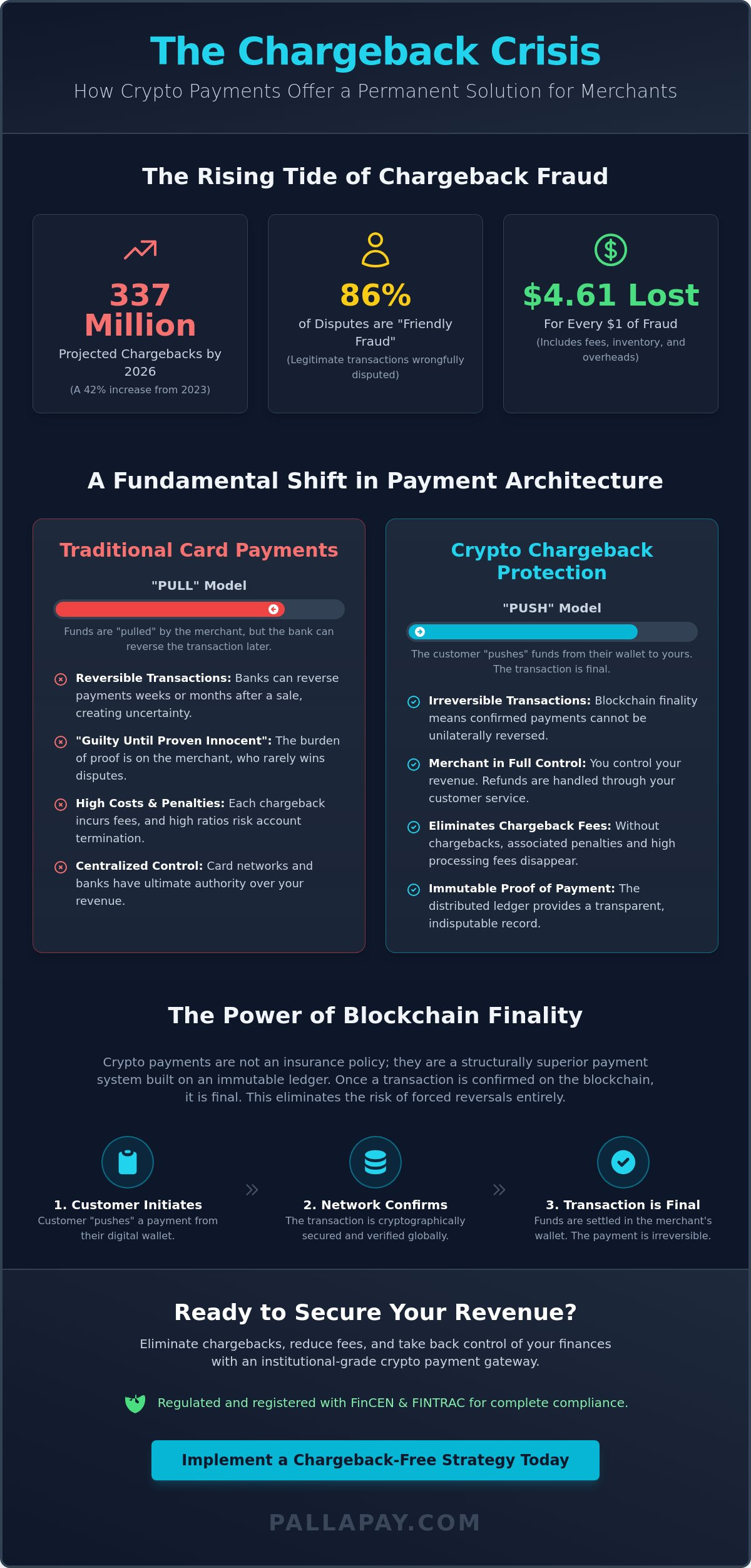

By the end of 2026, global chargeback transactions are projected to reach 337 million, with “friendly fraud” accounting for a staggering 86% of these disputes. If you’ve ever felt the sting of the “guilty until proven innocent” stance taken by major card networks, you aren’t alone. Most merchants now lose an average of $4.61 for every single dollar of fraud. This creates a massive drain on global revenue that traditional insurance simply cannot fix. It’s a frustrating reality where legitimate sales are often reversed without your consent.

This guide demonstrates how crypto chargeback protection for merchants shifts the paradigm from expensive insurance to a secure, irreversible payment architecture. You’ll discover how a professional crypto gateway eliminates the possibility of forced reversals while maintaining institutional-grade stability for your business operations. We will explore the mechanics of blockchain finality, the role of stablecoins in securing your cash flow, and how to integrate a seamless API that protects your bottom line from the rising tide of payment fraud.

Key Takeaways

- Understand why traditional chargeback insurance often fails to protect margins and how a structural shift in payment processing provides a permanent solution.

- Learn the technical mechanics of blockchain finality and how the “push” payment model prevents customers from unilaterally reversing confirmed transactions.

- Discover the significant cost advantages of adopting crypto chargeback protection for merchants to replace high-fee traditional card networks.

- Identify the necessary steps to integrate a professional crypto POS machine or API into your current checkout flow for secure global revenue.

- Explore how partnering with a regulated gateway registered with FinCEN and FINTRAC ensures institutional-grade security and cross-border compliance.

The Rising Cost of Chargeback Fraud for Merchants in 2026

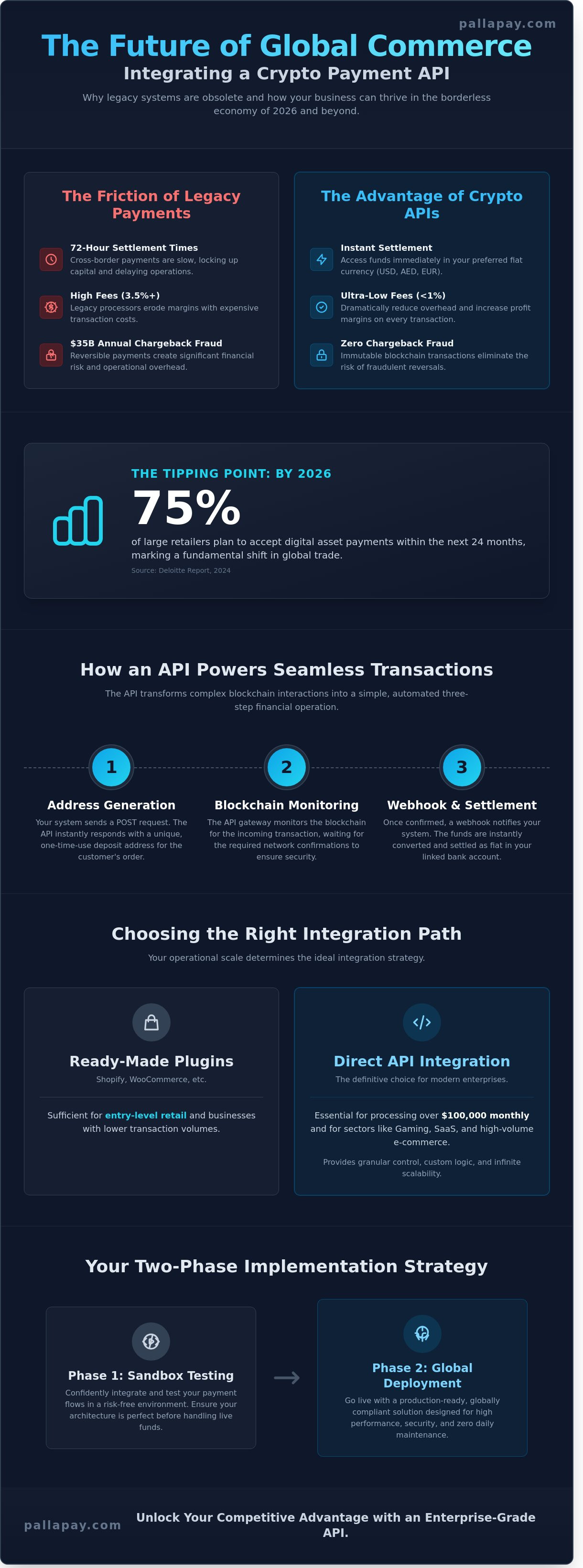

In 2026, the global retail sector faces a critical threshold as chargeback volume reaches a projected 337 million transactions. This figure represents a 42% increase from 2023 levels, signaling a systemic vulnerability in traditional payment networks. For many operators, particularly those in ecommerce, the financial impact is severe. Merchants are currently losing an average of $4.61 for every dollar of fraud encountered. This isn’t just a loss of revenue; it’s a direct erosion of profit margins through lost inventory, wasted shipping overheads, and escalating processor penalties. Traditional chargeback insurance has become a reactive and expensive band-aid that fails to address the root cause of the problem.

The Mechanics of the Traditional Dispute System

The traditional chargeback mechanism relies on a “pull” payment model where banks can reverse a transaction weeks after the sale is finalized. This system inherently favors the consumer, placing a heavy burden of proof on the merchant. Even with detailed documentation, merchants rarely win these disputes because card networks prioritize user trust over business security. High chargeback ratios don’t just result in immediate fees; they threaten the longevity of your merchant account. When a business exceeds certain thresholds, processors often impose higher transaction fees or mandate restrictive cash reserves, further stifling growth and liquidity.

Why 2026 Requires a New Merchant Protection Standard

As we move through 2026, consumer fraud tactics have become significantly more sophisticated. The rise of “friendly fraud,” which accounts for up to 86% of all disputes, often involves customers using AI-generated documentation to validate illegitimate claims. Traditional tools like 3D Secure provide a layer of friction, yet they fail to stop post-transaction reversals. Businesses can no longer rely on systems that treat fraud as an inevitable tax on operations. True crypto chargeback protection for merchants offers a shift from risk mitigation to total risk elimination. By adopting a payment architecture based on blockchain finality, you ensure that once a transaction is confirmed, the revenue remains under your control. This technological answer solves the operational need for absolute payment certainty in an increasingly volatile global market.

Mastercard projects that U.S. merchants alone will lose $15 billion to chargeback fraud this year. This staggering loss highlights the inadequacy of current card-based systems. Transitioning to a secure gateway allows your business to bypass the “guilty until proven innocent” stance of major card networks. It’s time to replace outdated insurance policies with a payment model that provides the ultimate protection for your global revenue.

How Crypto Chargeback Protection Works: The Power of Irreversibility

At its core, crypto chargeback protection for merchants is not a service or an insurance policy; it’s a fundamental property of blockchain technology. In traditional finance, payments operate on a “pull” model. When a customer swipes a card, the merchant’s processor requests funds from the issuing bank. This authorization remains conditional, allowing the bank to unilaterally reverse the transaction weeks or even months later. Cryptocurrency flips this logic by using a “push” model. The customer must actively initiate the transfer of assets from their wallet to yours. Once the network confirms the transaction, the funds are moved permanently. There’s no central issuing bank with the authority to “pull” those funds back into the customer’s account.

Distributed ledger technology (DLT) provides a transparent, immutable proof of payment that serves as the ultimate record for your accounting. Because every transaction is cryptographically secured and broadcast across a global network, the evidence of the transfer is indisputable. This eliminates the middleman typically responsible for initiating disputes. Without a centralized authority to mediate or reverse transactions, the merchant retains full control over their revenue. This structural shift moves the responsibility of refunds back to your own customer service department, ensuring that you only return funds when a claim is legitimate and verified by your team.

The Blockchain as a Final Settlement Layer

Understanding transaction finality is essential for managing institutional-grade financial flows. Transaction finality is the definitive state where a payment is permanently recorded on the blockchain and cannot be altered or reversed by any party. This protocol-level security ensures that once a digital asset reaches your wallet, it’s yours. Smart contracts can further refine this process by automating escrow or multi-signature approvals, providing a secure bridge between payment and delivery without the risk of traditional reversals. For businesses handling complex cross-border transactions, this creates a level of certainty that legacy banking systems simply can’t match.

Comparing Traditional vs. Crypto Protection Frameworks

The traditional dispute framework is inherently merchant-liable and characterized by slow, expensive resolution processes. Research from The Payments Association highlights that rising fraud levels are putting nearly half of certain retail sectors at risk of scaling back in 2026. This vulnerability stems from a system designed to protect the consumer at the merchant’s expense. In contrast, crypto offers a zero-dispute architecture where payments are final at the point of sale. Merchants in high-ticket industries like hotels and luxury e-commerce are increasingly prioritizing these payments to secure revenue on items with high shipping costs or non-refundable bookings. Integrating a professional payment API allows you to adopt this fraud-free model while maintaining the speed and efficiency your customers expect.

Traditional Gateways vs. Crypto Chargeback Protection

Traditional payment providers often market “chargeback protection” as a comprehensive shield, yet it’s essentially a reactive insurance policy laden with exclusions. These services typically require merchants to pay a premium on every transaction, often pushing processing fees well above 3%. In contrast, crypto chargeback protection for merchants is a structural feature of the payment architecture itself. By removing the ability for a central authority to reverse funds, the need for expensive insurance disappears. This allows for a leaner operational model where processing costs are significantly reduced compared to legacy card networks.

Global reach and liquidity speed also define the divide between these two systems. Traditional card networks frequently flag cross-border sales as high-risk, leading to higher decline rates or extended hold periods that can last up to 14 days. These delays are designed to buffer the bank against potential disputes. Cryptocurrency transactions operate independently of these geographic restrictions and banking “cooling-off” periods. Settlements occur with near-instant speed, allowing businesses to maintain a healthier cash flow and re-invest capital into growth rather than waiting for funds to clear a processor’s risk department.

The Hidden Limitations of Card Protection Services

The “fine print” of traditional unauthorized transaction coverage often reveals a complex web of requirements. Merchants must frequently provide perfect evidence within strict timeframes to even qualify for protection. This creates an administrative nightmare that drains resources and rarely guarantees a win. Even if a merchant is “protected,” high chargeback ratios can still damage their reputation with acquiring banks. This can lead to increased scrutiny, higher reserve requirements, or the sudden termination of the merchant account. Relying on card-based protection means managing a symptom rather than curing the underlying vulnerability of the “pull” payment model.

The Crypto Advantage: Proactive Security

A secure crypto payment gateway provides proactive security by ensuring that every transaction is final at the point of confirmation. This structural irreversibility eliminates the “fraud tax” that many businesses have come to accept as a cost of doing business. As detailed in the report How Crypto Shields Merchants Against Chargeback Fraud, the shift to blockchain finality removes the mechanism that makes friendly fraud possible. By adopting this technology, businesses move away from the “guilty until proven innocent” stance of traditional finance. This shift toward crypto chargeback protection for merchants represents a move from passive risk management to active revenue security, allowing you to focus on global expansion without the fear of arbitrary fund reversals.

Implementing a Chargeback-Free Strategy for Your Business

Transitioning to a fraud-free environment requires a deliberate shift in your payment architecture. To begin, select a regulated gateway that aligns with institutional standards. This ensures your revenue is handled by an entity registered with authorities like FinCEN in the USA or FINTRAC in Canada. Establishing this foundation is the first step in securing crypto chargeback protection for merchants. Once the partnership is formed, you can move toward technical integration. This process transforms your payment flow from a conditional authorization model to a definitive settlement model.

Communicating the benefits of these payments to your customers is equally vital. Transparency regarding the irreversibility of blockchain transactions helps set expectations and reduces the likelihood of confusion. You can manage these digital assets through a secure merchant dashboard, which provides real-time visibility into your global revenue. Finally, utilize professional off-ramps to convert your protected revenue into local currency, ensuring your cash flow remains liquid and usable for daily operations.

Integrating Crypto Payments Without Technical Friction

Modern businesses require solutions that integrate into existing workflows without disrupting the user experience. Using a payment API allows you to automate secure checkouts, providing a seamless transition for online customers. For physical retail locations, setting up Crypto POS machines offers a familiar interface for both staff and shoppers. These tools ensure the checkout mirrors traditional card flows while providing the underlying security of the blockchain. This balance of familiarity and innovation is essential for maintaining high conversion rates while eliminating dispute risk.

Managing Volatility and Liquidity

A common concern for businesses is the price movement of digital assets. Professional fiat settlement removes this risk by instantly converting incoming crypto payments into stable currencies. This feature ensures that the value you see at the point of sale is the exact value you receive in your account. By setting up automated off-ramps to your corporate bank account, you can maintain a steady stream of liquidity. For instance, direct settlement in AED can save merchants approximately 2% to 3% on currency conversion costs compared to traditional methods. Maintaining a secure digital wallet for operational liquidity further empowers your business to move capital across borders with unmatched efficiency. To begin securing your global revenue, integrate a secure crypto gateway today.

Secure Your Global Revenue with Pallapay’s Ecosystem

Pallapay serves as the definitive destination for businesses seeking institutional financial reliability alongside disruptive innovation. In 2026, securing your global revenue requires a partner that understands both the technical finality of the blockchain and the practicalities of modern commerce. By providing crypto chargeback protection for merchants across more than 180 countries, we offer a level of stability that traditional networks cannot match. Our ecosystem is built on the confidence of a global industry leader, ensuring that your transition to digital asset payments is both secure and effortless. This global reach is supported by local expertise, ensuring that regardless of where your customers are located, your revenue remains protected from the risks of “friendly fraud” disputes.

Institutional-Grade Compliance and Security

Trust is the backbone of any financial operation. Pallapay maintains active MSB registration with FinCEN in the United States and FINTRAC in Canada, providing a professional bridge to established regulatory standards. We handle the complex background processes of Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols so your team doesn’t have to manage these technical burdens. For high-volume settlements, our OTC crypto exchange offers a secure environment that prioritizes speed and safety. Additionally, our presence in major global hubs reinforces merchant trust through physical accessibility and dedicated support. This institutional grounding ensures that your business operates within a framework of absolute security and regulatory harmony.

The Pallapay Merchant Advantage

Adopting our technology means gaining access to a comprehensive suite of tools designed for rapid growth. The Pallapay merchant dashboard provides advanced statistics and cost-tracking, allowing you to monitor your global revenue with absolute clarity and real-time precision. We offer customizable solutions for retail stores and online platforms, ensuring that your specific operational needs are met with precision. This tailored approach allows you to scale your payment infrastructure at your own pace.

Beyond basic processing, our ecosystem includes the Pallapay Mastercard and diverse gift card products, which add immediate utility to your digital holdings. These tools allow you to convert protected revenue into spending power instantly, bypassing the friction of traditional banking delays. By integrating these services, you create an efficient cycle of liquidity that supports your business’s momentum. Pallapay serves as the professional bridge that connects established practices with modern advancements, ensuring your business is ready for the inevitable global evolution of payments.

Securing the Future of Global Merchant Revenue

The evolution of digital commerce in 2026 demands a move away from the restrictive “guilty until proven innocent” mindset of traditional card networks. By adopting a system built on blockchain finality, you eliminate the mechanism that makes friendly fraud possible. This structural shift ensures that confirmed revenue stays in your control, providing the most reliable form of crypto chargeback protection for merchants available today. You’re no longer just managing risk; you’re removing it from your balance sheet entirely.

Professional growth requires a partner that combines disruptive technology with institutional stability. Pallapay provides this through our status as an MSB registered entity in the USA and Canada, backed by a global OTC presence and near-instant fiat settlement capabilities. This ensures that your liquidity remains high while your operational friction stays low. It’s time to transition from outdated dispute systems to a future of absolute payment certainty. Secure your business against chargebacks with Pallapay’s global payment gateway. We look forward to helping you scale your international operations with total confidence.

Frequently Asked Questions

Is there any way for a customer to get a refund on a crypto payment?

Yes, but the refund must be initiated by the merchant rather than the customer’s bank. Because blockchain transactions are irreversible by the sender, you retain full authority over your return policy. This structural shift is the core of crypto chargeback protection for merchants, ensuring that funds are only returned if you verify the claim is legitimate. It places the merchant back in control of the customer service and dispute resolution process.

Do I need to understand blockchain technology to use crypto chargeback protection?

No, you don’t need deep technical knowledge to implement these security features. Modern payment gateways handle the underlying cryptographic processes and network confirmations in the background. You interact with a professional merchant dashboard that feels identical to traditional financial tools. This allows you to focus on scaling your business while the technology provides a secure, fraud-free environment for every transaction you process.

How do crypto gateway fees compare to traditional chargeback insurance?

Crypto gateway fees are significantly more cost-effective, typically ranging from 0% to 1%. Traditional card networks often charge between 2.1% and 3.5%, and that doesn’t include the added premiums for separate chargeback insurance or the high costs of dispute penalties. By adopting a system with inherent protection, you eliminate the need for expensive “band-aid” insurance policies and reduce your overall operational overhead immediately.

Can crypto payments be used for high-ticket items in industries like luxury travel?

Yes, cryptocurrency is exceptionally well-suited for high-value transactions where the risk of “friendly fraud” is greatest. When selling luxury goods or travel packages, a single forced reversal can devastate your monthly margins. Using a secure gateway ensures that large payments are final at the point of confirmation. This provides institutional-grade certainty for high-ticket sectors, allowing you to ship goods or confirm bookings without the fear of post-sale fund withdrawals.

What happens if a customer claims they didn’t receive the item after paying in crypto?

The merchant manages the dispute internally based on their established terms and conditions. Unlike card networks that often side with the consumer by default, crypto payments don’t have a third-party “issuing bank” that can freeze your funds. You can review the customer’s claim and shipping evidence fairly. If a mistake occurred, you can issue a voluntary refund; if the claim is fraudulent, your revenue remains safely in your account.

Is crypto chargeback protection legal and compliant for US-based merchants?

Yes, accepting cryptocurrency is fully legal and compliant for merchants in the United States and other global regions. To ensure institutional trust, it’s essential to partner with a gateway that is MSB registered. Pallapay is registered with FinCEN in the USA and FINTRAC in Canada, ensuring that your crypto chargeback protection for merchants is backed by a framework of global regulatory compliance and institutional financial reliability.

How quickly can I convert my crypto payments into fiat currency like USD or EUR?

Conversions can happen near-instantly through professional fiat settlement services. You don’t have to wait for the traditional 7 to 14 day hold periods required by many credit card processors. Most gateways allow you to lock in the exchange rate at the moment of the transaction, protecting you from price volatility. This ensures that your revenue is available for bank transfer or operational use in your local currency with minimal delay.

Can I accept multiple cryptocurrencies like Bitcoin, Ethereum, and USDT simultaneously?

Yes, a comprehensive payment gateway allows you to accept a diverse range of digital assets through a single API or POS integration. This flexibility caters to a global audience while consolidating all incoming payments into a unified merchant dashboard. Whether a customer pays in Bitcoin or a stablecoin like USDT, the transaction remains irreversible. This ensures your business captures every sales opportunity without exposing itself to the risks of traditional payment disputes.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.