Your e-commerce store is no longer just a digital storefront; it’s a strategic liquidity engine that can fuel your entry into global financial markets. By integrating a professional crypto payment gateway for e-commerce, you aren’t just accepting digital assets; you’re bypassing the high transaction fees and slow settlement cycles of traditional banking rails. This shift allows you to move from passive merchant to active participant in the global economy.

You likely recognize that waiting days for international funds to clear is an unnecessary drag on your capital, especially when market opportunities in Gold (XAU/USD) and Forex CFDs require immediate action. We’ll show you how to transform your daily sales into a high-yield advantage by utilizing instant fiat settlements and seamless off-ramping. This isn’t about chasing trends; it’s about establishing a professional bridge between your commercial operations and institutional-grade wealth building.

This guide outlines the 2026 regulatory landscape, including the impact of the GENIUS Act, and explains how to bridge the gap between retail profits and the transformative potential of CFD trading. You’ll discover how a unified ecosystem provides the stability you need to scale your business while moving profits into the world’s most liquid currency and commodity markets.

Key Takeaways

- Establish a high-liquidity engine for your business by integrating a crypto payment gateway for e-commerce that provides instant fiat settlement and eliminates traditional banking delays.

- Identify the critical security standards and compliance requirements, such as MSB registration in the US and Canada, that ensure institutional-grade reliability for your digital transactions.

- Streamline your capital flow using professional off-ramp solutions to move profits from your online store directly into your bank account or trading wallet without friction.

- Leverage your commercial revenue to access the transformative potential of Forex and Gold (XAU/USD) CFD trading for strategic wealth diversification and growth.

- Simplify your financial operations by adopting a comprehensive ecosystem that bridges the gap between retail sales and high-yield global investment markets.

What is a Crypto Payment Gateway for E-commerce?

A crypto payment gateway for e-commerce acts as the critical software layer that authorizes and processes digital asset transactions between a customer and a merchant. In 2026, this technology has evolved from a niche experimental tool into essential financial infrastructure for businesses seeking global liquidity. Before diving into the mechanics, it’s helpful to understand the foundational technology by exploring What is Cryptocurrency? and how its decentralized nature facilitates trustless value transfer.

For online merchants, the primary hurdle has always been price stability. Modern gateways solve this by providing instant conversion into stablecoins like USDT or direct fiat settlement. This ensures that a sale made in Bitcoin or Ethereum doesn’t lose value before it hits your balance sheet. By locking in the value at the moment of the transaction, you maintain consistent cash flow while building the capital necessary for high-impact investments like Forex and Gold CFD trading.

How Modern Gateways Work in 2026

The modern checkout experience is designed for speed and security. When a customer selects crypto at checkout, the gateway generates a unique payment address and monitors the blockchain for the transaction. Security protocols have reached institutional standards through Multi-Party Computation (MPC) nodes and multi-sig custody. These systems ensure that private keys are never stored in a single vulnerable location. Once the transaction is detected, the gateway performs a real-time conversion. This instant liquidity is non-negotiable for merchants who intend to pivot their retail profits into the XAU/USD or Forex markets, where timing is the difference between stagnation and financial transformation.

Why E-commerce is Moving Toward Crypto-Native Rails

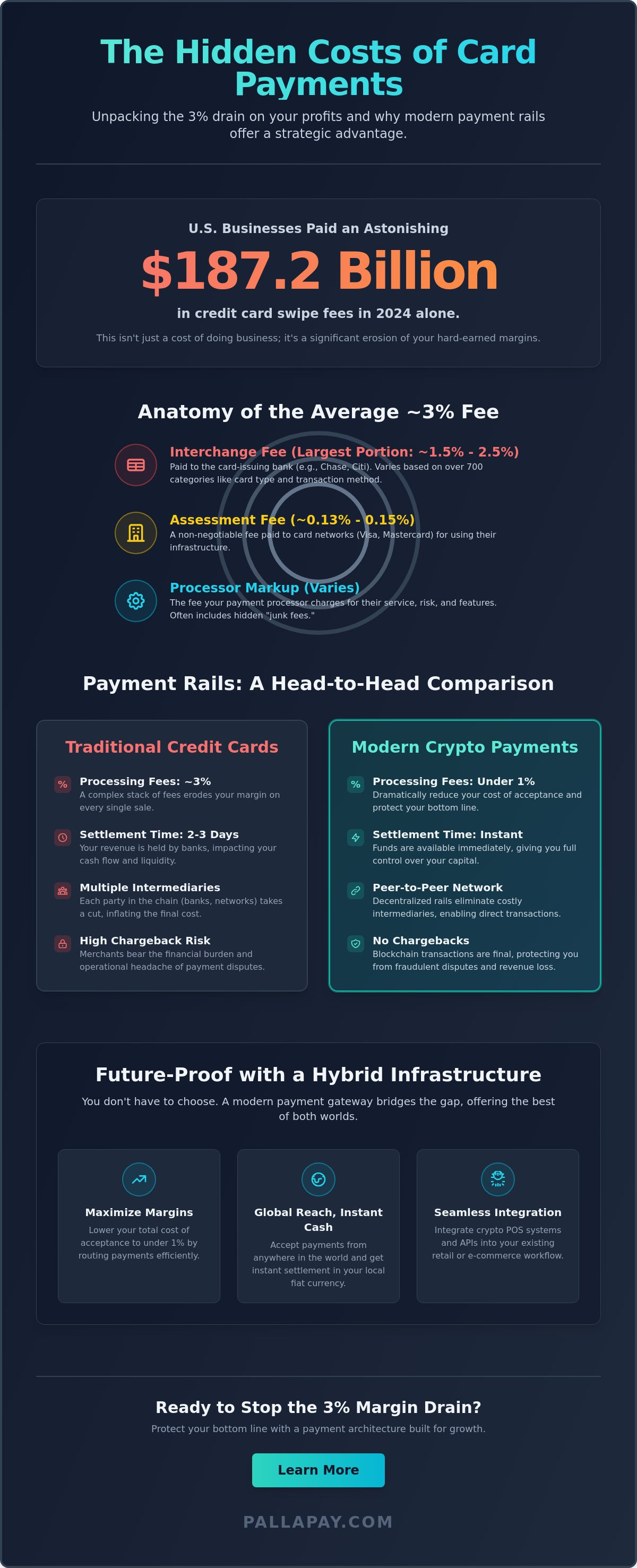

Traditional credit card networks often feel like a relic of a slower era. By switching to a crypto payment gateway for e-commerce, businesses can reduce transaction costs by up to 80% compared to legacy processors. These savings directly improve your bottom line, providing more capital to fuel your trading strategies.

- Eliminating Chargeback Fraud: Crypto transactions are final and immutable, removing the risk of “friendly fraud” that plagues global retail.

- Global Accessibility: Merchants can accept orders from any corner of the globe without the limitations of traditional banking borders.

- Faster Capital Rotation: Instant settlements allow you to move funds from sales to market investments in minutes rather than days.

This borderless efficiency is what allows a modern e-shop to function as a high-performance wealth engine. By removing the friction of traditional rails, you’re free to focus on the transformative potential of the markets. Integrating these solutions through dedicated e-commerce tools ensures your business remains competitive in an increasingly digital economy.

Evaluating the Best Crypto Payment Providers for Your Business

Selecting the right crypto payment gateway for e-commerce requires a strategic shift in perspective. You aren’t just choosing a vendor; you’re selecting a partner that dictates how quickly your retail revenue can be deployed into high-yield markets. In 2026, the baseline for any professional provider is a combination of regulatory compliance and technological agility. Security starts with Money Services Business (MSB) registration. This isn’t a luxury; it’s a fundamental requirement that ensures your provider operates under strict federal oversight. When a gateway is registered in major jurisdictions like the US and Canada, it signals a commitment to institutional-grade safety. This protection is vital when you’re managing large volumes of capital intended for XAU/USD or Forex CFD positions.

Settlement speed is the next critical factor. Many legacy providers still operate on “next-day” settlement cycles, which can leave your capital exposed to market shifts or missed entries. Leading gateways now offer instant liquidity. This means your e-commerce sales are converted and available for use immediately, allowing you to react to gold price movements or currency fluctuations in real time. Supported assets also play a pivotal role. While Bitcoin and Ethereum remain staples, the efficiency of stablecoins like USDT cannot be overstated. A provider that balances these popular assets with stablecoin-native rails ensures your cash flow remains predictable even during periods of high market volatility.

Integration options should accommodate your specific business scale. Whether you require ready-made plugins for popular platforms or a custom-built solution, the transition should be frictionless. A sophisticated gateway eliminates the technical hurdles of the digital economy, letting you focus on the growth of your trading portfolio.

The Importance of API for Crypto Payments

A robust API for Crypto Payments is the backbone of a sophisticated financial strategy. It allows you to move beyond basic checkout buttons and integrate payment flows directly into your business logic. By automating the transition from sale to settlement, you ensure that your capital is always positioned for the next trading opportunity. This technical flexibility maintains your brand’s professional appearance while handling the complex background processes of asset conversion without manual intervention. It’s the difference between a static storefront and a dynamic liquidity engine.

Compliance and Institutional Trust

In the 2026 global landscape, navigating the complexities of KYC and AML is essential for long-term stability. Regulated gateways protect you from the legal and financial risks associated with unverified transactions. Pallapay maintains active MSB registrations in the US and Canada, providing a secure foundation for merchants who prioritize reliability. This institutional trust allows you to focus on the transformative potential of your trading account, knowing your underlying payment infrastructure meets the highest global standards. If you’re ready to secure your business’s financial future, exploring a regulated settlement solution is the next logical step.

Fiat Settlement and the Power of the Crypto Off-Ramp

Liquidity is the oxygen of a growing enterprise. While accepting digital assets opens your business to a global market, the ability to convert those assets into spendable cash is what sustains your operations and fuels your investment strategies. A professional crypto payment gateway for e-commerce serves as the primary engine for this conversion, turning volatile digital revenue into stable fiat currency. This process, known as fiat settlement, ensures that your hard-earned profits aren’t subject to the unpredictable swings of the crypto market. By locking in value at the point of sale, you create a predictable cash flow that can be immediately deployed where it matters most.

The true strategic advantage lies in the off-ramp. An off-ramp is the technological bridge that moves your digital assets back into the traditional banking system or into liquid cash. For the modern entrepreneur, this isn’t just a technical feature; it’s a wealth-building tool. Moving profits through a dedicated crypto off-ramp allows you to bypass the delays of legacy financial institutions. This speed is essential when you intend to transition e-commerce revenue into the high-stakes world of XAU/USD and Forex CFD trading. In these markets, having capital ready to deploy can be the difference between a missed opportunity and a life-changing financial move.

Instant Fiat Settlement for E-commerce

Traditional cross-border transfers are often slow and expensive, sometimes taking days to clear. By utilizing Fiat Settlement, you eliminate the “waiting game” entirely. This real-time liquidity enables precise inventory management, allowing you to restock products based on actual sales data rather than projections. Furthermore, managing multi-currency accounts becomes effortless. You can accept payments in various digital assets while settling in the fiat currency that best supports your global e-commerce operations. This efficiency keeps your business lean and your capital mobile, ready for the next market shift.

Bridging the Gap with Physical Off-Ramps

High-volume merchants require more than just digital transfers; they need tangible access to their capital. Physical OTC desks provide a secure environment for extracting large-scale profits with professional oversight. This is complemented by the Pallapay Mastercard, which allows you to spend your e-commerce profits in the real world just as easily as traditional currency. Whether you’re reinvesting in your shop or funding a new position in Gold and USD CFDs, these tools turn digital sales into tangible capital. This seamless transition from retail profit to market-ready liquidity is the cornerstone of a sophisticated financial life, allowing you to grow your wealth across multiple sectors simultaneously.

Transformative Potential: From E-commerce Profits to Gold and Forex Trading

The 2026 wealth cycle represents a fundamental shift in how digital entrepreneurs manage their capital. By utilizing a crypto payment gateway for e-commerce, you create a direct pipeline from retail transactions to global investment opportunities. This is not merely about processing payments; it’s about capturing liquidity in real-time to fund high-performance market positions. When your store generates revenue, that capital is instantly available to serve as margin for CFD trading. This allows you to move beyond the linear growth of retail sales and enter the world of institutional-grade wealth management.

Gold and USD CFDs have emerged as the preferred hedges for digital entrepreneurs seeking to protect their purchasing power. While your e-commerce business provides the base income, the markets provide the scale. The transition from a store owner to a global investor is a psychological shift that defines the modern financial elite. You’ll stop viewing sales as stagnant bank balances and start seeing them as active units of leverage. By locking in your retail profits through instant settlement, you ensure that your trading margin is always ready for the next market move.

Mastering Gold and USD CFD Trading

Contracts for Difference (CFDs) allow you to capitalize on price movements in the XAU/USD and Forex markets without the requirement of owning the underlying asset. This flexibility is crucial for maintaining a lean business model. Gold remains the ultimate safe haven, providing a stable counterpoint to the volatility of the digital economy. Simultaneously, USD CFDs enable you to profit from global currency fluctuations, turning macroeconomic shifts into business advantages. By using the instant liquidity provided by your gateway, you can enter these positions at the precise moment the market presents an opportunity.

Changing Your Financial Life Through Strategic Reinvestment

Compounded trading gains offer a path to financial independence that linear retail income cannot match. A crypto-native business model accelerates this process by removing the friction points between earning and investing. Consider a scenario where a merchant utilizes a holiday sales peak to fund a high-volume Forex position. Instead of waiting for traditional bank clearances, the merchant uses settled USDT to enter a Gold CFD trade during a period of market volatility. This move can turn a standard retail profit into a significant capital gain in a fraction of the time. If you’re ready to bridge the gap between your store and the global markets, leverage professional liquidity tools to start your journey.

Implementing the Pallapay Ecosystem for Your E-shop

Adopting a professional crypto payment gateway for e-commerce is the final step in your transition from a traditional merchant to a high-liquidity global investor. The Pallapay ecosystem provides this transition without friction; it connects your digital sales directly to your strategic wealth goals. Whether you operate high-volume E-commerce platforms or traditional Retail Stores, the infrastructure remains consistent, secure, and highly efficient. This integrated approach ensures that every transaction serves as a building block for your broader financial portfolio.

Omnichannel dominance is now a baseline requirement for success. By combining your online gateway with Crypto POS Machines, you capture value across every touchpoint of your business. If your business struggles with fragmented revenue streams, the Pallapay Merchant Dashboard provides the unified oversight you need. All revenue streams converge in one place, providing real-time tracking of your liquidity. This clarity is essential. It allows you to see exactly how much capital is ready to be pivoted into Gold or Forex markets at any given second, ensuring you never miss a market entry due to administrative delays.

Integrating the Payment API

A developer-friendly Payment API is the engine behind your global expansion. It enables you to customize the checkout experience, ensuring that your customers feel the same trust they’d with a traditional bank while enjoying the speed of crypto-native rails. Automation is the key to scaling your wealth. You can set specific rules to move a percentage of every sale directly into your settlement account. If manual fund transfers slow your investment timing, this automated flow provides the instant liquidity required to maintain your margin in high-stakes CFD trading environments.

The Future of Your Business with Pallapay

Managing business expenses shouldn’t require exiting your digital ecosystem. The Pallapay Mastercard allows you to spend settled profits directly, bridging the gap between your digital success and real-world operations. This utility, backed by the security of a regulated partner with MSB registrations in the US and Canada, provides the peace of mind necessary for aggressive market participation. You’re no longer just running a shop; you’re managing a sophisticated wealth engine. By adopting these tools, you’re positioning yourself at the forefront of the 2026 financial evolution, where the transformative potential of Gold and Forex CFDs is finally within reach.

Unlocking Your Global Wealth Engine

The evolution of global commerce in 2026 demands more than just a place to store digital assets; it requires a high-velocity bridge between your daily sales and the world’s most liquid markets. By implementing a professional crypto payment gateway for e-commerce, you’ve secured the ability to bypass traditional banking delays and high fees. This infrastructure isn’t just a checkout tool. It’s the foundation for a transformative financial life where retail profits fund strategic positions in Gold and USD CFD markets.

Success in this landscape depends on institutional-grade reliability and speed. As an MSB registered entity in both the USA and Canada, Pallapay ensures your capital remains secure while providing the instant fiat settlement necessary for real-time market entries. You’ve learned how to turn your e-shop into a wealth engine that supports diverse trading strategies through a comprehensive ecosystem. Now is the time to transition from a merchant to a global investor.

Scale your e-commerce business and start trading with Pallapay today.

The path to financial independence is built on the efficiency of your tools and the clarity of your vision. Take the first step toward mastering the markets and securing your professional legacy with a partner that understands the speed of modern wealth.

Frequently Asked Questions

What is a crypto payment gateway and how does it work for e-commerce?

A crypto payment gateway for e-commerce is a sophisticated software layer that authorizes and processes digital asset transactions for online merchants. When a customer chooses to pay with cryptocurrency, the gateway generates a unique payment address and monitors the blockchain for confirmation. Once the transaction is verified, the system automatically converts the digital assets into your preferred fiat currency or stablecoin, providing a standardized checkout experience similar to traditional credit card processors.

How fast can I convert my crypto sales into fiat for trading?

Conversion occurs instantly at the moment of the transaction through our automated settlement engine. This real-time liquidity is designed specifically for merchants who need to capitalize on market volatility without waiting for legacy banking cycles. Once the blockchain confirms the payment, the funds are settled in fiat, allowing you to move capital into your trading account to fund Gold or Forex positions immediately.

Are crypto payments safe for my e-commerce customers in 2026?

Crypto payments are exceptionally secure in 2026 due to the implementation of Multi-Party Computation (MPC) nodes and multi-signature custody protocols. These institutional-grade standards ensure that private keys are never stored in a single vulnerable location, protecting customer funds from unauthorized access. The immutable nature of the blockchain also eliminates chargeback fraud, which provides a more secure and predictable environment for merchants than traditional card networks.

What are the fees associated with using a crypto payment gateway vs. credit cards?

Crypto gateways typically offer a more cost-effective alternative to traditional credit card processors. While standard card networks often charge up to 2.9% plus additional fixed costs per transaction, crypto-native rails can reduce these overhead expenses significantly. These savings directly increase your bottom line, providing more capital to serve as margin for your XAU/USD or currency trading strategies.

Can I use my e-commerce profits to trade Gold and Forex CFDs immediately?

You can deploy your retail profits into CFD markets as soon as the fiat settlement is finalized in your dashboard. The integration between our payment infrastructure and trading accounts is engineered for maximum speed to support a high-performance wealth cycle. This allows you to capture price movements in Gold or major currency pairs immediately after a successful sale, turning your store’s daily revenue into active trading capital.

Do I need a special bank account to accept crypto payments through Pallapay?

No special bank account is required to begin accepting digital assets. You can receive settlements directly into your existing corporate bank account or utilize our integrated ecosystem for even faster access. For merchants seeking maximum flexibility, profits can be off-ramped to a Mastercard or managed within a secure merchant dashboard, providing multiple paths to access your liquidity without traditional banking hurdles.

What is the benefit of using an MSB-registered gateway like Pallapay?

MSB registration in the US and Canada provides a necessary foundation of institutional trust and regulatory compliance. It ensures the gateway adheres to strict Anti-Money Laundering (AML) and Know Your Customer (KYC) standards, which protects your business from the legal risks associated with unregulated platforms. This professional status is vital for merchants who prioritize long-term stability and want to build a sustainable bridge between e-commerce and global financial markets.

How does the Pallapay Mastercard help with my business liquidity?

The Mastercard provides immediate, real-world access to your settled e-commerce profits without the delays of traditional bank transfers. You can use the card for corporate expenses or to fund trading-related costs directly from your settled balance. This creates a seamless loop where digital sales become tangible purchasing power, ensuring your business remains liquid and responsive to market opportunities in the Gold and Forex sectors.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.