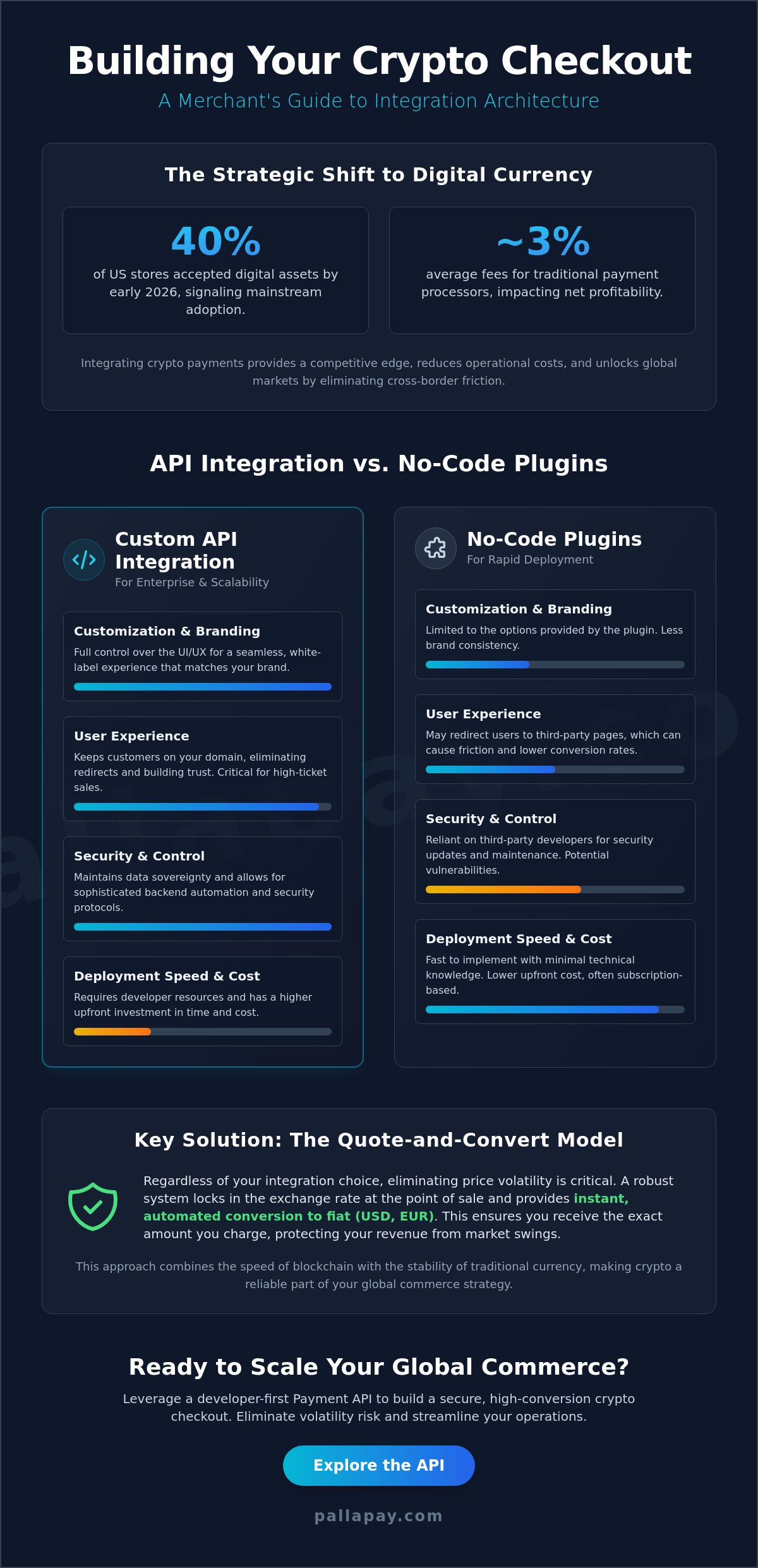

With 61% of U.S. crypto holders now utilizing digital assets for direct payments, a single technical bottleneck in your protocol for troubleshooting crypto payments can instantly derail your conversion rates. You’ve likely felt the frustration of reconciling complex blockchain data with fiat ledgers while managing customer expectations during a ‘stuck’ transaction. It’s a friction point that modern merchants cannot afford in a landscape where over 430 million people globally own digital assets.

Mastering these institutional protocols allows you to do more than just resolve immediate errors; it unlocks a professional gateway to advanced wealth generation. This guide provides the clarity needed to move from basic transaction management to sophisticated financial strategies like Forex and gold CFD trading. We’ll explore how to navigate the 2026 regulatory environment, including the EU’s Transfer of Funds Regulation, to transform your operational hurdles into a resilient engine for growth. Whether you’re optimizing XAU/USD trades or streamlining USD CFD positions, the journey begins with a stable, frictionless payment infrastructure.

Key Takeaways

- Identify the technical sources of transaction friction, including network congestion and gas fee miscalculations, to prevent revenue loss from stalled payments.

- Establish a professional protocol for troubleshooting crypto payments by verifying Transaction IDs (TXIDs) and monitoring network confirmation thresholds in real-time.

- Unlock the transformative potential of digital assets by moving beyond simple processing into high-growth opportunities like gold (XAUUSD) and USD CFD trading.

- Streamline your financial operations using instant fiat settlement and automated Z-reports to bridge the gap between blockchain data and traditional ledgers.

- Scale with institutional confidence by integrating secure infrastructure that spans from OTC crypto exchanges to global retail POS solutions.

Why Crypto Payments Stall: Identifying Common Transaction Friction

Transaction friction represents the operational gap between a user’s initiation and the final merchant settlement. In a high-velocity digital economy, this friction often manifests as “stuck” transactions that disrupt cash flow and erode customer trust. When troubleshooting crypto payments, the first step is recognizing that most delays aren’t random; they’re the result of specific network-level mechanics. Identifying whether a failure originated at the wallet-side or the gateway-side is essential for a fast resolution.

Every transaction enters a mempool, which is a digital waiting room where validators select entries based on priority. If the attached gas fee is too low compared to current network demand, the transaction sits idle. By 2026, with global crypto ownership exceeding 430 million, mempool management has become a critical merchant skill. Understanding where your transaction is waiting allows you to provide accurate timelines to your clients instead of vague excuses.

Blockchain Network Congestion and Gas Optimization

Fluctuating network fees directly impact transaction speed. For B2B payments, setting a 10% to 20% fee buffer ensures your transactions maintain priority during peak congestion. Merchants should use blockchain explorers to verify if a transaction is “pending” in the mempool or if it failed to broadcast entirely. Real-time monitoring of gas prices on networks like Ethereum or Tron is no longer optional; it’s a requirement for institutional reliability.

Address Errors and Protocol Incompatibility

Address errors remain a leading cause of friction. Sending TRC-20 USDT to an ERC-20 address often leads to permanent asset loss due to protocol incompatibility. Implementing checksum-validated address fields in your checkout process reduces these human errors significantly. A core risk factor is that blockchain transactions are irreversible once broadcast to the network. This permanence makes understanding double-spending and other ledger-level security threats vital for any merchant handling significant volume.

Establishing a reliable payment flow isn’t just about retail efficiency; it’s the foundation for transformative wealth generation. Once you’ve mastered transaction stability, you can seamlessly transition funds into a Forex account to trade Gold (XAUUSD) or USD CFDs. This shift from simple processing to active market participation can fundamentally change an individual’s financial trajectory. Utilizing professional fiat settlement ensures your trading capital is liquid and ready when high-impact market opportunities arise.

A Step-by-Step Protocol for Troubleshooting Failed Transactions

Resolving a failed transaction requires a systematic approach that moves from public ledger data to private integration logs. When troubleshooting crypto payments, your objective is to isolate the failure point before it impacts the customer experience or your daily reconciliation. Start by locating the Transaction ID (TXID). This alphanumeric string serves as the definitive proof of payment on the blockchain. By entering this ID into a network-specific explorer, you can determine if the funds are actually in transit or if the transaction never reached the network.

Step 2 involves confirming the number of network confirmations against your gateway’s required threshold. Most institutional gateways require multiple confirmations for Bitcoin or a single confirmation for high-speed networks like Tron to finalize a settlement. If a transaction shows zero confirmations after an extended period, it’s likely stuck in the mempool due to insufficient gas fees. At this stage, understanding the risks of using cryptocurrency, such as technical volatility and network congestion, helps you provide accurate status updates to your accounting department.

Verifying On-Chain Status (TXID Analysis)

Distinguishing between a “pending” and “dropped” transaction is vital for operational clarity. A pending transaction remains in the mempool waiting for a validator, while a dropped one has been purged by nodes and will never settle. Use multi-chain explorers to track these statuses across different protocols simultaneously. If a Bitcoin payment is delayed, you can suggest the customer utilize “Replace-By-Fee” (RBF) to increase the gas price and accelerate the broadcast. This proactive management ensures your liquidity remains accessible for future growth.

Debugging API and Gateway Integration Errors

If the blockchain confirms a successful transfer but your dashboard remains unchanged, the issue lies in your integration layer. Analyze your API response codes to identify common webhook failure scenarios, such as 404 or 500 errors. Ensure your Payment API is correctly configured to handle timeout signals and retry logic. Keeping your gateway firmware and software libraries updated is a simple yet effective way to prevent compatibility issues that lead to silent failures.

Once the transaction clears, the final step is to initiate a crypto offramp to mitigate any lingering market volatility. Securing your capital in this manner is essential for merchants who want to leverage their retail revenue for more sophisticated wealth generation. By converting settled funds into a dedicated Forex account, you can explore the transformative potential of gold (XAUUSD) or USD CFD trading. This shift from manual payment troubleshooting to active capital management can fundamentally change your financial trajectory, turning simple business revenue into a high-growth investment engine.

Beyond the Transaction: Leveraging Crypto for Forex and Gold CFD Trading

Mastering the technical nuances of troubleshooting crypto payments is a vital defensive strategy; however, it only marks the beginning of a merchant’s digital journey. Once your transaction flows are stabilized and your settlement protocols are efficient, you possess a powerful resource: liquid digital capital. In the professional landscape of 2026, forward-thinking individuals are shifting their focus from basic payment processing to the transformative potential of global market participation. By utilizing settled USDT, you can bypass the multi-day delays and high fees of traditional banking systems to enter the Forex and commodity markets instantly.

While the initial phase of troubleshooting crypto payments focuses on asset recovery, the secondary phase focuses on capital growth. Volatility is often viewed as a barrier to adoption by skeptics, but for a sophisticated trader, it represents a significant opportunity. CFD trading allows you to hedge against the very price swings that might otherwise impact your bottom line. By taking strategic positions in the market, you can protect your purchasing power while simultaneously building a secondary revenue stream that operates independently of your retail sales.

The Financial Impact of Gold and USD CFD Trading

Gold (XAUUSD) and USD CFDs have emerged as the preferred instruments for those seeking to diversify their holdings professionally. CFD trading allows you to speculate on price movements without the logistical burden of physical asset ownership. This flexibility is particularly valuable in the XAU/USD pair, where high liquidity ensures that large positions can be entered or exited with minimal slippage. This isn’t just about incremental gains. It’s about fundamentally changing your financial trajectory. When you leverage the volatility of the markets through strategic CFD positions, you turn a perceived risk into a structured opportunity for wealth generation.

Converting Payment Settlement into Strategic Capital

Integrating your crypto wallet with professional trading platforms creates a seamless bridge between your retail operations and the global markets. Using stablecoins as your base currency for Forex margin provides a competitive edge in speed and efficiency. Instead of waiting for bank wires to clear, your settled merchant revenue becomes strategic capital that can be deployed the moment a market signal appears. This professional evolution allows a business to move from passive merchant operations to active market participation, creating a resilient ecosystem where retail income and trading profits reinforce each other through institutional-grade tools.

Optimizing Settlement and Reducing Future Payment Failures

Reactive troubleshooting crypto payments is a necessary skill for asset recovery, but true operational excellence lies in preventing friction before it occurs. High-performance merchants in 2026 focus on optimizing the settlement layer to ensure that digital assets transition into usable capital without delay. By implementing fiat settlement, you bypass the traditional frictions associated with blockchain-to-bank transfers. This ensures that market volatility doesn’t erode your margins between the time of sale and the time of actual deposit, providing a stable foundation for your business’s liquidity.

Streamlining In-Store and Online Checkouts

Reducing customer-side errors is the most effective way to lower the volume of support tickets and failed transactions. Modern crypto POS machines significantly reduce manual entry errors by automating the address generation and network selection process for physical retail. For ecommerce environments, optimizing the checkout flow involves providing clear “Time-to-Pay” windows. These windows account for network variability, ensuring that a customer doesn’t send funds to an expired invoice, which is a primary cause of failed settlements and manual reconciliation efforts.

Advanced Settlement Strategies

Managing a high volume of transactions requires sophisticated automated reporting to keep your ledgers accurate. Setting up automated “Z-reports” for your crypto sales allows for seamless reconciliation between your digital ledger and traditional accounting software. These reports should handle edge cases like partial payments or overpayments automatically, either by issuing a programmatic refund or flagging the delta for review. As of June 2026, Travel Rule compliance is an essential component of every settlement workflow, requiring full sender and recipient details for every transfer to meet institutional standards and maintain regulatory standing.

Security remains the backbone of this professional ecosystem. Utilizing multi-signature security for merchant cold storage ensures that your accumulated assets are protected by multiple layers of authorization. This level of safety allows you to move confidently from simple payment acceptance to active wealth generation. Once your settlement is optimized, your business capital is ready to be deployed into high-growth markets. Trading Gold (XAUUSD) or USD CFDs becomes a logical extension of your financial strategy, offering the potential to transform your business’s financial life through professional market engagement and leverage.

To begin optimizing your merchant flow and securing your revenue, integrate our Payment API today for a seamless settlement experience.

Scaling with Confidence: The Pallapay Secure Infrastructure

Scaling a business in the digital asset space requires a partnership with a regulated financial institution that bridges the gap between disruptive tech and institutional reliability. Effective troubleshooting crypto payments at scale is only possible when your infrastructure is backed by global MSB registrations in the US and Canada. These registrations serve as a foundation of trust, ensuring that your capital is managed within a recognized legal framework. The Pallapay ecosystem serves as a definitive destination for these needs, offering everything from a high-volume OTC crypto exchange to integrated retail POS solutions.

Operational friction can occur at any time, but it shouldn’t stop your progress. Our 24/7 professional support provides a dedicated safety net, assisting with complex transaction friction that might otherwise stall your cash flow. This reliable foundation is what allows a merchant to move from simple payment processing to the transformative wealth generation found in gold (XAUUSD) and USD CFD trading. By removing the technical burden of ledger reconciliation, you gain the clarity needed to focus on market growth.

The Importance of Regulated Financial Partners

MSB registration is a non-negotiable standard for merchants handling significant volume in 2026. It guarantees that your financial partner operates under strict regulatory oversight, which is essential for maintaining institutional trust during settlement. We prioritize crypto security through advanced multi-signature protocols and institutional-grade encryption for all settled assets. Our global network of physical offices provides a level of reliability for OTC desk operations that digital-only entities simply cannot provide, ensuring your large-scale conversions are handled with absolute stability.

Unlocking Your Business Potential

The Pallapay ecosystem is designed to support your business at every stage of its evolution. By streamlining the mechanics of troubleshooting crypto payments, we empower you to focus on the strategic growth of your capital. Integrating our Payment API is the final step in unlocking your business’s full potential for global commerce. Once your payment flows are secure and automated, you have the operational freedom to explore the transformative potential of the Forex market. Trading Gold and USD CFDs can fundamentally change your financial life, turning a standard retail operation into a sophisticated engine for capital growth and long-term wealth.

Securing Your Financial Evolution in 2026

Mastering the technical protocols for troubleshooting crypto payments transforms an operational hurdle into a decisive strategic advantage. You’ve learned how to isolate network friction and implement institutional settlement layers that protect your business margins from volatility. This transition isn’t just about operational efficiency; it’s about the freedom to deploy your capital into high-growth markets like Gold (XAUUSD) and USD CFDs. When your payment infrastructure is stable, your focus shifts toward the transformative potential of active market participation.

Pallapay provides the institutional foundation for this growth, featuring official MSB registration in the US and Canada alongside a global presence in 180+ countries. Our comprehensive ecosystem includes physical OTC desks and retail POS hardware, ensuring your digital assets are always liquid and accessible. Integrate the Pallapay Payment API to secure your business today and unlock a new trajectory for your financial life. The bridge between traditional reliability and digital innovation is ready for your business to cross. You’re now equipped to turn every transaction into a stepping stone for global wealth generation.

Frequently Asked Questions

Why is my crypto payment still pending after an hour?

A pending status usually indicates that the transaction hasn’t been picked up by a validator due to a low gas fee or high network congestion. When troubleshooting crypto payments, you should check the mempool status via a blockchain explorer. If the fee was set below the current market rate, the transaction remains in a waiting state until demand decreases or the sender utilizes a fee-boosting tool.

What happens if a customer sends the wrong amount of cryptocurrency?

Most payment gateways will flag the transaction as “Partially Paid” or “Overpaid” without automatically finalizing the order. For underpayments, the system typically waits for the remaining balance to be sent to the same address before releasing the goods. In the case of overpayments, the merchant must either manually reconcile the excess or utilize an automated system to refund the delta to the customer’s wallet.

How do I troubleshoot a failed API call in my crypto gateway?

Start by reviewing the HTTP response codes in your integration logs to identify the specific failure point. A 401 error suggests an issue with your API keys, while 422 or 400 errors often point to malformed request bodies or invalid wallet addresses. Ensuring your webhook endpoints are publicly accessible and capable of returning a 200 OK status is essential for maintaining a stable communication flow.

Can I recover cryptocurrency sent to the wrong network protocol?

Recovery is often impossible because blockchain transactions are irreversible and cross-chain compatibility is limited. If a customer sends TRC-20 USDT to an ERC-20 address, the assets are generally lost unless the receiving wallet provider has specific recovery tools. This highlights the importance of using a gateway that enforces network-specific address validation during the checkout process to prevent these high-risk errors entirely.

How does network congestion affect my business settlement times?

High congestion increases the time required to reach the necessary confirmation threshold for a final settlement. When the network is saturated, validators prioritize transactions with higher fees, leaving lower-fee business transfers in the mempool for longer periods. This delay can impact your liquidity, making it vital to use a provider that offers instant fiat conversion to shield your revenue from price fluctuations during the wait.

Is it possible to automate the resolution of stuck crypto payments?

Yes, automation is possible through features like Replace-By-Fee (RBF) or Child-Pays-For-Parent (CPFP) protocols. Advanced gateways can be configured to automatically detect stuck transactions and suggest a fee bump to accelerate the broadcast. This proactive approach to troubleshooting crypto payments reduces manual intervention and ensures that your ecommerce operations maintain a consistent settlement rhythm without requiring constant technical oversight.

What is the role of a TXID in troubleshooting merchant payments?

The Transaction ID (TXID) is the unique alphanumeric hash that serves as the definitive proof of a transfer on the public ledger. It allows you to track the exact status, timestamp, and network fees of any payment independently of your internal dashboard. For merchants, the TXID is the primary tool for reconciling blockchain data with fiat ledgers and resolving customer disputes regarding payment delivery.

How can I use my settled crypto funds for Gold or Forex trading?

Once your merchant revenue is settled into a secure wallet, you can transfer those funds directly to a professional Forex account. This allows you to leverage your capital by trading Gold (XAUUSD) or USD CFDs on global markets. Moving from simple payment processing to active trading can fundamentally change your financial life, turning standard business profits into a diversified engine for wealth generation through strategic market engagement.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.