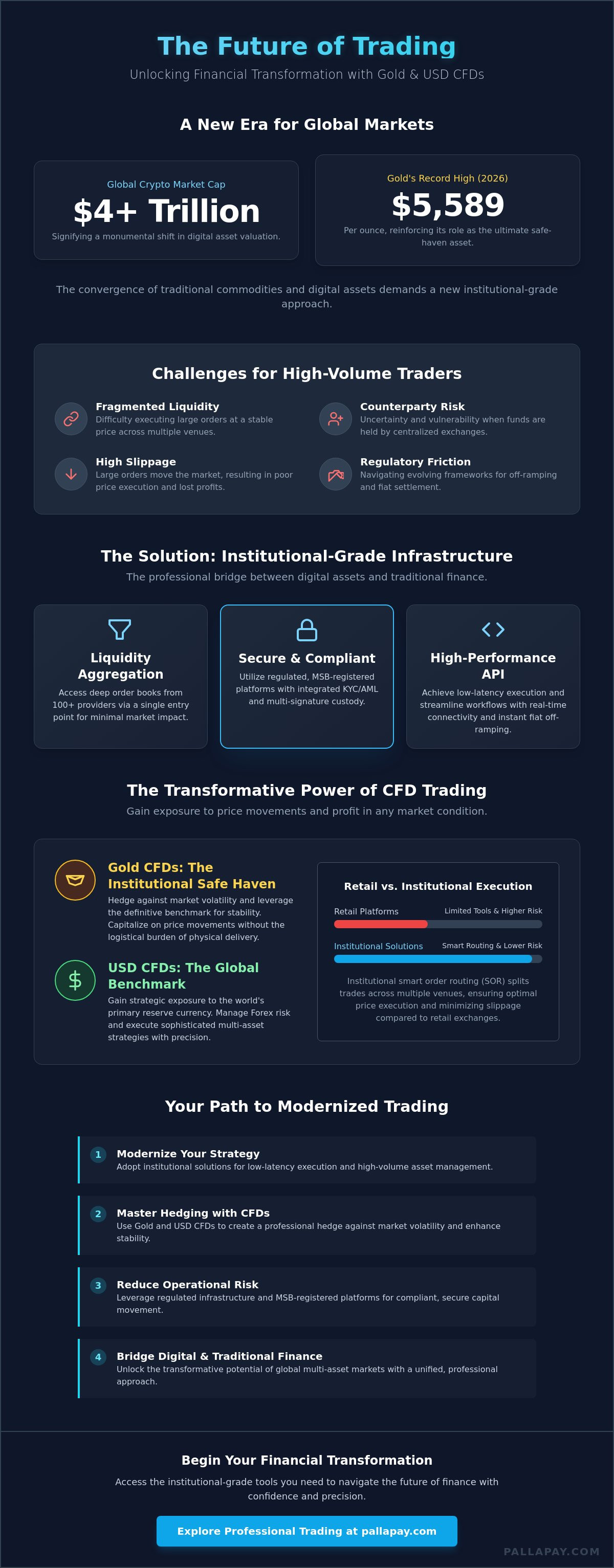

In 2025, the total on-chain transaction volume for stablecoins surpassed $27 trillion, signaling a permanent shift in how modern enterprises manage liquidity. Most executives agree that traditional banking often feels like a relic, especially when high fees on international transfers and slow settlement cycles keep capital locked in inefficient systems. You shouldn’t have to watch inflation erode your idle corporate cash while waiting for outdated rails to clear. Understanding the strategic benefits of accepting usdt for business is no longer optional; it’s a fundamental requirement for any firm looking to maintain a competitive edge in the 2026 financial landscape.

We’ll show you how integrating USDT payments streamlines your global operations and unlocks high-yield opportunities in Forex and Gold CFD trading. This guide details the mechanics of instant settlements and explains how to pivot from passive payment collection to active wealth generation. You’ll discover how the transformative potential of XAU/USD markets can change your organization’s financial trajectory by turning every transaction into a strategic growth asset. This isn’t just about a new way to get paid; it’s about building a professional bridge to the future of institutional finance.

Key Takeaways

- Accelerate your settlement cycles with 24/7/365 availability, ensuring that corporate capital is never locked behind traditional banking hours.

- Minimize operational friction by reducing cross-border transaction costs from standard high-percentage fees to efficient, fractional network expenses.

- Maximize the benefits of accepting usdt for business by utilizing real-time liquidity as instant margin for high-stakes Forex and Gold CFD trading.

- Transform stagnant revenue into a strategic growth engine by leveraging XAU/USD markets to hedge against inflation and capture institutional-grade returns.

- Deploy sophisticated payment infrastructure through seamless API and POS integrations that unify global commerce with modern treasury management.

Why USDT is the Global Standard for Business Settlements in 2026

The digital landscape has matured, and by July 2026, the distinction between traditional treasury and digital asset management has effectively vanished. For any enterprise operating on a global scale, the benefits of accepting usdt for business center on one primary factor: predictability. Unlike speculative assets, Tether (USDT) functions as a digital mirror of the US Dollar, providing a stable unit of account that fits seamlessly into existing corporate balance sheets. This stability eliminates the “crypto-anxiety” that previously deterred institutional involvement. It allows firms to enjoy the speed of blockchain without the price swings of Bitcoin. Businesses don’t want to risk their payroll or vendor payments on an asset that could drop 10% overnight; they want the reliability of the dollar with the efficiency of the cloud.

With a market capitalization exceeding $186 billion as of early July 2026, USDT commands nearly 60% of the stablecoin market. This unmatched liquidity ensures that even the largest corporate settlements can be executed instantly without slippage. While Bitcoin remains a store of value for many, businesses prefer USDT for day-to-day operations because its value doesn’t shift during the hours between an invoice being issued and the payment being settled. It’s a utility-focused tool designed for commerce. By choosing a stable medium, companies can forecast their cash flow with precision while still accessing the global, borderless nature of digital finance.

The Institutional Shift Toward Stablecoin Treasury

The implementation of the EU’s MiCA framework and the US GENIUS Act has transformed how corporations view digital assets. What began as a trial phase for tech-forward companies has become a standard operational procedure for global competitors. Firms now hold USDT as a core treasury asset to facilitate immediate vendor payments and maintain liquid reserves. This shift is driven by the need for speed; waiting for a bank to open on Monday is a liability in a 24/7 global market. USDT serves as the professional bridge between legacy banking and decentralized finance.

Compliance and Security: The Non-Negotiables

Accepting digital payments requires more than just a digital wallet. It demands a partnership with a regulated Money Services Business (MSB) that can provide direct fiat settlement. Professional firms prioritize providers that offer institutional-grade security protocols to protect their bottom line. Multi-signature wallets have become the corporate standard, requiring multiple authorized approvals before any capital moves. This layer of governance ensures that one of the core benefits of accepting usdt for business, security, is never compromised by human error or external threats. When your capital is protected by hardware-level encryption and strict regulatory oversight, the transition to digital settlements becomes an effortless strategic upgrade.

Operational Efficiency: Eliminating Cross-Border Friction

The traditional financial system relies on a complex web of correspondent banks, each adding a layer of delay and a slice of the transaction fee. By the time a cross-border payment reaches its destination, the sender has often lost 3% to 5% of the total value to various intermediaries. One of the core benefits of accepting usdt for business is the immediate removal of these 20th-century bottlenecks. Instead of waiting for bank opening hours or navigating public holidays in different time zones, you operate on a 24/7/365 settlement cycle. This transition moves your status from “payment pending” to “capital available” in seconds, providing the agility required to thrive in modern commerce.

Operating globally usually requires maintaining dozens of local bank accounts to manage different currencies, which creates an administrative burden that drains human resources. USDT simplifies this by acting as a universal digital dollar. It allows you to consolidate global revenue into a single, highly liquid stream without the need for complex banking structures. This consolidation reduces operational overhead and provides a clearer view of your real-time financial position. You don’t just save money on fees; you reclaim the time your accounting team used to spend reconciling disparate accounts. Efficiency becomes your primary competitive advantage.

To complement these financial efficiencies, forward-thinking enterprises often explore Offshore Staffing with Ubuntu BPO to optimize their broader administrative functions and support teams globally.

Revolutionizing International Supply Chains

Supply chain efficiency depends entirely on the speed of capital movement. Many ecommerce businesses have pivoted to USDT to settle with international vendors instantly. By avoiding predatory FX spreads and the hidden fees of intermediary banks, these firms can secure better terms and faster shipping times. This rapid turnover of capital directly translates into higher inventory velocity and improved profit margins. When a payment is sent via blockchain, the vendor receives it almost immediately, allowing them to release goods without the usual three-day wait for wire confirmation.

The End of Chargeback Fraud

Traditional credit card payments are inherently vulnerable to malicious reversals and “friendly fraud,” which can disrupt cash flow and lead to significant losses. Blockchain transactions are defined by their finality. Once a USDT payment is confirmed on the network, it’s irreversible. This protective layer ensures that merchants aren’t subject to the whims of card issuers or fraudulent claims. Your revenue remains secure, allowing for more accurate cash flow predictability and long-term financial planning. It’s a fundamental shift in the power dynamic of digital commerce. If you’re ready to modernize your checkout, integrating a payment API can secure these operational advantages today.

Strategic Capital Growth: Leveraging USDT for Forex and Gold CFD Trading

Accepting digital payments is often viewed as a defensive move to reduce fees, but the true benefits of accepting usdt for business emerge when you pivot from a merchant mindset to a strategic investor mindset. Instead of letting revenue sit idle in a low-interest bank account where inflation might erode its value, USDT provides a high-velocity liquidity advantage. Because USDT operates on blockchain rails, it can be deployed as instant margin for high-stakes trading environments. This means your daily sales don’t just sit on a balance sheet; they become the active engine for your corporate treasury, allowing for immediate participation in global markets.

Professional traders increasingly favor USDT as their primary base currency for its stability and ease of transfer between global exchanges. When your business accepts USDT, you’re already holding the preferred medium for professional Forex and commodity markets. This eliminates the need for expensive fiat-to-crypto conversions or the typical two-day settlement delay associated with traditional brokerage funding. You’re moving from a state of passive holding to active capital deployment with zero friction. It’s a fundamental shift that positions your business as a sophisticated participant in the digital economy.

XAU/USD: Hedging Business Capital with Gold CFDs

Gold has always been the ultimate hedge against fiat instability, but physical storage is a logistical nightmare for most businesses. Gold CFD trading allows you to profit from XAU/USD price movements without the overhead of physical security, insurance, or transport, whereas established entities like Dover Jewelry and Pawn Exchange continue to serve those who prioritize the tangible security of physical assets. By using your USDT liquidity, you can enter the gold market during periods of currency volatility to protect your purchasing power with institutional precision. This strategic move can fundamentally change an individual’s financial life by turning standard business risk into a diversified portfolio of commodity exposure.

Forex Trading: Mastering Currency Fluctuations

The global Forex market offers a transformative potential for accelerating corporate growth through leveraged trading. By maintaining a USDT-denominated Forex account, you can capitalize on USD strength while avoiding the delays and predatory spreads of traditional wire transfers. CFD trading empowers businesses to generate returns from both rising and falling market trends through speculative positions that don’t require ownership of the underlying currency pair. This flexibility ensures that your capital remains productive regardless of broader economic shifts. Mastering these markets allows a business to offset operational costs through savvy market participation.

Implementing a USDT Framework: POS and API Integration

Transitioning from traditional payment processing to a digital asset framework requires a structured approach that prioritizes security and operational continuity. The benefits of accepting usdt for business are only fully realized when the technology integrates silently into your existing stack without disrupting the customer journey. By July 2026, technical barriers have largely vanished, replaced by standardized protocols that allow for rapid deployment across global markets. Successful implementation follows a logical progression that connects your storefront directly to your corporate treasury with minimal friction.

- Step 1: Select a payment gateway that offers direct fiat settlement to ensure your accounting remains compliant with local regulations while avoiding unnecessary market exposure.

- Step 2: Integrate a robust payment API into your existing e-commerce checkout to automate the collection and reconciliation process in real-time.

- Step 3: Deploy physical POS terminals at brick-and-mortar locations to provide a unified, professional payment experience for in-person clients.

- Step 4: Conduct comprehensive staff training on digital asset handling, focusing on wallet security and verifying transaction confirmations to prevent operational errors.

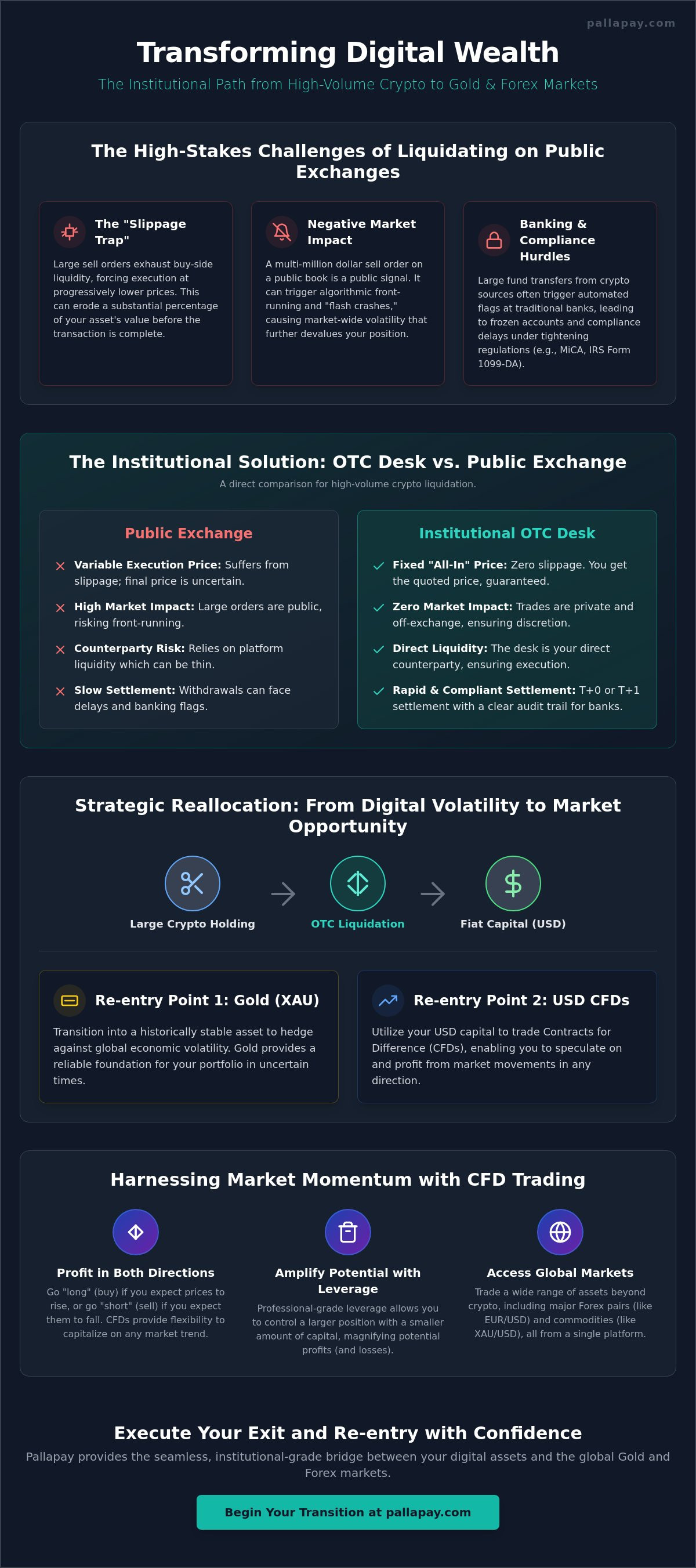

- Step 5: Establish a connection with a dedicated OTC desk for high-volume liquidations, ensuring you can move large blocks of capital without impacting market prices.

Omnichannel Acceptance: From Web to Storefront

The modern consumer expects a consistent experience across all platforms. For retail stores, this means accepting USDT as easily as a standard credit card. In the 2026 payment landscape, QR codes and NFC technology have become the primary drivers of this efficiency. A customer simply scans a code at the register, and the transaction is settled on the blockchain in seconds. This omnichannel approach ensures you never miss a sale while providing a tech-forward image that resonates with professional digital asset holders. It’s about providing a frictionless bridge between digital wealth and physical commerce.

Automating the Flow: From USDT to Bank Transfer

Efficiency is driven by automation. By setting up auto-conversion rules, you can mitigate even the smallest stablecoin fluctuations and ensure your revenue is always where it’s needed most. Utilizing sophisticated off-ramp services allows for a seamless connection between your digital revenue and legacy systems like payroll or tax accounting. This creates a closed-loop ecosystem where payments are received, converted, and deployed with zero manual intervention. If you’re ready to modernize your infrastructure, you can integrate our crypto payment gateway to begin your transition today.

The Future of Corporate Finance: Converting Payments into Opportunities

By July 2026, the “wait and see” approach to digital assets has become a distinct competitive disadvantage. Companies that hesitated to adopt digital settlements now find themselves excluded from high-velocity supply chains and sophisticated trading circles. The benefits of accepting usdt for business extend far beyond simple transaction processing; they represent the complete convergence of payments, trading, and treasury management into a single, high-performance ecosystem. This integration allows a business to capture revenue and immediately pivot into XAU/USD markets or Forex positions, maximizing the utility of every dollar earned. Waiting is no longer a conservative strategy; it’s a loss of momentum.

The long-term vision for corporate finance is one that is borderless, instant, and inherently high-growth. In this new landscape, the traditional silos between “getting paid” and “investing” have collapsed. Every incoming payment is a liquidity event that can be used to hedge against inflation or capture market volatility in real-time. This level of financial agility was once reserved for elite hedge funds, yet the 2026 digital framework makes it accessible to any enterprise with the right infrastructure. Efficiency is the new standard, and those who master these tools will define the next decade of commerce.

The Pallapay Advantage: Beyond the Gateway

Pallapay facilitates the professional bridge between crypto innovation and institutional reliability. By maintaining official MSB registrations in the United States and Canada, we provide the regulatory certainty required for modern corporate governance. Our ecosystem is a comprehensive destination for all technical needs, offering access to high-volume OTC desks, robust POS hardware, and seamless card issuance. Leveraging the Pallapay Mastercard allows you to spend USDT profits in the real world, providing a direct link between your digital treasury and physical operational requirements. We handle the complex background processes so you can focus on strategic expansion.

Next Steps for Your Business

The path to financial transformation begins with a single integration. You can initiate your first USDT transaction today and begin consulting with experts to tailor a CFD trading strategy that aligns with your specific corporate treasury goals. Whether you’re looking to hedge against fiat instability through Gold CFDs or capitalize on currency movements in the Forex market, our tools provide the necessary leverage for accelerated growth. This shift has the power to change an individual’s financial life by providing institutional-grade tools to every business owner. Start your journey toward financial transformation with Pallapay and secure your place in a borderless, instant, and high-growth financial future.

Securing Your Position in the Global Digital Economy

The transition to a digital dollar framework is no longer a speculative choice; it’s a strategic necessity for institutional growth. By integrating these systems, you eliminate the friction of legacy banking and gain immediate access to high-yield markets like XAU/USD and Forex CFDs. The benefits of accepting usdt for business reside in this unique ability to transform stagnant revenue into a high-velocity growth engine. You’re not just adopting a new payment method; you’re building a professional bridge to a borderless financial future where capital is never idle.

Success in this landscape requires a partner that combines disruptive innovation with institutional reliability. Pallapay provides a comprehensive POS and API infrastructure to support your expansion across 180+ countries. As an official MSB registered in the USA and Canada, we ensure your operations remain secure and compliant at every step. It’s time to move beyond traditional limitations and capture the transformative potential of modern trading. Empower your business with Pallapay’s secure USDT payment solutions and high-volume OTC services. Your evolution into a strategic global entity starts with a single, secure integration.

Frequently Asked Questions

Is accepting USDT legal for my registered business?

Accepting USDT is legal for registered businesses in most global jurisdictions that recognize digital assets as legitimate payment instruments. In 2026, frameworks like the US GENIUS Act and the EU’s MiCA regulation have established clear compliance pathways for corporate entities. You must ensure your business partners with a regulated service provider that adheres to strict Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols to maintain full legal standing.

How do I protect my business from USDT price fluctuations?

Protecting your business from minor stablecoin fluctuations is achieved through automated fiat settlement or immediate conversion rules. While USDT maintains a 1:1 peg with the US Dollar, you can set your payment gateway to instantly convert incoming digital assets into your local currency. This strategy locks in the transaction value at the moment of sale, ensuring your accounting remains precise and your margins are protected from even the smallest market movements.

Can I instantly convert USDT into cash for business expenses?

You can convert USDT into cash instantly by utilizing professional OTC desks or crypto-to-bank transfer services. These platforms allow you to liquidate large volumes of digital assets and move the resulting fiat directly into your corporate bank account. This ensures that your revenue is always available for immediate business expenses such as payroll, vendor payments, or inventory acquisition without the delays typical of traditional financial intermediaries.

What are the tax implications of holding USDT on a corporate balance sheet?

Holding USDT on a corporate balance sheet typically requires reporting the asset at its fair market value in your functional currency. Most tax authorities treat stablecoins as digital property or foreign currency equivalents, meaning you must track the cost basis and any realized gains or losses upon conversion. Because tax laws vary significantly by region in 2026, you should consult with a certified professional to ensure your reporting meets current standards.

How does Gold CFD trading differ from buying physical gold?

Gold CFD trading focuses on price speculation rather than physical ownership, eliminating the need for secure storage, insurance, or transport. Unlike physical gold, which is a passive asset, CFDs allow you to use leverage and profit from both rising and falling price trends. This flexibility makes it a more efficient tool for businesses looking to hedge their capital against inflation or currency volatility without the logistical burden of bullion.

What kind of hardware do I need to accept USDT in my retail store?

To accept USDT in a physical retail environment, you simply need a dedicated Crypto POS Machine or a tablet equipped with a compatible payment application. These devices generate unique QR codes for each transaction, allowing customers to pay directly from their digital wallets. The hardware integrates seamlessly with your existing network, providing real-time confirmation and a professional checkout experience that mirrors traditional card-based systems.

How fast are USDT transactions compared to traditional wire transfers?

USDT transactions settle in seconds or minutes, representing a massive improvement over the 3-5 business days required for traditional international wire transfers. This rapid settlement cycle is one of the most impactful benefits of accepting usdt for business, as it provides instant access to capital. By removing the “pending” state of traditional banking, your firm can reinvest revenue into growth opportunities like Gold CFDs almost as soon as a sale is completed.

Is a specialized developer needed to integrate a USDT payment API?

A specialized developer is usually not required because modern payment APIs are designed for easy integration with standard e-commerce platforms. Most professional providers offer comprehensive documentation and pre-built plugins that allow your existing IT team to deploy the system quickly. This “plug-and-play” approach ensures that you can begin accepting digital payments with minimal technical overhead, allowing you to focus on your core business operations instead of complex coding.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.