What if your daily retail sales didn’t just sit in a stagnant bank account but served as the immediate fuel for institutional-grade gold and currency markets? You likely feel the sting of traditional processors that take over 3.5% of your revenue and delay settlements for days. Integrating a crypto pos machine for small business in 2026 solves this by providing instant fiat conversion and eliminating the risk of costly chargebacks. With over 45% of global merchants now accepting digital assets, the shift toward blockchain-based payments is no longer a trend; it’s a standard for professional growth.

This guide explains how to select a terminal that transforms your storefront into a gateway for XAU/USD and USD CFD trading. You’ll discover how the GENIUS Act of 2025 has stabilized the market, allowing you to move capital from a customer’s wallet to a forex account with zero friction. We’ll explore the latest hardware options, regulatory requirements like the proposed PARITY Act, and the specific technical flows that turn your overhead into a strategic trading advantage. It’s time to stop paying for outdated infrastructure and start leveraging your revenue for transformative financial impact.

Key Takeaways

- Learn how a crypto pos machine for small business functions as a professional bridge, transitioning your operations from basic payment processing to active capital management.

- Identify essential terminal features like instant QR code generation and multi-currency support that ensure a frictionless checkout experience for your global clientele.

- Discover how to leverage retail revenue for XAU/USD and USD CFD trading, turning standard transactions into strategic assets for long-term financial growth.

- Master the criteria for evaluating providers, focusing on transparent fee models and the necessity of MSB registration to maintain institutional-grade security.

- Explore the advantages of an integrated ecosystem that links your physical point of sale to liquid markets through dedicated crypto cards and OTC services.

The Strategic Evolution: Why Small Businesses Need a Crypto POS Machine

A Point of Sale (POS) was once a static terminal designed for simple commerce, but it’s now evolving into a sophisticated financial bridge. For the modern entrepreneur, a crypto pos machine for small business is a professional gateway into a digital economy where liquidity is immediate and capital is globally mobile. This technology moves beyond the basic act of accepting payments. It allows you to manage liquid capital with the precision of an institutional trader, ensuring your revenue is always working for you.

The transition from legacy systems to blockchain-integrated hardware removes the friction inherent in traditional banking. You’re no longer at the mercy of slow settlement times that hinder reinvestment. Instead, your retail revenue becomes a launchpad for high-impact gold and USD CFD trading. By establishing direct blockchain-to-fiat pipelines, you gain near real-time access to funds. This level of agility is what defines a truly modern enterprise, allowing you to pivot that liquidity into the forex market and capture XAU/USD movements while your competitors are still waiting for their bank to clear yesterday’s transactions.

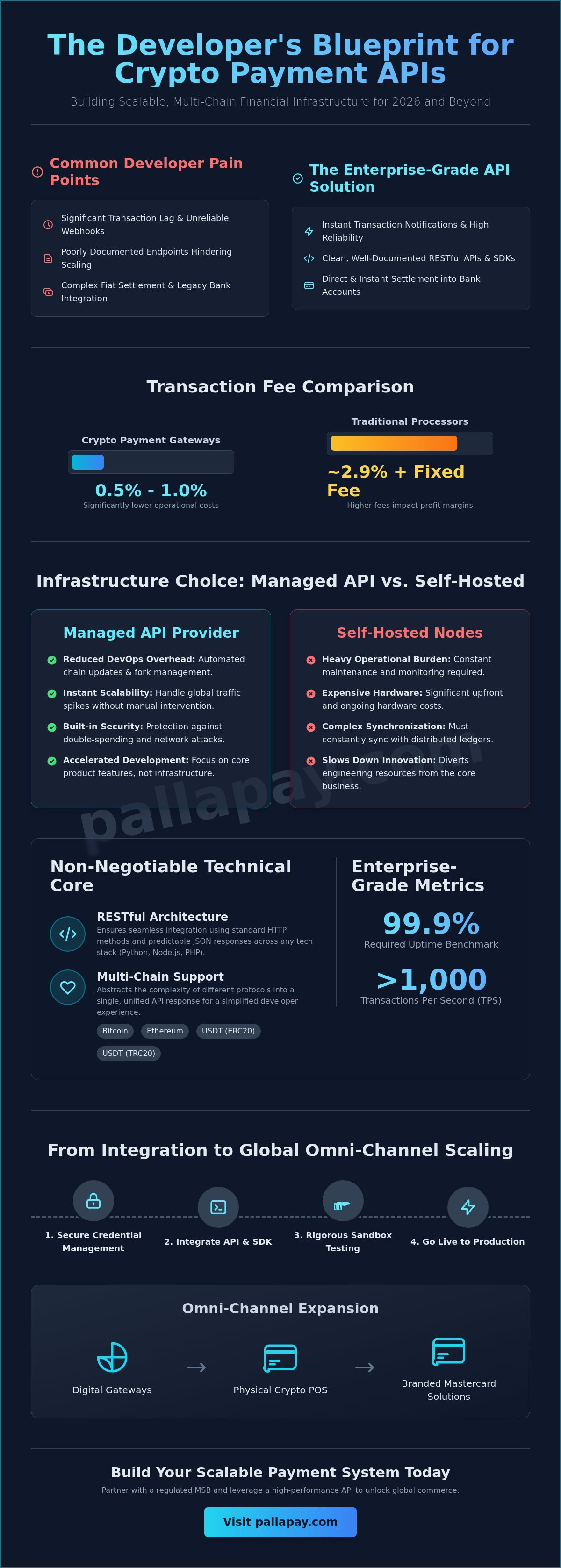

The Death of Traditional Merchant Fees

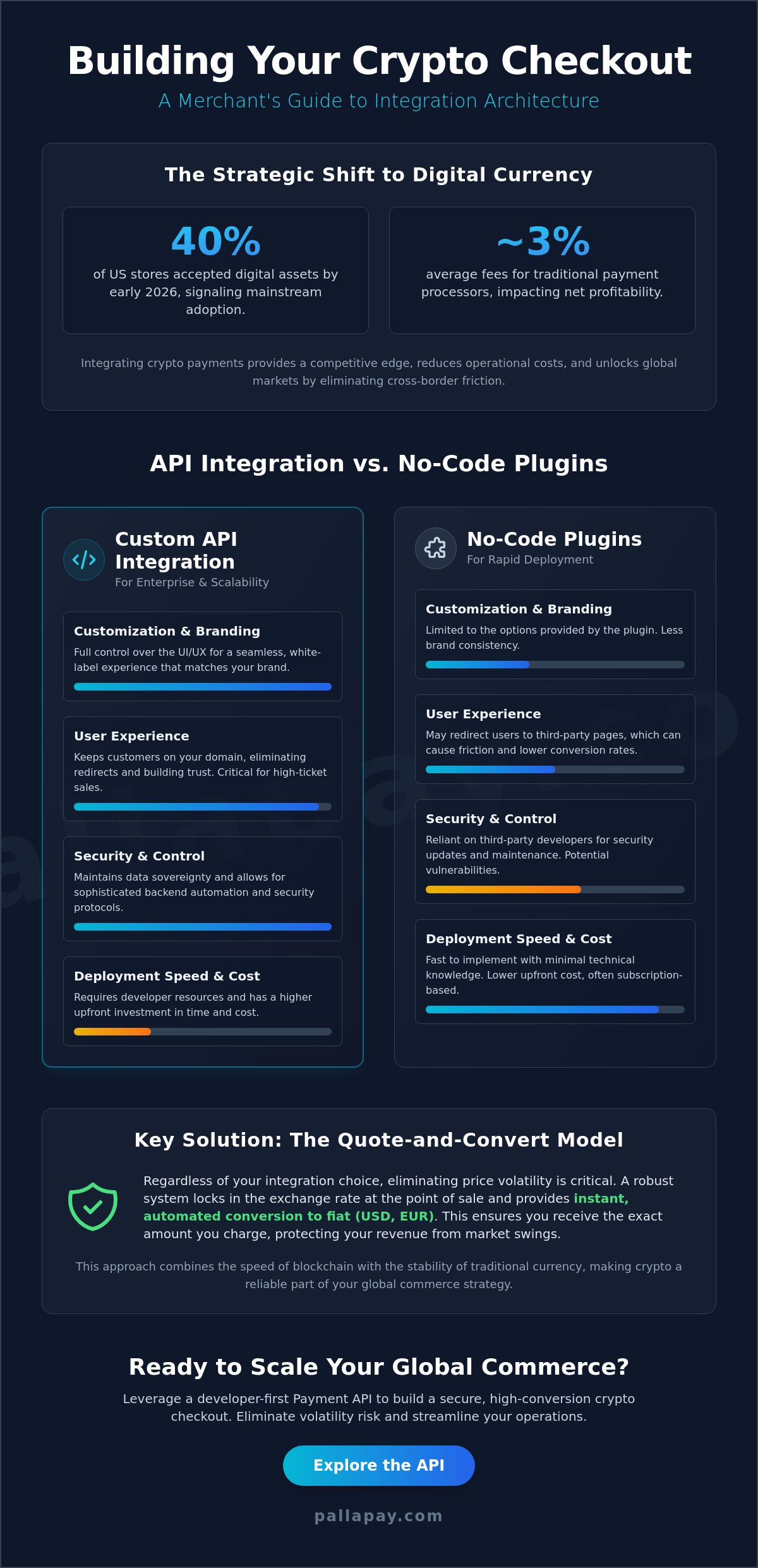

Legacy credit card processors typically extract between 3% and 5% from your hard-earned revenue. Crypto processing operates with lean efficiency, drastically reducing these overhead costs by cutting out the intermediaries. Additionally, the immutable nature of blockchain transactions eliminates the risk of chargeback fraud, which costs merchants billions annually. For a retail operation generating $1,000,000 in annual sales, transitioning to crypto-based settlement can reclaim a substantial portion of profit that would otherwise be lost to intermediary fees and disputed payments.

Capturing the High-Net-Worth Consumer

High-net-worth, crypto-native consumers actively seek out merchants who respect their digital-first lifestyle. They prefer brands that offer the security and speed they’ve come to expect from blockchain technology. Being a “crypto-ready” destination provides a clear marketing advantage, positioning your brand as a tech-savvy leader in a competitive market. Implementing these retail store solutions allows you to capture a share of the $1.5 trillion digital asset market while ensuring your business is prepared for the inevitable global financial evolution.

Essential Features of a High-Performance Crypto POS Terminal

High-performance hardware is the operational heart of a modern storefront. A crypto pos machine for small business must do more than just process transactions; it must integrate seamlessly with global liquidity pools. Multi-currency support is a non-negotiable requirement for professional growth. While Bitcoin remains a primary asset, stablecoins like USDT and USDC provide the price certainty required for retail inventory management. According to the U.S. Chamber of Commerce technology report, small businesses are increasingly leveraging digital tools to stay competitive, and crypto-readiness is a significant part of that evolution.

Instant QR code generation ensures a frictionless checkout experience where customers scan, confirm, and pay in seconds. This speed is matched by robust security protocols, including end-to-end encryption and MSB-compliant processing. These features protect your enterprise from external threats while ensuring every transaction meets global regulatory standards. Staff shouldn’t need a degree in computer science to manage these systems. Modern interfaces use visual cues and simplified workflows to ensure that a crypto payment is as easy to handle as a standard debit card tap.

Real-Time Fiat Settlement Mechanics

Volatility is the primary concern for most merchants, yet high-performance terminals solve this through instant conversion. When a customer pays in a digital asset, the system settles it into fiat immediately. This process fuels your daily cash flow and provides the ready capital needed for high-impact gold and USD CFD trading. Accessing fiat settlement products allows you to lock in value at the moment of sale, effectively turning your retail revenue into a stable investment fund.

Connectivity and Hardware Durability

Choosing the right crypto pos machine for small business depends on your specific retail environment. Standalone handheld terminals offer mobility and built-in thermal printing for physical receipts, making them ideal for restaurants and boutiques. These units require robust battery life and 5G or dual-band Wi-Fi connectivity to prevent downtime during peak hours. Conversely, integrated tablet-based software provides larger interfaces for complex inventory management. Both options should support digital receipts to align with modern consumer preferences. If you’re looking to streamline your operations further, integrating a professional payment API can bridge the gap between your physical store and your digital accounting systems.

From Retail Revenue to Financial Freedom: Leveraging CFDs and Gold

While a crypto pos machine for small business simplifies daily transactions, its true value lies in its role as a liquidity engine. Most business owners view sales as the end of a process. Professional entrepreneurs see them as the beginning of a wealth-building cycle. By converting retail sales into digital assets, you bypass the sluggishness of legacy finance. This transition allows for a psychological shift from a traditional shopkeeper to a strategic financial investor. You’re no longer just managing inventory; you’re managing a portfolio of liquid capital that can be deployed into global markets at a moment’s notice.

This strategic evolution is about more than just modernizing your checkout counter. It’s about securing your financial future by moving capital into assets that outpace inflation. When your daily revenue is settled in digital form, the path to diversified wealth becomes direct. You can transition from a successful retail day to an active position in the world’s most liquid markets without waiting for external approvals or clearing houses.

The Power of Gold and USD CFD Trading

Gold trading (XAU/USD) has long been the standard for hedging against economic volatility. In the context of 2026, where state-level cryptocurrency legislation is becoming more defined, the ability to move from crypto to commodities is a powerful advantage. Contracts for Difference (CFDs) enable you to profit from the price fluctuations of gold or the US dollar without the logistical burden of physical ownership. This flexibility is essential for those seeking significant financial life changes through market participation. CFDs allow for leveraged exposure to global markets, meaning you can control a larger position with a smaller amount of initial capital. This leverage accelerates the transformative potential of your retail revenue when managed with professional discipline.

Liquidity: The Bridge Between Sales and Strategy

Speed is the most critical factor in successful trading. Traditional settlement delays often mean missing high-yield opportunities in the forex market. When you utilize a crypto pos machine for small business, your revenue is settled instantly into stable digital assets. This provides the immediate liquidity needed to fund a trading account at the exact moment a market signal appears. Utilizing professional crypto off-ramp services ensures that your capital moves at the speed of the internet. You can transition from a retail sale to an XAU/USD position in minutes. This seamless flow eliminates the barriers that once kept small business owners out of institutional-grade trading environments, allowing your business to act as its own investment fund.

Buying Guide: How to Evaluate Crypto POS Providers for Your Small Business

Selecting a crypto pos machine for small business is a decision that dictates your future financial agility. You shouldn’t view this as a simple hardware purchase; it’s an investment in a professional partnership. Evaluate fee structures with a focus on long-term scalability. While some providers offer monthly subscription models, others favor transaction-based fees. Your choice should align with your volume, especially if you intend to use that revenue for high-impact USD CFD trading. Compliance is equally critical. Ensure your provider holds Money Services Business (MSB) registration. This ensures your capital is handled with institutional-grade security, particularly as the GENIUS Act of July 2025 and the July 18, 2026, regulatory deadlines bring tighter federal frameworks to digital assets.

Integration capabilities are the difference between a siloed tool and a growth engine. Your terminal must communicate with your existing accounting software to prevent manual errors and streamline tax reporting under the 2026 PARITY Act. If you manage multiple locations, a centralized dashboard is essential for maintaining a bird’s-eye view of your global liquidity. This level of control allows you to monitor sales trends and move capital into your forex account without friction. Professional growth requires a system that supports your evolution from a local merchant to a global market participant, ensuring you can capitalize on XAU/USD movements as they happen.

Hardware vs. Software-Only Solutions

While mobile apps offer a low barrier to entry, a physical terminal remains superior for building customer trust and operational speed. Dedicated hardware facilitates faster transaction processing and provides a more professional checkout experience that customers expect in a retail environment. In 2026, Near Field Communication (NFC) is a standard requirement, allowing for tap-to-pay functionality that mimics traditional card payments. This ease of use is a core component of the crypto POS machine: the complete guide, which details how hardware durability and specialized scanners impact your daily revenue cycles.

Customer Support and Maintenance

Technical assistance is mission-critical when your hardware is the gateway to your revenue. Look for providers that offer comprehensive support and regular software update cycles to ensure your system remains secure. This future-proofs your business against new blockchain protocols and emerging security threats. Avoid providers with hidden setup costs or complex hardware configurations that delay your launch. A reliable partner handles the background mechanics so you can focus on strategic gold trading and wealth preservation. If you’re ready to upgrade your infrastructure, you can explore our retail store solutions designed for high-performance commerce.

The Pallapay Advantage: Your Partner in Global Financial Growth

Pallapay serves as the definitive destination for merchants who demand more than basic payment processing. By deploying a crypto pos machine for small business through our ecosystem, you aren’t just adopting a tool; you’re securing a strategic partnership. We bridge the gap between disruptive retail innovation and institutional financial reliability. Our platform ensures that every transaction contributes to your broader financial evolution, providing the high-speed liquidity required to excel in Gold and USD CFD markets. While competitors focus solely on transaction volume, we focus on the utility of your capital.

The integrated ecosystem is built for maximum efficiency. Your retail revenue flows seamlessly into an environment where capital can be redeployed through the Pallapay Mastercard or managed via our OTC crypto exchange. This connectivity is what allows a business owner to transition from managing a storefront to executing high-impact trades in the XAU/USD pair. We handle the complex background processes, from instant fiat conversion to regulatory alignment, so you can focus on the transformative potential of the global market. Our infrastructure is designed to make complex technical conversions feel like standard, effortless business operations.

Total Ecosystem Integration

Managing your financial life shouldn’t involve juggling multiple platforms. The Pallapay dashboard offers a comprehensive view of your assets, from retail sales to trading balances, providing a single source of truth for your liquidity. For businesses looking to scale, our payment API provides a robust framework for global expansion and custom technical flows. This level of technical integration is underpinned by our commitment to crypto security in 2026, ensuring your data and funds remain protected against emerging threats. You gain the stability of an established financial partner while leveraging the speed of modern blockchain technology.

Next Steps: Transform Your Business Today

Transitioning to a digital-first financial model is a straightforward process. You can apply for a professional POS terminal by following three simple steps on our platform, moving quickly from application to implementation. Our team is available to discuss how our crypto wallet and liquidity management services can support your specific growth goals. Don’t let legacy banking delays limit your potential for wealth creation or market entry. Contact our specialists today to secure your hardware and begin leveraging your retail revenue for a more prosperous financial future.

Secure Your Financial Future with Modern Liquidity

Adopting a crypto pos machine for small business represents more than a technological upgrade. It marks your entry into a global financial ecosystem where retail revenue is instantly converted into the liquid capital required for strategic growth. We’ve explored how instant fiat settlement removes the barriers to high-impact gold and USD CFD trading. This transition allows you to capture market movements in real-time, effectively turning your daily sales into a launchpad for long-term wealth creation. Professional growth depends on the speed of your capital; blockchain technology ensures that speed is absolute.

Pallapay provides the institutional-grade reliability your enterprise deserves. With official MSB registration in the US and Canada, our award-winning infrastructure serves merchants across 180+ countries. You don’t have to wait for legacy bank clearances to act on a forex signal. Instead, you can leverage seamless fiat settlement to fund your trading account and secure your financial life. This integrated approach turns every customer transaction into a strategic advantage.

Equip your business with the Pallapay Crypto POS and unlock global financial markets today.

The evolution of global commerce is inevitable. By choosing a partner that prioritizes speed, security, and compliance, you’re positioning your enterprise at the forefront of this transformation. Start your journey toward financial freedom today.

Frequently Asked Questions

How does a crypto POS machine actually settle in fiat currency?

A crypto POS terminal settles in fiat by executing an immediate exchange at the exact moment of a transaction. When a customer pays with a digital asset, the payment gateway locks the current market rate and converts the funds into your preferred currency, such as USD. This automated process eliminates exposure to price volatility, ensuring the exact retail value of your sale is preserved for immediate operational use.

Is it legal for my small business to accept cryptocurrency payments?

Accepting digital assets is legal in most global jurisdictions, provided you comply with local financial regulations. In the United States, the GENIUS Act of 2025 and the subsequent 2026 regulatory framework established clear guidelines for stablecoin transactions. Professional merchants should ensure their provider is an officially registered Money Services Business (MSB) to maintain full compliance with state and federal reporting requirements while protecting their commercial interests.

What are the transaction fees compared to traditional credit cards?

Processing digital assets typically incurs significantly lower costs than legacy credit card networks. While traditional processors often charge between 3% and 5% per transaction, crypto processing fees generally range from 0.4% to 2%. This reduction in overhead allows small businesses to retain a larger portion of their revenue, which can be strategically redeployed into high-impact investments like gold or currency markets.

Can I use the funds from my crypto POS to trade Gold or Forex CFDs?

You can directly leverage your retail revenue for market participation through integrated liquidity bridges. Using a crypto pos machine for small business allows you to settle funds into stable digital assets that are compatible with professional trading accounts. This seamless pipeline enables you to move from a retail sale to an active position in XAU/USD or USD CFDs without the delays associated with traditional banking systems.

Do I need a special bank account to use a crypto POS terminal?

You don’t necessarily need a specialized bank account to begin accepting crypto payments through a professional terminal. Most systems settle funds into a digital wallet or a dedicated merchant account within the provider’s ecosystem. From there, you can choose to transfer funds to a standard bank account via a crypto off-ramp or use an integrated Mastercard for direct access to your liquid capital.

What happens if a customer wants a refund on a crypto payment?

Refunds are typically processed by issuing the digital asset equivalent of the original fiat purchase price at the current market rate. The merchant initiates the refund through their dashboard, and the system calculates the necessary amount of cryptocurrency to return to the customer’s wallet. This process ensures the customer receives the correct value while the merchant avoids losses due to asset price fluctuations since the original sale.

How long does it take to set up a Pallapay POS machine for my store?

Setting up a Pallapay POS terminal is a streamlined process designed for rapid deployment. Once your application is reviewed and your account is verified, the hardware is configured and shipped to your location. Most merchants can begin accepting digital payments within a few business days of receiving their terminal. The intuitive interface ensures that your retail staff can manage transactions immediately with minimal technical training.

Which cryptocurrencies are most commonly used for in-store payments in 2026?

In 2026, regulated stablecoins like USDT and USDC are the most common assets used for retail commerce due to their price stability. These are often preferred by merchants following the full implementation of the GENIUS Act. However, Bitcoin and Ethereum remain staple options for high-net-worth consumers. A professional terminal supports a multi-currency environment, allowing you to cater to diverse customer preferences while maintaining secure, instant settlement.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.