In 2026, the success of a retail business in the UAE no longer depends on which bank you use, but on your ability to accept any asset a customer carries. The future of retail payments in uae has shifted toward absolute payment agnosticism, where the distinction between traditional fiat, the Digital Dirham, and cryptocurrency has effectively vanished at the point of sale. While the UAE payments market is projected to reach USD 213.43 billion this year, many merchants still struggle with high transaction fees and the complexity of modernizing their checkout systems.

You likely feel the pressure to adapt as customers demand faster, more diverse ways to pay without the friction of legacy systems. This article explores the transformative technologies and regulatory shifts, such as the full retail launch of the Digital Dirham, that are redefining commerce. We’ll examine how your business can leverage tools like crypto POS machines and instant fiat conversions to reduce costs and capture growth. From the implementation of the Jaywan card scheme to seamless API integrations, you’ll learn how to position your brand as a forward-thinking strategic partner in this inevitable global evolution.

Key Takeaways

- Adapt to a digital-first landscape where government mandates and consumer preferences have marginalized physical cash in favor of digital assets.

- Enhance security and speed by integrating biometric authentication and unified QR code systems into your existing retail environment.

- Accept Bitcoin and USDT at the point of sale with instant conversion to AED to ensure liquidity and eliminate price volatility.

- Audit your current terminal hardware to ensure seamless compatibility with the future of retail payments in uae and multi-asset transaction protocols.

- Deploy professional crypto POS machines and payment gateways to act as a reliable bridge between traditional commerce and modern financial innovation.

The Great Transition: From Cash-Dependency to a Digital-First UAE Economy

The UAE is entering a phase where physical currency is rapidly becoming a relic of commerce history. By 2026, the The Great Transition: From Cash-Dependency to a Digital-First UAE Economy has been accelerated by decisive government mandates that prioritize a cashless society. This shift isn’t just about convenience; it’s a structural realignment of the national economy. Retailers who once relied on physical notes now manage liquidity through digital channels that offer real-time settlement and absolute transparency. The future of retail payments in uae is defined by this move toward a multi-asset environment where digital hubs replace the traditional leather wallet.

Younger demographics, specifically Gen Z and Millennials, are the primary architects of this change. These consumers don’t just want digital payments; they demand “invisible” experiences where the transaction happens seamlessly in the background. This behavioral shift has led to the decline of the traditional wallet in favor of unified digital hubs. These hubs can hold everything from the Digital Dirham to stablecoins like USDT, allowing for a more fluid exchange of value. The National Payments Systems Strategy has been instrumental here, providing the framework for retail liquidity that moves as fast as the consumer’s digital lifestyle.

Drivers of the Digital Surge

Smartphone penetration in the UAE is among the highest globally, making mobile-first shopping the absolute standard for every household. The Financial Infrastructure Transformation (FIT) program has provided the necessary rails for these innovations to flourish, ensuring that the underlying architecture is as robust as the front-end interface. Security used to be a point of hesitation for many shoppers. Today, it’s a baseline requirement. Consumers expect institutional-grade encryption and biometric protection as a standard feature, ensuring that every transaction is both fast and safe.

Retail Adaptation Challenges

Despite the clear progress, many retail stores still struggle with legacy hardware that creates bottlenecks. Slow checkout lines caused by outdated terminals are a significant friction point that can drive customers away. Overcoming the lingering cultural bias toward cash requires more than just new tech; it requires digital incentives that reward the user for choosing efficiency. The cost of inaction is high. Businesses that fail to integrate a modern payment API risk losing significant market share to tech-forward competitors who offer a frictionless path to purchase. The future of retail payments in uae belongs to those who view payment technology as a strategic asset rather than a back-office expense.

Beyond Contactless: Biometrics, QR Codes, and the Digital Dirham

The future of retail payments in uae is evolving past the simple tap-and-go interaction. While contactless cards were the innovation of the last decade, 2026 is defined by biometric authentication and the integration of sovereign digital currencies. Retailers are now deploying facial and palm recognition systems that link a customer’s physical identity directly to their multi-asset digital hub. This transition eliminates the need for physical hardware on the consumer side, turning the checkout process into a frictionless, “invisible” event that prioritizes security and speed.

Unified QR code ecosystems have also matured, providing a standardized bridge between local merchants and global shoppers. By adopting a single standard, businesses can accept a wide array of international wallets without managing multiple proprietary systems. This simplification is a key driver in the sustained UAE eCommerce market growth, as it reduces the technical barriers for both online and physical storefronts. Additionally, the evolution of NFC technology has turned every mobile device into a potential payment terminal, allowing smaller merchants to accept secure payments without investing in bulky legacy hardware.

The Impact of the Digital Dirham on Retail

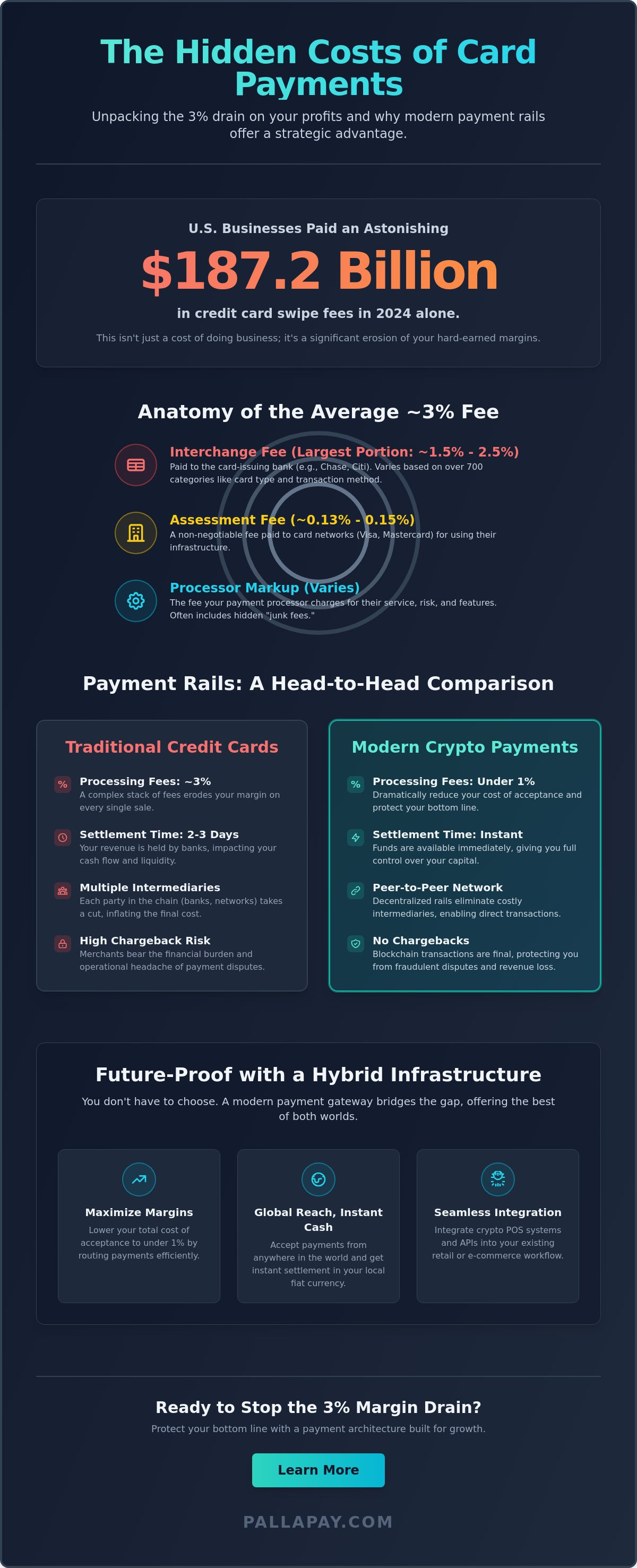

The Digital Dirham is the backbone of 2026 UAE retail. Unlike traditional electronic payments that often involve multi-day clearing cycles, this Central Bank Digital Currency (CBDC) allows for instant merchant settlement. It eliminates intermediary delays, ensuring that liquidity is reflected in a business account the moment a transaction is authorized. Because it operates on a direct government-backed rail, it significantly reduces transaction costs compared to traditional credit card networks. For high-volume retailers, these marginal savings translate into substantial operational capital that can be reinvested into growth. Managing these assets becomes effortless when using a professional ecommerce payment solution designed for real-time settlement.

Visual and Invisible Payments

QR codes serve as a vital tool for cross-border tourists and local residents alike, offering a familiar interface for diverse payment types. High-end retail hubs are increasingly adopting “Just Walk Out” technology, where computer vision and biometrics track purchases and bill the user automatically upon exit. This setup integrates loyalty programs directly into the payment flow, ensuring that discounts and rewards are applied without manual input. If you’re looking to modernize your storefront, you might consider how a crypto POS machine can bridge the gap between these emerging digital assets and your daily fiat requirements.

Cryptocurrency in Mainstream Retail: Bridging Digital Assets and Fiat

With the UAE payments market projected to reach USD 213.43 billion in 2026, the normalization of digital assets has transformed the retail floor from a single-currency environment into a multi-asset gateway. The future of retail payments in uae is increasingly defined by the seamless integration of cryptocurrency into everyday commerce. High-net-worth shoppers frequently prefer brands that offer crypto flexibility, viewing it as a hallmark of modern, tech-savvy service. To accommodate this, retailers are adopting systems that solve the volatility problem through real-time conversion to AED. This ensures that while the customer pays in a digital asset like Bitcoin, the merchant receives the exact fiat value, protecting margins from market fluctuations. This shift is a central theme in the evolving future of payments in the Middle East, where digital assets are moving from speculative investments to functional retail tools.

Compliance remains a top priority for maintaining institutional stability. By partnering with MSB-registered providers, businesses operate within a clear regulatory safety net. This professional oversight ensures that every transaction meets stringent anti-money laundering standards, instilling absolute trust in both the business and the consumer. It’s a strategic move that bridges the gap between disruptive innovation and traditional financial reliability. Using these regulated channels makes complex technical conversions feel like standard, effortless business operations.

Hybrid Ecosystems and Fiat Settlement

Implementing a robust fiat settlement system is the most effective way to protect retail margins from the inherent price shifts of digital assets. These hybrid ecosystems allow merchants to accept diverse payment types while maintaining a traditional accounting flow. Stablecoins like USDT play a critical role here, facilitating low-fee cross-border purchases without the high costs associated with international banking rails. This utility-focused approach ensures that the checkout process remains fast and secure. For a deeper look at these technologies, see our guide on the future of crypto payment gateways.

The Merchant Advantage

Adopting borderless payment options gives UAE retailers a distinct advantage in attracting a global customer base. Blockchain-verified transactions inherently reduce the risk of chargeback fraud, as the decentralized nature of the ledger makes payments final and transparent. This creates a sense of absolute security for the merchant. Beyond the technical benefits, offering these solutions positions your brand as a leader in the global financial evolution. It’s about more than just a transaction; it’s about signaling to your customers that your business is a forward-thinking strategic partner in their financial journey. By adopting these tools, you accelerate your own progress and stay ahead of technological shifts.

Preparing Your Business: A Roadmap for Modernizing Retail Infrastructure

Modernizing for the 2026 environment requires a systematic audit of your existing financial architecture. You must first evaluate your current hardware to ensure full compatibility with NFC protocols and blockchain-based settlement layers. The future of retail payments in uae demands a gateway that handles multi-asset transactions without increasing latency at the checkout counter. If your legacy systems can’t process the Digital Dirham alongside traditional cards, you risk creating operational bottlenecks that frustrate modern consumers. A professional transition involves moving toward a unified system where diverse assets are treated with the same institutional reliability as cash.

To navigate the variety of available options, you can learn more about PaySelect and compare the leading payment gateways and POS systems designed for the UAE’s digital economy.

Staff readiness is equally critical. Your team needs to understand the workflows for biometric authentication and cryptocurrency acceptance to assist customers effectively. This internal knowledge ensures that new technology feels like a supportive tool rather than a complex hurdle. Once your infrastructure is secure, you should market these new capabilities to tech-savvy segments who prioritize speed and safety. High-net-worth shoppers actively seek out merchants who offer the flexibility they’ve grown accustomed to in the digital asset space, whether they are shopping locally or planning high-end international escapes with YAL’OOU Exclusive Yachting & More.

Upgrading the Physical Storefront

The retail store of 2026 requires a crypto POS machine to remain competitive in a cashless economy. These devices do more than just accept payments; they act as the bridge between decentralized assets and your daily accounting needs. By integrating digital payments with your inventory management through robust Payment APIs, you can automate reconciliation and reduce manual errors. This creates a frictionless “tap-and-go” environment that is essential for high-traffic locations where every second of checkout time impacts your bottom line.

Security and Data Privacy

Protecting consumer biometric data is a non-negotiable requirement under UAE privacy laws. You must implement end-to-end encryption for all digital asset transfers to ensure that sensitive information never leaves a secure environment. Hardware security modules are vital in 2026 because they provide an isolated, tamper-resistant environment for the encryption of sensitive biometric and transaction data. This level of security instills absolute trust in your customers, positioning your brand as a reliable strategic partner in their financial journey. Ensuring your providers meet these 2026 regulatory standards is the final step in securing the future of retail payments in uae for your business.

Ready to modernize your checkout experience? Integrate our secure Payment API today to start accepting a wider range of digital assets with instant fiat settlement.

Navigating the Evolution with Pallapay: Seamless Payments for the Next Generation

The transition to a digital-first economy requires a partner that understands the delicate balance between disruptive innovation and institutional stability. Pallapay serves as the professional bridge for merchants navigating the future of retail payments in uae, providing the tools necessary to thrive in a multi-asset landscape. As physical cash continues to marginalize, businesses need comprehensive POS solutions that are designed specifically for the modern merchant. We provide an integrated ecosystem that handles the complex background processes of digital asset management, allowing you to focus on your core operations with absolute confidence. Our platform isn’t just a tool; it’s an essential component of your business’s inevitable global evolution.

Complexity and risk are the primary barriers to adopting new payment technologies. Pallapay eliminates these concerns through instant conversion and fiat settlement, ensuring that your retail margins remain protected regardless of market shifts. Whether your customers choose to pay with the Digital Dirham or volatile digital assets, your business receives the exact value in AED. This utility-focused approach makes complex technical conversions feel like standard, effortless business operations. With local expertise and a global reach supporting growth in over 180 countries, we empower you to accelerate your progress without the friction of legacy systems.

The Pallapay Ecosystem

Our ecosystem is designed to be the definitive destination for all your technical financial needs. From sophisticated off-ramp services to institutional-grade OTC desks, we provide the infrastructure for total financial liquidity. The Pallapay Mastercard integration is a signature element of our voice, allowing consumers to spend their digital assets as easily as fiat at any terminal. This seamless flow is particularly vital for the hotels and e-commerce sectors, where the demand for diverse, high-speed payment options is at its peak. By adopting these integrated solutions, you position your brand as a forward-thinking strategic partner in the future of retail payments in uae.

Why Leading Retailers Choose Pallapay

Security is the backbone of every service we provide. We maintain a security-first approach backed by official MSB registrations, ensuring that your operations remain fully compliant with 2026 regulatory standards. Merchants require total financial clarity to make informed decisions, so we provide real-time stats and comprehensive dashboards that track every transaction across your entire network. This transparency builds absolute trust and stability for both professional users and individual shoppers alike. The flow of information is clean and uncluttered, mirroring the efficiency of the operations we facilitate. It’s time to bridge the gap between established practices and modern advancements. Modernize your retail payments with Pallapay today and secure your place in the next generation of commerce.

Mastering the New Standard of UAE Retail Commerce

The transition toward an asset-agnostic economy is accelerating across the region. Merchants must move beyond legacy systems to embrace the Digital Dirham and biometric authentication as standard operational features. The future of retail payments in uae rewards those who provide frictionless, secure, and multi-asset checkout experiences. By integrating real-time conversion tools, you eliminate the risks of price volatility while capturing the growing segment of digital-first shoppers.

Pallapay acts as your professional bridge to this global evolution. We’re MSB Registered in the USA and Canada, supporting operations in over 180 countries with instant fiat settlement in AED and USD. This institutional reliability ensures your business growth is grounded in stability and compliance. Don’t let technological shifts become a barrier to your success. Upgrade your retail business with Pallapay’s Crypto POS and Gateway. Your path to a more efficient, borderless storefront starts with a partner that values precision and speed.

Frequently Asked Questions

What is the most popular payment method in the UAE for 2026?

Digital wallets and contactless POS transactions are the most utilized methods, with point-of-sale systems accounting for 79.92% of the market as of late 2025. The retail launch of the Digital Dirham in March 2026 has further accelerated this trend toward government-backed digital transfers. Merchants are now prioritizing multi-asset terminals to meet the high consumer demand for a completely cashless shopping experience.

Is it legal for UAE retailers to accept cryptocurrency payments?

Retailers can legally accept cryptocurrency by utilizing regulated payment service providers that comply with national financial guidelines. The government has already established a precedent for this through partnerships that allow for the payment of specific service fees using digital assets. By using an MSB-registered gateway, your business ensures that every transaction meets stringent security and anti-money laundering standards while remaining fully compliant.

How does the Digital Dirham differ from traditional online banking?

The Digital Dirham is a Central Bank Digital Currency that holds a 1:1 parity with the physical dirham and serves as official legal tender. Unlike traditional online banking, which relies on commercial bank records and intermediary clearing, the Digital Dirham allows for instant, peer-to-peer settlement. This direct architecture is a fundamental element of the future of retail payments in uae, as it eliminates delays and reduces transaction costs for merchants.

Do I need new hardware to accept biometric payments in my store?

Accepting biometric payments typically requires specialized hardware such as facial recognition cameras or palm-vein scanners integrated into your checkout system. While some advanced mobile devices can facilitate these transactions, a dedicated biometric terminal offers the institutional-grade security needed for high-traffic environments. Upgrading your physical infrastructure is a necessary step to provide the frictionless, “invisible” checkout experiences that 2026 consumers expect.

What are the transaction fees for crypto payments compared to credit cards?

Crypto and CBDC transactions generally offer lower fees because they bypass the complex web of intermediaries and interchange costs associated with traditional credit card rails. By settling transactions over a direct blockchain or the Digital Dirham network, businesses can retain more of their retail margins. These cost efficiencies are especially noticeable during cross-border transactions, where legacy banking fees are often at their highest.

How can I protect my retail business from digital payment fraud?

Protecting your business requires a multi-layered approach that includes biometric authentication and end-to-end encryption for all sensitive data. Blockchain-verified transactions provide an immutable record of payment, which significantly lowers the risk of chargeback fraud compared to traditional methods. Utilizing professional gateways that employ hardware security modules ensures that your transaction data remains isolated and protected from unauthorized access at all times.

Can I receive settlements in AED if my customer pays in Bitcoin?

You can receive your settlements in AED regardless of whether the customer pays in Bitcoin, USDT, or Ethereum. Professional payment providers offer instant fiat conversion that locks in the current exchange rate at the exact moment of the transaction. This process protects your business from the volatility of digital assets while ensuring your bank balance reflects the stable local currency you need for daily operations.

How does the Wage Protection System (WPS) integrate with digital payments?

The Wage Protection System (WPS) benefits from the real-time liquidity and automated reporting provided by a modern digital payment ecosystem. As retail income is processed through digital hubs, the funds can be seamlessly channeled into compliant payroll systems to ensure timely salary transfers. This integration is a key part of the future of retail payments in uae, as it connects consumer spending directly to institutional financial obligations.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.