems. Pallapay facilitates these transactions by providing a seamless bridge between your digital wallet and the merchant’s settlement account. It’s as simple as scanning a QR code for an instant checkout experience.

Is it legal for businesses to accept USDT payments?

Accepting USDT is legal in over 120 jurisdictions that established clear Virtual Asset Service Provider (VASP) frameworks by 2026. Businesses must comply with local AML and KYC regulations, such as the EU’s MiCA framework which became fully enforceable in late 2024. Using a regulated gateway ensures your business remains compliant while tapping into the $120 billion Tether liquidity pool. It’s a professional way to modernize your financial operations.

How much are the fees for sending USDT across borders compared to banks?

Sending USDT across borders costs between $0.50 and $2.00 on scalable networks like Tron or Polygon, which represents a 95% saving compared to legacy systems. Traditional banks typically charge a flat $35 fee plus a 3% currency conversion spread. Tether transactions settle in under 60 seconds. International bank wires often take 3 to 5 business days to clear, making USDT the superior choice for efficiency.

How can I convert my USDT into physical cash safely?

You can convert USDT to physical cash through licensed OTC desks or specialized crypto ATMs. Pallapay operates secure physical branches where users exchange digital assets for fiat currency in under 15 minutes. This process requires a valid government ID to meet 2026 global regulatory standards. It’s the most reliable method to access liquidity without waiting for the standard 48-hour banking processing windows.

What happens if the USDT peg breaks during a transaction?

If the USDT peg fluctuates by more than 0.5% during a transaction, professional gateways pause the settlement to protect the buyer and seller. Tether maintained its $1.00 peg with 99.9% consistency throughout 2025 due to its audited reserve backing. Modern smart contracts utilize real-time oracle price feeds to ensure the transaction value reflects current market rates. This mechanism prevents financial loss during rare periods of high market volatility.

Do I need a bank account to use USDT for global payments?

You don’t need a traditional bank account to send or receive global payments using Tether. This is one of the most transformative usdt use cases, as it provides financial tools to the 1.4 billion unbanked adults worldwide. A digital wallet and an internet connection are the only requirements for participation. This setup represents the future of payments, allowing users to manage global capital without institutional gatekeepers.

Can I use USDT for high-volume B2B transactions?

USDT is an ideal instrument for high-volume B2B transactions because it offers instant settlement and eliminates the risk of credit card chargebacks. Corporate entities use Tether to move $1 million or more across borders for a fraction of the cost of traditional letters of credit. By using a professional gateway, businesses automate their supply chain payments and improve their cash flow. It’s a sophisticated solution for modern enterprise liquidity management.

Leave a Reply