What if your most illiquid asset could become the fuel for high-velocity global trading in less than twenty-four hours? You likely agree that high-value property sales often feel trapped behind weeks of banking delays and archaic escrow processes that erode your potential returns. A specialized real estate crypto payment gateway solves this by bypassing traditional bottlenecks and securing your capital with institutional reliability.

This article shows you how to leverage these gateways to facilitate high-volume transactions and gain the immediate liquidity needed to enter transformative markets. You’ll learn to move seamlessly from property titles to Gold CFDs and Forex trading, turning stagnant wealth into active growth. We’ll explore the mechanics of instant fiat settlement and the strategic path to diversifying your portfolio into the world’s most liquid commodity and currency markets. By bridging the gap between physical assets and digital speed, you can finally unlock the full potential of your real estate holdings in the 2026 financial ecosystem.

Key Takeaways

- Learn how a professional real estate crypto payment gateway eliminates traditional banking delays by facilitating instant, high-volume property settlements.

- Discover how instant fiat-to-bank conversion protects your capital from market volatility during large-scale asset transfers.

- Understand the strategic process of pivoting illiquid real estate wealth into the high-velocity world of Forex and Gold CFDs.

- Identify the essential role of regulated MSB status and global OTC desks in maintaining institutional-grade security for your transactions.

- Explore how an integrated financial ecosystem can transform your property holdings into a diversified portfolio of liquid global assets.

The Role of Crypto Payment Gateways in Modern Real Estate

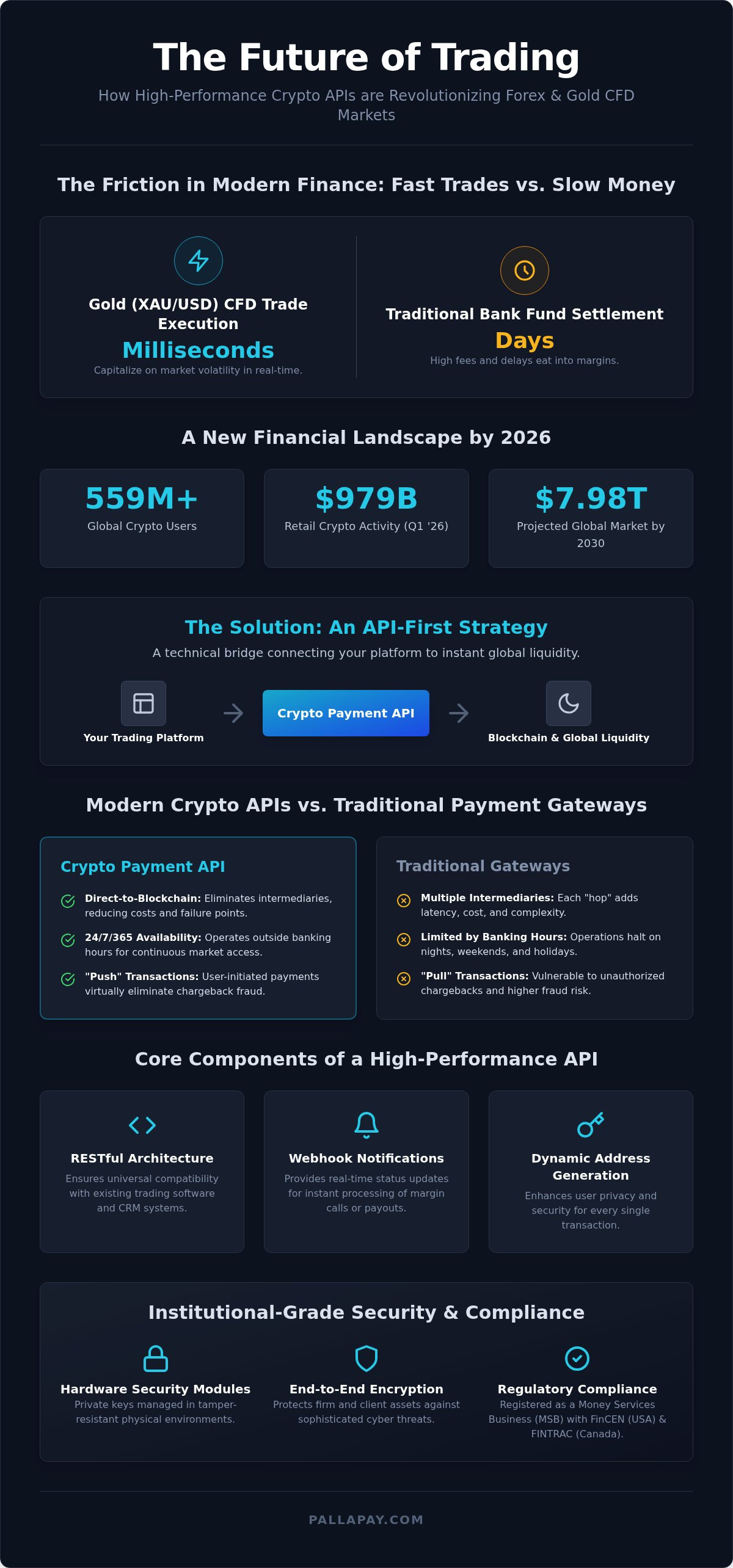

Modern property markets require more than just a basic wallet transfer. A dedicated real estate crypto payment gateway acts as a specialized financial bridge. It isn’t just about moving tokens; it’s about institutional-grade settlement. Traditional banking systems often struggle with the speed requirements of 2026 markets. Cross-border transfers can take days or weeks. This delay is unacceptable when property values fluctuate or when an investor needs to pivot into high-velocity markets like Forex or Gold CFDs.

By 2026, the industry has shifted significantly. Major developers now view crypto not as a niche option, but as a standard requirement. These gateways eliminate “seasoning of funds” hurdles. In traditional mortgages, banks often require capital to sit in an account for months to prove its origin. Using a regulated gateway with robust AML/KYC protocols provides a clear, documented audit trail that satisfies compliance without the unnecessary wait. This efficiency is built on the foundational principles of cryptocurrency and blockchain technology, which allow for transparent and immutable transaction histories.

Addressing the Liquidity Gap in Property Markets

Real estate is traditionally illiquid. You can’t sell a floor of an office building in an afternoon. However, crypto gateways provide an immediate entry or exit point. They reduce the friction of moving capital across borders for international buyers. Stablecoins like USDT are frequently used to maintain value during property negotiations. This ensures the purchase price remains stable even if the broader market shifts. Once the sale is settled, investors often use a crypto offramp to move capital into USD CFD trading or Gold markets for higher velocity growth. This transition from a stagnant physical asset to a liquid trading account can happen in a single business day.

The Advantage for Developers and Agencies

Agencies that adopt this technology attract a new demographic of affluent, crypto-native investors. These are individuals with significant digital wealth looking for tangible assets to balance their portfolios. By using a real estate crypto payment gateway, developers reduce the overhead costs associated with international wire transfers and intermediary banks. They also eliminate the uncertainty of failed bank transfers for high-value sales. This isn’t just a utility; it enhances brand prestige. It positions the developer as a strategic partner capable of handling the complexities of modern, global commerce. This forward-thinking approach turns a simple transaction into a competitive edge in a crowded market.

Essential Features of an Institutional Real Estate Gateway

Institutional property deals aren’t like standard retail purchases; they require a real estate crypto payment gateway capable of handling extreme volume. High-value transactions demand sophisticated processing to prevent slippage. When you’re moving millions in digital assets, even a minor price fluctuation can lead to substantial capital loss. This risk is managed through deep liquidity pools and specialized OTC desks that execute large orders at a locked price. This stability ensures that the agreed-upon sale value is precisely what reaches the final account.

Instant fiat settlement is the second pillar of a professional gateway. Most property sellers need local currency to clear existing debts or reinvest in new projects immediately. A reliable system converts digital assets and initiates a direct fiat settlement to a corporate bank account in record time. This speed prevents capital from being trapped in a volatile state during the closing process. Adhering to IRS guidelines on digital assets ensures that these settlements are fully documented for tax and legal compliance, providing the transparency required for institutional audits.

Security Protocols for Large-Scale Transfers

Large-scale asset transfers require more than just basic encryption. Dedicated OTC desks facilitate the liquidation of high-value property payments, ensuring that market volatility doesn’t impact the transaction outcome. For funds in transit, institutional providers utilize cold storage and multi-signature security protocols to eliminate single points of failure. MSB registration stands as the definitive cornerstone of institutional trust and regulatory accountability in the 2026 financial landscape. These layers of protection ensure that your capital moves safely from the buyer’s wallet to your liquid trading account.

Seamless Integration with Existing Workflows

Operational success depends on how effectively a gateway integrates with your current business tools. High-performance payment APIs allow developers to connect the gateway directly to real estate CRM and accounting software. This automation removes the friction of manual data entry and reduces the potential for human error in high-stakes reporting. Professional merchant dashboards offer real-time tracking, giving you full visibility into every stage of the settlement process. These systems generate compliant crypto-invoices that meet the specific legal requirements of the property sector. By streamlining these background mechanics, you can focus on the strategic pivot of reinvesting your wealth into high-velocity markets like Gold and USD CFDs.

Beyond Bricks and Mortar: Diversifying into Forex and Gold CFDs

Traditional asset management often treats real estate as a final destination. However, the integration of a real estate crypto payment gateway transforms the property sale into a liquidity event with global reach. Once the settlement is complete, the investor isn’t just holding cash; they’re holding fuel for high-velocity markets. This immediate availability of funds is a competitive advantage in a globalized economy where market windows open and close in hours, not months. The speed of crypto-settled funds is the primary driver of this evolution. Traditional banking often traps wealth in a state of in-transit limbo, but a digital gateway ensures that your capital is ready for reinvestment the moment the deed is signed. Understanding how blockchain is used in real estate clarifies how these digital rails provide the necessary speed for modern portfolio management.

The Financial Transformation of the Modern Investor

Transitioning from the slow appreciation of a physical building to the dynamic potential of Forex trading represents a profound financial transformation. While real estate provides stability, CFD trading provides the daily liquidity needed to navigate shifting economic landscapes. This psychological shift from a passive landlord to an active market participant empowers investors to take control of their capital’s velocity. It’s about moving from waiting for growth to generating growth through strategic exposure to currency pairs and commodities. This shift can fundamentally change an individual’s financial life by providing a level of agility that traditional property owners simply don’t possess. Instead of capital being locked in a physical structure, it becomes a versatile tool for wealth generation.

Gold and USD: The Pillars of Global CFD Trading

Gold and USD CFDs offer a unique hedge for real estate investors in 2026. When markets become volatile, these assets provide a secure harbor for liquidated property wealth. There’s a natural synergy between USD-based assets and real estate holdings that sophisticated investors use to balance their risk. Gold remains the ultimate diversifier, especially during periods of global economic uncertainty. CFD trading allows for exposure to gold prices without physical storage burdens, making it an efficient way to diversify without the logistical overhead of bullion. By pairing the stability of gold with the liquidity of USD-based CFDs, you create a balanced portfolio that is both resilient and responsive to global trends. Leveraging these markets allows for a level of portfolio protection that physical assets alone cannot provide.

Strategic Implementation: From Crypto Settlement to Trading Success

Moving from a property sale to active trading requires a methodical approach. The first step involves selecting a regulated real estate crypto payment gateway that offers high-volume OTC capabilities. This ensures that multi-million dollar transactions don’t disrupt the market or suffer from slippage. Once the gateway is secured, the next priority is configuring fiat settlement services to your corporate bank account. This step provides the immediate liquidity needed to fund a trading account without the typical five-day wait associated with international bank wires.

The transition from a physical asset to a liquid trading balance involves a few technical milestones. First, the buyer’s crypto is received and locked at a specific rate. Next, the OTC desk liquidates the asset, and the gateway initiates a transfer to your bank. Finally, you move these funds into a specialized brokerage account to begin trading. This streamlined flow allows you to capitalize on market movements almost immediately after a property sale closes.

Optimizing the Off-Ramp Process

Capital efficiency depends on minimizing conversion fees and slippage. When moving from a property sale into a liquid state, utilizing a professional crypto offramp ensures that you retain the maximum value of your assets. Timing remains critical. Some investors choose to hold USDT briefly to wait for specific market entries, while others move directly into Gold or USD CFDs to capitalize on immediate volatility. This process allows you to turn a static property into a dynamic portfolio of currency pairs and commodities, effectively changing your financial trajectory through active market engagement.

Risk Management in High-Value Diversification

High-value diversification requires a disciplined approach to risk. Moving large sums between real estate and trading accounts demands absolute security, which is why working with a strategic partner is essential. When entering the Forex and Gold markets, setting strict stop-losses and managing leverage are non-negotiable practices. These tools protect your capital from sudden market reversals and ensure that your trading remains a sustainable wealth-building activity.

- Implement multi-signature approval for large outgoing transfers to prevent unauthorized capital movement.

- Diversify capital across multiple currency pairs to avoid over-exposure to a single economic zone.

- Regularly audit capital flows to ensure compliance with global financial standards and tax requirements.

Consulting with experts ensures that your capital flow remains compliant while you pursue the transformative potential of CFD trading. If you are ready to accelerate your progress, you can start your off-ramp process today to unlock new market opportunities.

Pallapay: The Professional Bridge to Global Asset Liquidity

Pallapay serves as the definitive destination for institutional-grade property settlement. We provide the infrastructure necessary to bridge the gap between traditional real estate assets and the high-velocity world of digital finance. As a global industry leader, our ecosystem supports the entire journey from the initial property sale to the final reinvestment in liquid markets. By utilizing a real estate crypto payment gateway with a proven track record, businesses can eliminate the friction of cross-border capital movement. Our reliability is anchored in physical global offices and MSB registrations in the United States and Canada, ensuring that every high-volume transaction meets the highest standards of regulatory accountability.

We empower businesses to accelerate their progress by providing a secure, utility-focused environment. This isn’t just about accepting digital assets; it’s about providing a strategic path to financial evolution. Our platform handles the underlying mechanics of settlement and conversion, allowing you to focus on high-level portfolio management. This institutional reliability instills absolute trust in both developers and their affluent, crypto-native clients.

Integrated Solutions for Real Estate and Beyond

Custom property platforms require flexible, robust technology. Developers can leverage the Pallapay Payment API to integrate crypto acceptance directly into their existing CRM and management software. This automation reduces manual overhead and ensures that every transaction is tracked in real-time through our professional merchant dashboards. Furthermore, utilizing our off-ramp expertise allows for rapid capital redeployment. Our infrastructure manages the background complexity of liquidity pools and OTC liquidation, ensuring that property sellers receive their fiat funds with maximum efficiency and minimal slippage. This integrated approach turns a complex technical process into a standard, effortless business operation.

Starting Your Financial Evolution

The transition from property ownership to active market participation begins with a single strategic choice. Integrating our gateway into your real estate agency or development firm provides the immediate liquidity needed to master the Gold and Forex CFD markets. While real estate offers long-term stability, CFD trading provides the dynamic potential to change an individual’s financial life through daily market engagement. We provide the professional bridge that connects these two worlds, allowing you to move from stagnant assets to high-growth opportunities in USD-based currency pairs and commodity markets. This evolution is not just a tool; it’s an essential component of the modern global economy. If you are ready to transform your transaction model, you should consult with a Pallapay specialist to modernize your transaction infrastructure.

Accelerate Your Financial Evolution with Institutional Liquidity

The landscape of property investment has shifted from stagnant asset holding to high-velocity capital management. You’ve seen how a professional real estate crypto payment gateway serves as the engine for this change, providing the speed and security required for multi-million dollar settlements. By leveraging instant fiat conversion, you can bypass traditional banking friction and move wealth into the most liquid markets on the planet. This strategic pivot into Forex and Gold CFDs doesn’t just diversify your portfolio; it provides the daily liquidity needed to thrive in a globalized economy.

Pallapay stands as your reliable partner in this transition. Our ecosystem is built on institutional financial reliability, featuring MSB registrations in the US and Canada alongside global OTC desks for high-volume liquidation. We provide the definitive bridge between your physical assets and the transformative potential of active trading. It’s time to move beyond the limitations of archaic systems and embrace a streamlined, professional approach to asset settlement.

Your journey toward a more agile financial life begins with the right infrastructure. Unlock Real Estate Liquidity with Pallapay Gateway and start your transition into the world’s most dynamic trading markets today.

Frequently Asked Questions

Can a real estate crypto payment gateway handle multi-million dollar transactions?

Yes, a specialized real estate crypto payment gateway is specifically designed to process high-volume transactions without causing market slippage. These platforms utilize dedicated OTC desks to liquidate large sums at locked prices; this ensures that multi-million dollar property sales remain stable. This infrastructure provides the deep liquidity required for institutional-grade transfers that traditional retail exchanges simply cannot support in a professional environment.

How long does it take for crypto to be settled into my bank account after a property sale?

Instant fiat settlement is the standard for professional gateways in 2026. Once the blockchain transaction is confirmed, the system initiates a direct transfer to your corporate bank account. While traditional bank wires can take several business days to clear, digital gateways often complete the entire cycle within twenty-four hours. This speed allows you to redeploy capital into liquid trading environments almost immediately after closing a sale.

Is it legal to accept cryptocurrency for real estate transactions in 2026?

Accepting cryptocurrency for property is legal and increasingly regulated across major global jurisdictions. In 2026, frameworks like the EU’s MiCA regulation and MSB registrations in North America provide the necessary legal clarity for these transactions. Using a regulated provider ensures that your sale complies with all anti-money laundering and know-your-customer requirements, providing a secure audit trail for tax and legal reporting purposes.

What are the fees associated with using a crypto gateway for property?

Fees generally consist of a small percentage of the total transaction volume and any applicable conversion rates for fiat settlement. These costs are often lower than the cumulative intermediary fees charged by traditional banks for international high-value transfers. You should review the specific fee structure of your chosen provider to ensure it aligns with your capital efficiency goals for large-scale property liquidation and reinvestment.

How can I reinvest my real estate proceeds into Gold and Forex CFDs?

You can reinvest proceeds by utilizing an integrated off-ramp service that moves liquidated fiat directly into a brokerage account. This transition allows you to pivot from stagnant property assets into high-velocity Gold and USD CFD trading. Engaging in these markets offers the potential to change your financial life by providing daily liquidity and the ability to capitalize on global currency movements through a professional trading platform.

Does using a crypto gateway protect me from the volatility of Bitcoin or Ethereum?

Yes, a real estate crypto payment gateway protects you from volatility by locking the exchange rate at the moment of the transaction. This instant conversion feature ensures that the seller receives the exact fiat amount agreed upon, regardless of Bitcoin or Ethereum price swings. Alternatively, using stablecoins like USDT during negotiations provides a fixed value that mirrors the US dollar, eliminating price uncertainty during the escrow period.

What is the benefit of using a regulated MSB for real estate settlement?

A regulated Money Services Business provides the institutional trust necessary for high-stakes real estate deals. MSB status in the US and Canada signifies that the provider adheres to strict federal oversight and financial reporting standards. This regulatory layer ensures that your capital is handled with the highest level of security; it reduces the risk of frozen funds or compliance failures during the settlement process.

Can I use a crypto gateway for both residential and commercial real estate?

Digital gateways are versatile tools that support both residential and commercial real estate transactions. Whether you’re settling a single-family home sale or a multi-unit commercial development, the underlying technology remains the same. The primary requirement is a provider capable of handling the specific volume and compliance needs of your project, ensuring a professional experience for both buyers and developers across all property sectors.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.