With crypto transactions now accounting for up to 26% of total revenue at merchants that have adopted the technology, the decision to integrate digital assets is no longer a speculative experiment. It is a strategic necessity for global commerce. However, for most organizations, the primary hurdle isn’t interest; it’s the challenge of knowing how to choose a crypto payment processor that satisfies legal, financial, and technical stakeholders. You likely feel the pressure to innovate while facing internal resistance regarding price volatility and the evolving regulatory landscape of 2026.

This guide empowers you to master a strategic framework for selecting a partner that offers institutional-grade security and seamless utility. We’ll provide a defensible business case to help you secure executive buy-in and a vetting checklist to ensure your chosen provider handles complex background processes with absolute reliability. By the end of this article, you’ll have a clear roadmap for launching a low-risk pilot program that bridges the gap between disruptive technology and established financial practices. We will move quickly from high-level value propositions to the functional evidence required for a successful transition.

Key Takeaways

- Identify how to align internal decision-makers by presenting the “hands-off” settlement model that eliminates price volatility risks for the organization.

- Master the criteria for how to choose a crypto payment processor by verifying institutional-grade security and MSB registrations across major global jurisdictions.

- Quantify the operational impact of switching to digital asset processing, including a significant reduction in transaction fees and achieving near-instant T+0 global settlement.

- Streamline your technical transition using a robust Payment API that integrates directly with existing ERP systems for a frictionless operational flow.

- Design a structured 90-day pilot program to validate performance metrics and transition from theoretical planning to live, low-risk commercial reality.

Defining the Strategic Need: Stakeholder Mapping and the “Hands-Off” Model

By 2026, digital assets have transitioned from speculative investments into a critical layer of the global financial infrastructure. For an enterprise, the decision to integrate these assets isn’t about joining a trend; it’s about optimizing the settlement layer of the business. Understanding how to choose a crypto payment processor requires a shift in perspective. You aren’t just looking for a technical plug-in. You’re selecting a strategic partner that functions as a modern payment service provider, bridging the gap between blockchain innovation and institutional requirements.

The most successful implementations in 2026 utilize the “Hands-Off” model. This approach allows your business to capture the benefits of decentralized finance without the volatility risks. You accept digital assets from global customers, but your internal treasury never touches the tokens. Instead, the processor facilitates an immediate conversion, ensuring your books remain denominated in traditional currency. This eliminates the need for complex digital asset accounting while still accessing a global market of over 430 million crypto users. It’s a professional bridge that connects established practices with modern advancements.

The Role of Fiat Settlement in Risk Mitigation

Institutional stability relies on predictable cash flow. A robust fiat settlement system acts as the essential bridge between blockchain speed and banking stability. This approach simplifies tax reporting because every transaction has a clear fiat value at the moment of sale. It fits perfectly into standard accounting workflows, removing the hurdle of fluctuating balance sheets that often stalls executive approval. By receiving local currency directly, you maintain financial reliability while offering your customers the cutting-edge utility they expect.

Tailoring the Message for Each Stakeholder

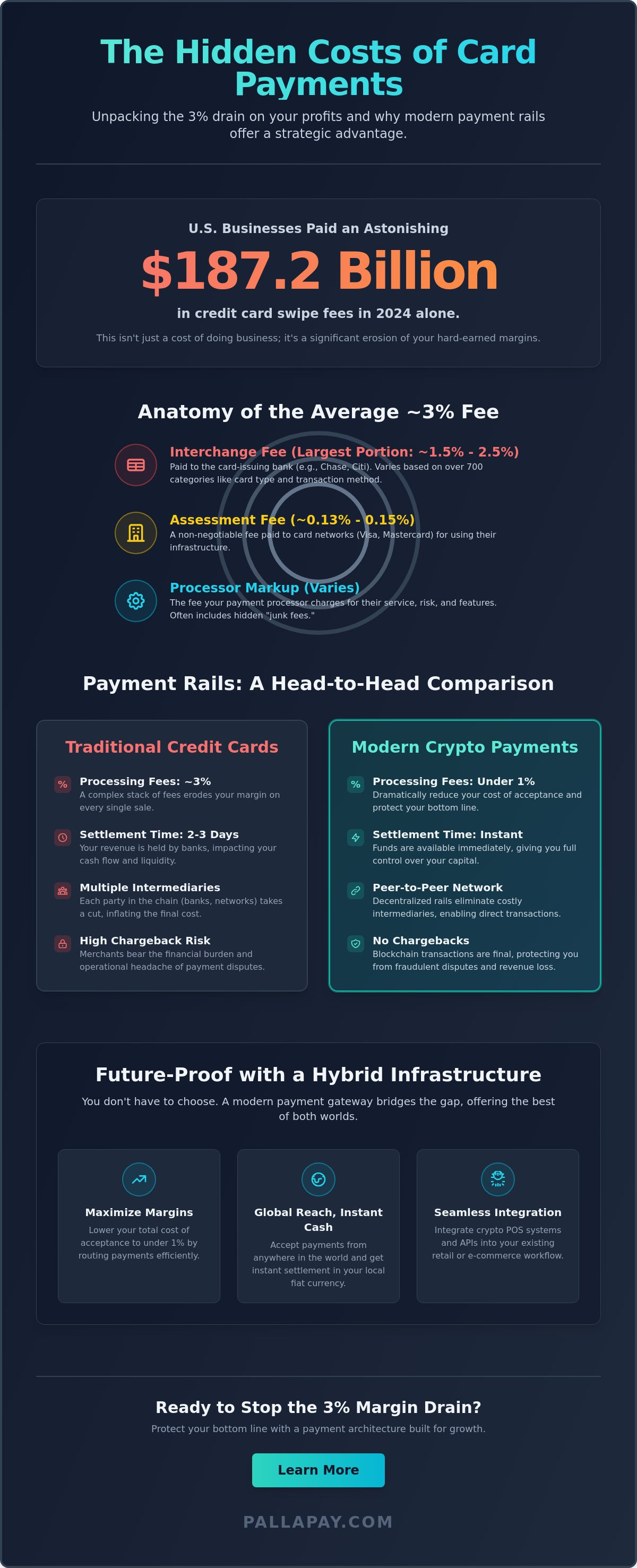

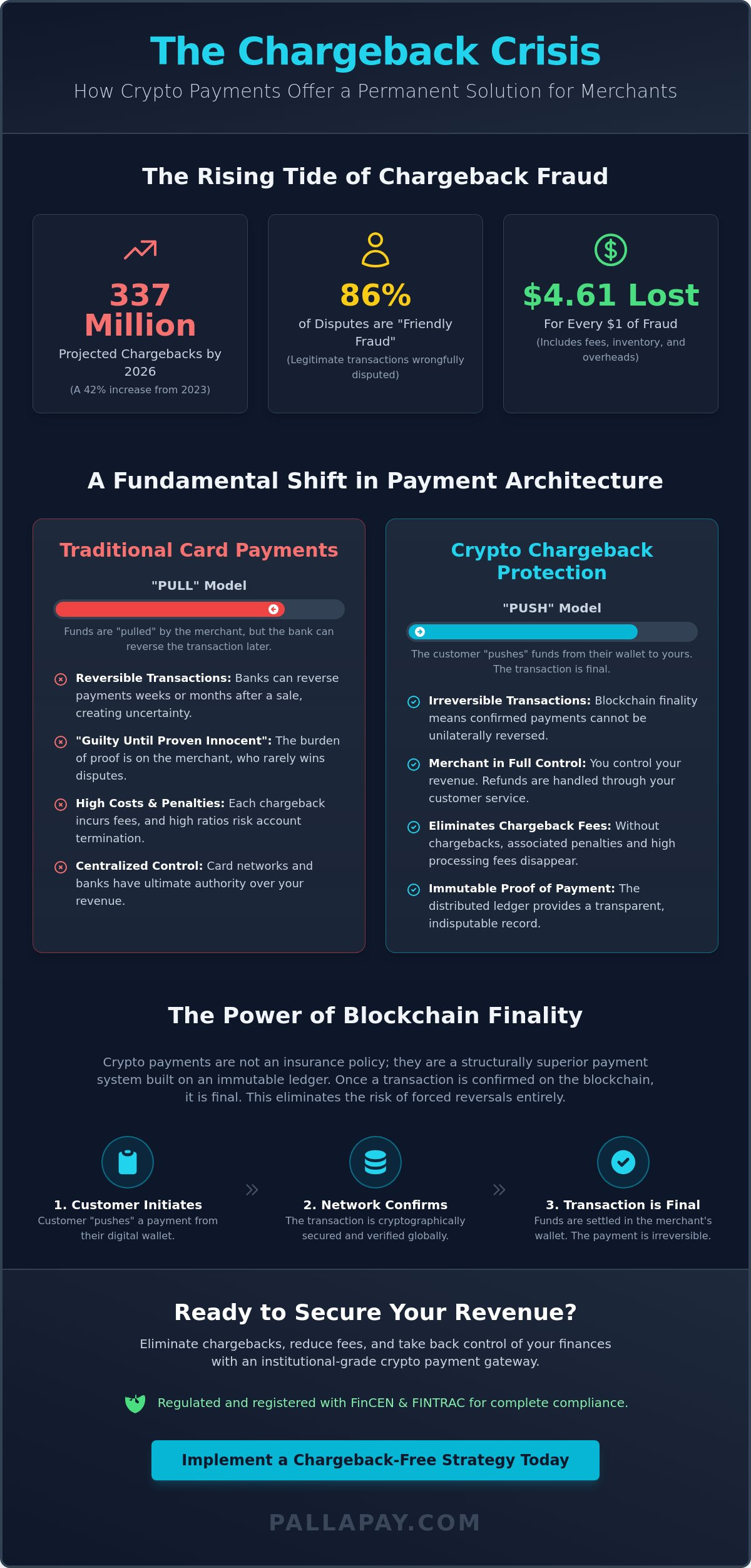

Securing internal buy-in requires speaking the language of each department. The CFO needs to see how crypto reduces cross-border friction. Traditional international card fees often exceed 3.5%, but crypto processing typically sits near 1%. Additionally, the elimination of chargeback fraud provides a direct boost to the bottom line. Mastering how to choose a crypto payment processor means identifying a partner that satisfies these diverse departmental needs simultaneously.

Your Legal team will focus on risk transfer. They want a partner that is a registered Money Services Business (MSB) to handle the heavy lifting of compliance. Meanwhile, the CMO will be interested in market expansion. Accepting crypto allows the brand to capture high-net-worth, crypto-native consumers who prioritize privacy and speed. By framing the choice as a multi-departmental win, you transform a technical request into a strategic business case that drives long-term growth.

Vetting Compliance and Security: The Institutional Checklist

Institutional trust is built on a foundation of rigorous regulatory adherence and technical resilience. When evaluating how to choose a crypto payment processor, the first point of verification must be the provider’s legal standing in key financial markets. A reputable partner should hold Money Services Business (MSB) registrations in major jurisdictions, specifically the United States and Canada. These registrations signify that the entity operates under the supervision of federal financial intelligence units, providing a necessary layer of accountability for your legal department.

A global footprint is equally vital for modern commerce. A processor capable of serving 180+ countries ensures that your business can scale without encountering regional payment silos. This expansive reach must be paired with institutional-grade KYC (Know Your Customer) and AML (Anti-Money Laundering) protocols. These systems don’t just satisfy regulators; they protect your brand by filtering out high-risk actors before they interact with your ecosystem. Blockchain transparency actually enhances these efforts, as it allows for real-time tracking of asset provenance in ways traditional banking cannot match.

Regulatory Compliance as a Corporate Shield

Operating within a regulated framework transforms compliance from a hurdle into a competitive advantage. A processor that manages the complexities of global financial laws effectively offloads the regulatory burden from your internal teams. By partnering with a registered MSB, you ensure that every transaction adheres to the latest global standards. Blockchain transparency facilitates a new era of accountability where immutable ledgers provide definitive proof of funds and transaction history for auditing purposes.

Institutional Security Standards

Technical resilience is the second pillar of the vetting process. You should look for providers that prioritize advanced crypto security measures such as multi-signature authorization and cold storage for asset protection. Unlike traditional payment systems that rely on vulnerable centralized databases, blockchain utilizes cryptographic immutability to secure transaction data. Implementing a reliable Crypto Payment Gateway allows you to automate these security checks seamlessly. To assess a provider’s technical strength, use this essential checklist:

- Proven Longevity: Does the provider have a documented history in the fintech sector dating back to at least 2018?

- Infrastructure: Are assets kept in air-gapped cold storage rather than hot wallets?

- Redundancy: Does the system feature multi-signature protocols to prevent single points of failure?

- Global Reach: Can the provider facilitate transactions and settlements across 180+ countries?

Choosing a partner with a long-standing reputation in the industry ensures that your transition to digital payments is secure and sustainable. Assessing these factors carefully is the definitive way to understand how to choose a crypto payment processor that will serve as a reliable strategic facilitator for your organization’s growth.

Quantifying the Value Proposition: Fees, Speed, and Global Reach

Selecting a partner isn’t just a technical hurdle; it’s a fiscal optimization strategy. When you evaluate how to choose a crypto payment processor, the most immediate metric is the impact on your bottom line. Traditional international credit card transactions often carry fees exceeding 3.5% once cross-border surcharges and currency conversion costs are tallied. In contrast, crypto processing fees typically hover around 1%. For high-ticket ecommerce operations, this 2.5% delta translates directly into preserved margins and increased competitive agility.

The total cost of ownership (TCO) extends beyond the transaction fee. A sophisticated partner eliminates the hidden costs of traditional finance, such as setup delays and recurring maintenance charges for legacy hardware. By adopting an integrated digital infrastructure, you replace fragmented payment silos with a unified flow. This efficiency is a core component of the “Hands-Off” model discussed earlier, where the complexity of the background process is handled entirely by the provider, leaving you with clean, predictable fiat results.

The Financial Impact of Instant Settlement

Institutional liquidity depends on the velocity of capital. While traditional systems rely on the multi-day SWIFT cycle, crypto enables a “T+0” reality. This means funds are available for operational use almost immediately after a transaction is confirmed. Immediate fund availability provides a significant working capital advantage, allowing businesses to reinvest capital faster than ever before. To protect against market fluctuations, a professional processor facilitates instant conversion to stable currencies like USD or EUR, ensuring that the value captured at the point of sale is the exact value that hits your account.

| Payment Method | Settlement Cycle | Standard Fees |

|---|---|---|

| International Credit Cards | 2 to 7 Business Days | 3.5% or higher |

| Bank Wires (SWIFT) | 1 to 5 Business Days | Variable + Flat Fees |

| Crypto Payment Processor | Instant (T+0) | Approximately 1% |

Unlocking New Global Markets

Global commerce is shifting toward regions where digital assets are a primary payment method. For retail stores, accepting crypto is a powerful tool to attract international travelers who prefer the security and ease of digital wallets over carrying physical currency. This reduction in friction is equally transformative for cross-border B2B transactions. Knowing how to choose a crypto payment processor that prioritizes speed and global reach allows your business to bypass the bottlenecks of traditional banking, positioning you as a forward-thinking strategic partner in the inevitable global evolution of finance.

The Implementation Roadmap: Integration and Operational Flow

Transitioning from a strategic framework to operational reality requires a structured, multi-phase approach. Knowing how to choose a crypto payment processor isn’t just about the initial sign-up; it’s about evaluating how the technology will live within your current ecosystem. A successful rollout prioritizes technical compatibility and internal readiness to ensure that digital asset acceptance becomes a standard, effortless business operation. By following a logical progression, you can mitigate technical risks while maximizing the efficiency of your new payment layer.

- Step 1: Selection of a Technical Partner. Focus on providers offering a robust Payment API that supports high-volume throughput and secure endpoints.

- Step 2: Technical Integration. Connect the processor to your existing ERP or shopping cart systems to automate the flow of transaction data.

- Step 3: Internal Team Training. Educate finance and accounting departments on using the merchant dashboard for real-time reporting and reconciliation.

- Step 4: Infrastructure Deployment. For brick-and-mortar locations, deploy a physical Crypto POS Machine to facilitate in-person digital asset payments.

- Step 5: Pilot Launch. Initiate a controlled 90-day pilot program to gather performance data and refine operational workflows before a full-scale launch.

Seamless API and POS Integration

Modern crypto payment gateways are designed for plug-and-play efficiency, allowing for a “hands-off” implementation with minimal IT overhead. This streamlined architecture ensures that your technical team can focus on growth rather than troubleshooting complex background processes. When evaluating partners, prioritize those that offer comprehensive documentation and reliable technical support to maintain constant uptime for your global operations. A professional bridge between legacy systems and blockchain technology should feel frictionless and secure from the first transaction.

Reporting and Reconciliation

Institutional reliability is maintained through clear visibility into every transaction. A critical component of how to choose a crypto payment processor is assessing the reporting capabilities that bridge blockchain data with traditional ledgers. Advanced merchant dashboards simplify the tracking of digital asset sales by providing a unified view of your global revenue. These systems facilitate the automated generation of tax-ready reports, denominated in your preferred fiat currency, which aligns perfectly with standard accounting practices. This centralized interface allows management to oversee multiple store locations or ecommerce channels simultaneously, ensuring total operational control. To begin your integration, explore our API for crypto payments and see how it can accelerate your progress.

Proposing the Pilot: Moving from Theory to Operational Reality

The final stage in mastering how to choose a crypto payment processor involves transitioning from theoretical research to a controlled operational environment. A structured 90-day pilot program is the most effective way to minimize perceived organizational risk while gathering primary data. This timeframe allows your finance team to complete three full monthly reconciliation cycles, providing a clear window into the efficiency of the “Hands-Off” settlement model. By limiting the initial scope to a specific ecommerce channel or a select group of retail locations, you can validate the technology without overextending internal resources.

A pilot program is more than a technical test; it is a strategic R&D investment in the future of your global financial infrastructure. It provides the empirical evidence needed to satisfy the last remaining concerns of your stakeholders. If the results align with your projections, you have a documented roadmap for a full-scale rollout. If adjustments are required, the modular nature of modern APIs allows you to refine the integration or revert to legacy systems without disrupting your core business operations. This reversibility is a key component of institutional-grade risk management.

Setting Realistic KPIs for Stakeholders

Success in the early stages should be measured through operational efficiency and error reduction rather than just raw transaction volume. You should track the exact fee savings achieved by bypassing traditional card networks, alongside the reduction in chargeback-related administrative costs. Quantitative metrics are vital, but qualitative feedback is equally important. Gathering insights from your first crypto-native customers can reveal a significant “first-mover” brand advantage in your sector. This data demonstrates to the CMO and CFO that the business is successfully capturing a high-growth, high-net-worth demographic that prioritizes speed and security.

The Final Pitch: Why 2026 is the Inflection Point

The global payments market is no longer waiting for crypto to mature; the infrastructure is already institutional-grade. In 2026, the greatest risk is no longer the volatility of the asset, but the competitive risk of being the last to adopt a more efficient settlement layer. Businesses that fail to integrate digital assets face higher overhead and slower capital velocity than their forward-thinking peers. The bridge approach we have outlined is sophisticated, regulated, and specifically designed to mitigate traditional risks. It is the definitive path for connecting established practices with the inevitable global evolution of commerce.

The most successful implementations are those built on a foundation of expert guidance and reliable technology. You don’t have to build this business case alone. To ensure your pilot program is optimized for both security and growth, consult with a Pallapay specialist to build your custom business case and take the first step toward a more efficient financial future.

Securing Your Position in the Future of Global Commerce

The decision to integrate digital assets marks a transition from traditional limitations to global scalability. By aligning your stakeholders through a risk-mitigated “Hands-Off” model and vetting partners against strict institutional standards, you ensure that innovation serves your bottom line. The roadmap we’ve established moves beyond technical integration to focus on long-term financial stability and market expansion. Mastering how to choose a crypto payment processor is the definitive step in transforming your payment infrastructure into a competitive advantage for 2026 and beyond.

As an institutional partner since 2018, we provide the stability and reach required for enterprise-level growth. Our ecosystem is MSB registered in the USA and Canada, supporting a global presence across 180+ countries. You’re now ready to move forward with the confidence that your background processes are handled by a proven industry leader. Explore Institutional Fiat Settlement Solutions to begin your transition today. Your organization is well-positioned to lead the next evolution of commerce.

Frequently Asked Questions

How do I explain crypto price volatility to my CFO?

Explain that price volatility is entirely avoided by using a processor that facilitates instant conversion to fiat. The merchant receives the exact local currency value of the sale at the moment of the transaction. This ensures that your internal treasury never interacts with fluctuating asset prices. It’s a strategic utility that provides the speed of blockchain with the stability of the traditional banking system.

Is it legal for a regulated business to accept cryptocurrency payments?

Accepting digital assets is entirely legal for regulated businesses that partner with licensed Money Services Businesses. These processors manage the complex regulatory requirements, including KYC and AML protocols, on your behalf. You should verify that your provider holds valid registrations in jurisdictions like the United States or Canada. This partnership ensures your operations remain compliant with global financial standards while expanding your reach.

Do we need to hold cryptocurrency on our company balance sheet?

You don’t need to hold any cryptocurrency on your balance sheet if you opt for a fiat-settlement model. The processor handles the digital asset on the backend and settles the transaction in your preferred currency, such as USD or EUR. This keeps your accounting processes standard and familiar, allowing for seamless use alongside specialized tools like AIA G702 G703 software for construction billing. It’s an efficient way to capture new revenue without changing your fundamental corporate treasury policies.

How long does the technical integration of a crypto gateway typically take?

Most technical integrations for crypto gateways are completed within a few business days using modern, plug-and-play APIs. The process is designed to be efficient, requiring minimal intervention from your IT department. Learning how to choose a crypto payment processor with comprehensive documentation is the best way to ensure a fast rollout. This allows your business to move quickly from a strategic decision to live operations.

What are the main security risks for corporate stakeholders to consider?

The most critical risks involve the security of the gateway and the reliability of the settlement partner. Stakeholders should prioritize providers that utilize multi-signature authorization and air-gapped cold storage for all assets. Because blockchain transactions are final and immutable, they eliminate the risk of chargeback fraud that plagues traditional credit cards. A vetted partner with a long history in fintech provides the necessary institutional-grade protection.

How do crypto processing fees compare to traditional credit card merchant fees?

Crypto processing fees are substantially lower than traditional merchant fees, typically sitting at approximately 1%. In contrast, international credit card transactions often cost 3.5% or more when factoring in cross-border surcharges. This significant delta is a core part of the value proposition for businesses researching how to choose a crypto payment processor. Lowering these overheads directly improves your operational margins and capital efficiency.

Can we receive settlements in our local fiat currency immediately?

You can receive settlements in your local fiat currency almost immediately through a T+0 settlement cycle. This is a major improvement over the standard multi-day SWIFT cycle found in traditional banking. Funds are converted and settled into your account, providing a clear advantage for working capital management. It ensures that your liquidity is never trapped in the settlement process, allowing for faster reinvestment and global growth.

What happens if a stakeholder is fundamentally opposed to digital assets?

Position the integration as a strategic tool for cost reduction and global market expansion rather than a speculative investment. Emphasize that the “Hands-Off” model ensures the company never touches the digital assets directly. By focusing on the data from a low-risk pilot program, you can demonstrate tangible improvements in transaction speed and fee savings. This shifts the focus from the asset’s reputation to the technology’s institutional utility.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.