The era of anonymous trading has ended, but for the professional investor, this transition represents the greatest expansion of opportunity in a decade. You might feel that providing personal documentation is a hurdle to your privacy, yet the reality of kyc in crypto in 2026 is that it serves as your digital passport to institutional-grade liquidity. It’s understandable to feel hesitant about sharing data when the lines between security and friction seem blurred. However, moving beyond the unregulated phase of digital assets is exactly what allows serious traders to bridge the gap between volatile tokens and stable, high-leverage markets like XAU/USD.

This article demonstrates how KYC compliance serves as the essential foundation for secure, high-stakes trading in gold and currency markets. You’ll discover how a verified identity unlocks professional tools for gold and forex CFD trading, ensuring your capital remains protected by a regulated entity. We’ll clarify the distinction between KYC and AML, explore the mechanics of high-leverage USD pairs, and show you how this professional gateway can fundamentally transform your financial trajectory. By adopting these standards, you gain the stability and speed required to excel in the modern global economy.

Key Takeaways

- Learn how kyc in crypto serves as the definitive digital handshake required to access institutional liquidity and regulated financial networks in 2026.

- Discover the secure, multi-step verification process that utilizes AI-driven biometrics to protect your personal data and trading capital from unauthorized access.

- Understand why regulatory compliance is the essential foundation for legal capital protection and seamless, professional fiat-to-crypto conversions.

- Unlock the transformative potential of high-leverage gold (XAU/USD) and forex CFD markets by bridging the gap between digital assets and traditional commodities.

- Explore how integrating with a professional ecosystem facilitates rapid, compliant entry into global currency trading environments for serious investors.

Defining KYC in the 2026 Crypto Landscape

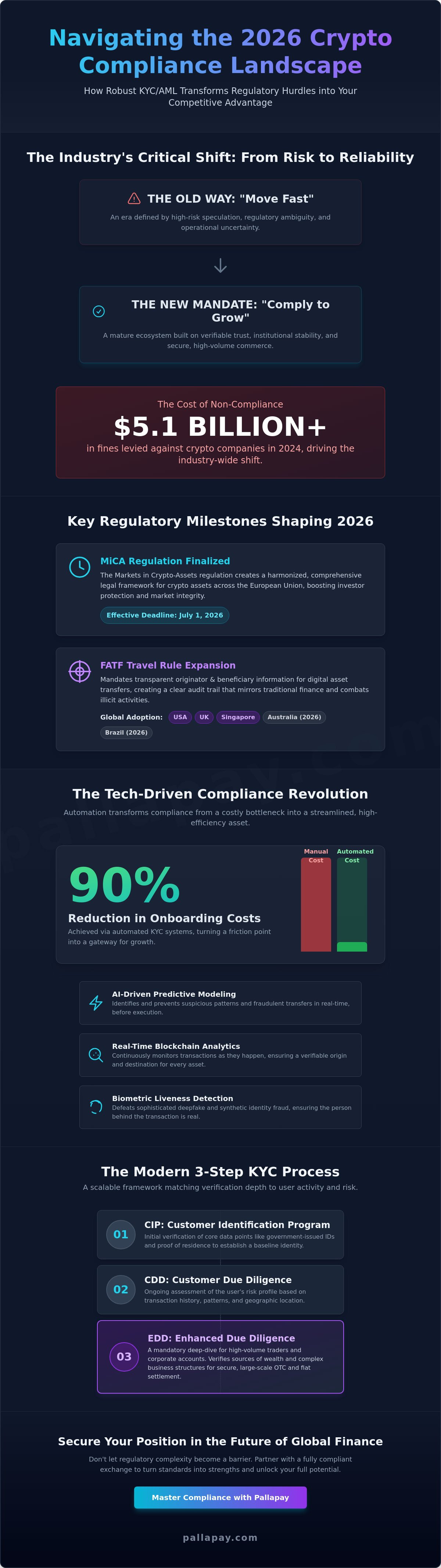

Identity verification is no longer an optional feature of the digital economy; it’s the infrastructure that makes high-stakes trading possible. By Defining KYC as a mandatory process of identifying and verifying a user’s identity, we establish the ground rules for institutional interaction. In 2026, kyc in crypto serves as the digital handshake between technological innovators and the world’s most regulated financial systems. It’s the mechanism that transforms a volatile digital asset into a tool for serious wealth generation. KYC is the foundational trust protocol for modern digital finance. Without this initial layer of verification, the path to trading precious metals or global currencies remains fragmented and insecure.

The Evolution of Virtual Asset Service Providers (VASPs)

The landscape for Virtual Asset Service Providers (VASPs) has matured significantly following the full implementation of the EU’s Markets in Crypto-Assets (MiCA) regulation on July 1, 2026. This shift was largely driven by the Financial Action Task Force (FATF) and its updated standards for global compliance. Professional traders now prioritize platforms with official Money Services Business (MSB) registrations in jurisdictions like the US and Canada. These regulated entities offer a higher tier of user protection, ensuring that your capital is handled with the same rigor as a traditional brokerage. While non-custodial services offer autonomy, custodial platforms with robust KYC protocols provide the necessary framework for high-volume fiat-to-crypto operations. Using a secure Pallapay Wallet allows you to manage these verified credentials while maintaining instant access to trading liquidity.

KYC vs. AML: Understanding the Synergy

Many traders conflate identity verification with crime prevention, yet understanding the synergy between KYC and AML is vital for long-term success. KYC focuses on the initial verification of who you are, while Anti-Money Laundering (AML) involves the continuous monitoring of transactions to detect suspicious activity. KYC is the prerequisite for effective AML monitoring. Without a verified identity, it’s impossible to maintain the integrity of the crypto-forex bridge. This dual-layered security prevents market manipulation and protects your individual account from unauthorized access. When you trade gold or forex CFDs, this compliance ensures that your profits are legitimate and your withdrawals are never delayed by regulatory red flags. It’s the difference between operating in a shadow market and participating in the global financial elite. By verifying your identity, you aren’t just following a rule; you’re securing your seat at the professional trading table.

The Multi-Step Process of Crypto Identity Verification

Verification is a sequence of precision. To access the high-liquidity markets of gold and forex, a trader must pass through a structured identification protocol designed to eliminate fraud. The architecture of kyc in crypto has transitioned from manual, document-heavy reviews into an automated, four-stage sequence that prioritizes both security and speed. This evolution ensures that professional traders can move from registration to execution without the delays associated with legacy banking.

- Submission of PII: Personally Identifiable Information is submitted through secure, end-to-end encrypted channels. This protects sensitive data from intercept risks during the initial transmission phase.

- Biometric Authentication: Sophisticated AI-driven facial recognition systems conduct liveness checks. This step confirms the user is a living person rather than a high-resolution image or a deepfake.

- Global Screening: Automated systems cross-reference data against international Politically Exposed Persons (PEP) and Sanctions lists. This happens in real-time to maintain compliance with global financial standards.

- Risk Assessment: The final stage evaluates financial history and intended trading volume. This allows the platform to assign appropriate leverage and account limits tailored to the user’s professional profile.

Modern Documentation Standards

In 2026, the standard for identity has shifted toward Digital Identity Wallets and Decentralized Identity (DID). These technologies allow for reusable verification, reducing the need for repetitive document uploads. Accepted forms of ID now include biometric passports and national IDs with embedded NFC chips. Even in a borderless digital economy, proof of residence remains essential. It is typically verified through digital utility records or direct bank API integrations to ensure the highest level of accuracy.

AI and Biometrics: Frictionless Onboarding

Speed is the primary competitive edge in modern finance. AI-driven verification reduces onboarding time from several days to mere seconds. This efficiency doesn’t compromise security; liveness detection serves as a critical defense against evolving deepfake fraud. This streamlined kyc in crypto experience allows for immediate market entry without sacrificing institutional-grade safety. For those ready to transition into high-stakes trading, utilizing a professional crypto off-ramp provides the necessary speed to capitalize on gold and currency price shifts.

Why KYC is Non-Negotiable for Secure Financial Transformation

Security isn’t just a feature; it’s the foundation of every successful trade. kyc in crypto acts as a personal shield, ensuring that only you can access and manage your trading capital. By establishing a verified identity, you eliminate the risk of account takeovers that plague unregulated platforms. This process creates a transparent audit trail, which is essential for traders who intend to move significant sums between digital assets and traditional commodity markets. It’s the difference between gambling in an opaque environment and investing within a professional framework.

Regulated environments provide the legal framework required for high-stakes financial operations. When you move large volumes between digital assets and traditional markets, you need the assurance that your fiat-to-crypto conversions are legally protected. Adopting kyc in crypto transforms your profile from a retail participant into a credible counterparty capable of engaging with institutional-grade liquidity. This verification allows large-scale investors to execute trades in gold and forex markets without the slippage or counterparty failures common in anonymous exchanges. Compliance is the price of entry for those seeking the stability of the global financial elite.

Mitigating Counterparty Risk

Trading on anonymous platforms significantly increases the risk of frozen assets or sudden liquidity drains. Choosing an MSB-regulated partner ensures your funds are handled by an entity registered in the USA and Canada, providing a level of oversight that protects your interests. This professional accountability is absent in the unregulated sectors of the industry. For a deeper understanding of how these protections function, consult our guide on Crypto Security in 2026. By mitigating these risks early, you ensure your capital remains mobile and ready for market opportunities.

Enabling Fiat Settlements and Card Issuance

The true value of a successful trading strategy is the ability to utilize profits in the physical world. Robust identity verification is the specific requirement for accessing high-utility tools like the Pallapay Mastercard. This integration allows you to spend your gold and forex gains directly at millions of merchants globally, turning digital success into tangible lifestyle improvements. By utilizing professional fiat settlement services, you bridge the gap between digital valuation and physical wealth. A compliant trading strategy relies on efficient crypto off-ramps to move capital between markets and personal bank accounts with absolute transparency and speed.

From Verification to Valuation: Accessing Gold and Forex CFDs

The bridge from identity verification to market valuation is where the professional trader finds a distinct competitive edge. While retail participants often struggle with limited asset classes, kyc in crypto provides the necessary credentials to enter the high-stakes world of Contracts for Difference (CFDs). This transition allows you to leverage your digital holdings as collateral for sophisticated positions in global commodities and currency pairs. It’s the ultimate evolution of the digital asset ecosystem; moving beyond simple holding to active, strategic wealth generation within a regulated framework.

Trading Gold (XAU/USD) in the Digital Age

Gold remains the definitive store of value, yet the logistics of physical ownership often hinder rapid market response. By utilizing crypto-funded CFD accounts, you combine the historic stability of gold with the near-instant settlement speeds of the blockchain. This model allows you to profit from XAU/USD price movements without the complexities of physical storage, security, or insurance. XAU/USD CFDs offer a sophisticated hedge against fiat inflation, providing a secure sanctuary during periods of global economic volatility. This synergy ensures that your portfolio remains resilient while maintaining the liquidity needed for rapid capital reallocation as market conditions shift.

Forex Trading: A Life-Changing Financial Skill

The foreign exchange market is the largest and most liquid financial arena in the world, processing trillions of dollars in daily volume. Mastering the forex market can lead to true financial independence by providing consistent opportunities for growth across USD and other major currency pairs. The synergy between crypto volatility and forex market depth creates a unique environment for the professional trader. While crypto markets provide explosive potential, the forex market offers the structural depth required for large-scale, high-leverage operations. Utilizing kyc in crypto as your entry point ensures that your entry into these markets is backed by institutional-grade security and legal protection.

Accessing these professional tools requires a partner that understands the intersection of digital innovation and traditional finance. Verification isn’t just about compliance; it’s about unlocking the ability to trade with the leverage and liquidity that only a regulated entity can provide. Start your journey toward financial independence by exploring our crypto off-ramp solutions to manage your trading profits with absolute ease and transparency.

Navigating the Pallapay Ecosystem with Absolute Compliance

The journey from a digital asset holder to a professional trader concludes within a comprehensive ecosystem designed for institutional reliability. Pallapay provides the definitive bridge between the innovation of digital assets and the stability of established financial markets. By integrating kyc in crypto directly into the user experience, the platform ensures that every transaction is backed by the highest standards of regulatory oversight. This isn’t merely a compliance layer; it’s a strategic advantage that allows for the seamless movement of capital across 180+ countries. Every feature is built to accelerate your progress while maintaining absolute security.

The Pallapay Wallet serves as the central hub for this financial transformation. It manages your verified credentials while providing instant access to the liquidity needed for high-stakes forex and gold trading. For those managing significant capital, the OTC Crypto Exchange offers the depth required for large-scale gold CFD positions without the slippage often found on retail exchanges. Businesses can further accelerate their operations by utilizing the Payment API, which automates compliant settlements and ensures that every transfer meets the rigorous standards of the 2026 regulatory landscape.

Institutional Reliability for Individual Traders

Professionalism is defined by accountability. Pallapay’s status as a registered Money Services Business (MSB) in both the United States and Canada provides the essential security foundation for your trading journey. This registration ensures that your capital is handled with the same institutional rigor as a traditional financial institution, yet with the speed of a modern fintech partner. Having a global partner with physical offices in major financial hubs provides a level of stability that anonymous platforms simply cannot replicate. You can start your financial transformation today by establishing a verified account that prioritizes your protection and growth.

The Future of Compliant Trading

The landscape of 2026 is defined by the mass adoption of digital assets through compliant platforms. As global regulations reach full implementation, the distinction between digital assets and traditional finance will continue to dissolve. Pallapay remains at the forefront of this evolution, developing upcoming features that will further simplify the transition between digital collateral and traditional commodity markets. The role of kyc in crypto is to empower the user by providing a single, verified gateway to the world’s most lucrative opportunities. Verify once, trade everything, and secure your financial future within an ecosystem built for the professional era.

Empowering Your Professional Trading Future

The transition to a regulated financial ecosystem is a strategic advancement rather than a barrier. By embracing the standards of kyc in crypto, you secure a digital credential that unlocks the world’s most liquid markets. This verification process bridges the gap between digital assets and the high-stakes reality of gold and forex CFD trading. You gain the ability to leverage your portfolio with institutional-grade security while ensuring your capital is protected by a regulated MSB in the USA and Canada.

Institutional-grade liquidity in XAU/USD and major currency pairs is only accessible through a compliant gateway. This structural depth allows you to transform digital holdings into tangible financial independence with the support of instant crypto off-ramp services. Your path to a sophisticated trading career is now clear and technologically supported.

Start Your Financial Transformation: Open a Verified Pallapay Account Today

Take the final step toward global commodity markets and begin your journey into professional finance with absolute confidence.

Frequently Asked Questions

What is the primary purpose of KYC in the crypto industry?

The primary purpose of kyc in crypto is to establish a verified link between a digital identity and a real-world individual. This process ensures that financial platforms remain compliant with global anti-money laundering standards and prevents unauthorized actors from accessing sensitive trading environments. By verifying users, platforms can offer higher limits and professional-grade tools like gold CFDs while maintaining institutional security for all participants.

Can I trade gold and forex CFDs without completing KYC?

Accessing professional gold and forex CFD markets without identity verification is virtually impossible in 2026. Regulated entities, including MSBs and licensed brokers, are legally mandated to verify every user before granting access to high-leverage trading tools. This requirement protects the integrity of the market and ensures that your capital is handled within a lawful, secure framework that permits the legal conversion of digital assets to fiat.

How long does the KYC verification process usually take on Pallapay?

Verification on Pallapay typically occurs within seconds or minutes thanks to advanced AI-driven biometric systems. While manual reviews were common in the past, modern liveness detection and automated database cross-referencing have streamlined the onboarding experience. This efficiency allows you to transition from registration to active gold and forex trading almost instantly, ensuring you don’t miss volatile market opportunities due to administrative delays.

What documents are required to pass KYC for high-volume trading?

High-volume trading requires a valid government-issued passport or national ID card with biometric features. You’ll also need to provide proof of residence, such as a recent utility bill or bank statement, to confirm your jurisdiction. For institutional-grade limits, platforms may request a declaration of the source of funds to ensure compliance with the latest FATF standards and MiCA regulations implemented in 2026.

Is my personal data safe when I submit it for crypto KYC?

Your personal data is protected by end-to-end encryption and strict data privacy protocols mandated by MSB registrations in the US and Canada. Regulated platforms utilize secure, siloed storage systems that prevent unauthorized access to your personally identifiable information. This level of oversight ensures that your data is only used for compliance purposes and is handled with the same security rigor as a traditional global bank.

Why do regulators require KYC for gold and currency trading?

Regulators require kyc in crypto and commodity markets to mitigate systemic risks such as money laundering and market manipulation. By identifying every participant, authorities can maintain the stability of the global financial system and ensure that high-leverage trading isn’t used for illicit activities. This transparency is what allows platforms to provide the deep liquidity necessary for professional-grade XAU/USD and forex CFD operations.

Can KYC help me recover my account if I lose access?

Identity verification is the most reliable method for recovering a lost or compromised account. If you lose your credentials, your pre-verified biometric data and government ID serve as the definitive proof of ownership. This security layer prevents malicious actors from hijacking your funds and ensures that the platform can safely restore your access to gold and forex trading tools without compromising your capital.

Does KYC impact the speed of my crypto-to-fiat withdrawals?

Completed verification actually accelerates your crypto-to-fiat withdrawals by removing the need for additional security checks during the off-ramp process. Verified accounts benefit from automated settlement flows and higher daily limits, allowing for the near-instant transfer of trading profits to your bank account or Mastercard. Without KYC, withdrawals are often subject to lengthy manual holds or strict transaction caps that hinder financial mobility.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.