With 39% of U.S. merchants now accepting digital assets, cryptocurrency accounts for over a quarter of their total revenue. Managing this volume is no longer a side project; it’s a core operational pillar. You’ve likely struggled with the friction of 24/7 market volatility and the frustration of tracking inconsistent network fees across various chains. We’ll help you master reconciling crypto sales in accounting to ensure your business remains audit-ready under the latest 2026 reporting standards. This guide provides the technical framework to streamline your month-end close and eliminate manual spreadsheet errors.

Establishing this financial clarity allows you to confidently transition from simple payment acceptance to sophisticated wealth-building strategies. We’ll demonstrate how accurate reconciliation serves as the essential bridge to reinvesting your profits into the transformative world of Forex and Gold CFD trading. By the end of this article, you’ll understand how to turn your digital revenue into a stable, high-performance asset base through professional XAU/USD trading and strategic capital allocation.

Key Takeaways

- Understand the vital role of blockchain verification in maintaining MSB compliance and institutional-grade financial reliability across global jurisdictions.

- Simplify the technical complexity of reconciling crypto sales in accounting by identifying and neutralizing hidden costs like network gas fees and exchange spreads.

- Implement a structured workflow to aggregate and normalize real-time transaction data from crypto POS machines and automated API endpoints into a single functional currency.

- Transition from basic digital asset acceptance to active wealth growth by utilizing audit-ready records as a foundation for high-leverage Gold and USD CFD trading.

- Build a secure bridge between disruptive innovation and established financial practices using an integrated ecosystem designed for professional merchant scalability.

What is Crypto Sales Reconciliation and Why Does It Matter?

Reconciling crypto sales in accounting is the fundamental process of verifying internal merchant records against the immutable data of the blockchain ledger. It serves as the definitive proof that every digital asset received at the point of sale matches the eventual settlement in your financial accounts. For modern merchants, this isn’t just a ledger exercise; it’s the professional foundation that transforms volatile digital transactions into reliable, audit-ready capital. Effective systems for reconciling crypto sales in accounting eliminate the guesswork from high-frequency transaction environments, ensuring that your books reflect reality at every block confirmation.

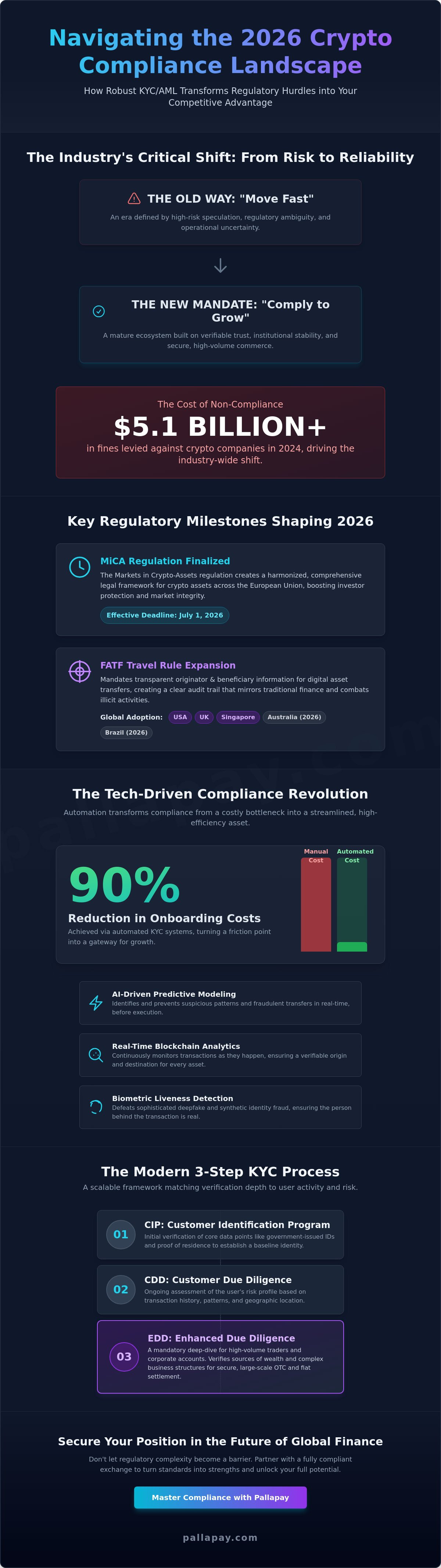

The necessity for precision has reached a critical point as international regulations tighten. Organizations now look toward the Crypto-Asset Reporting Framework (CARF) to standardize how digital asset information is exchanged across borders. Adhering to these standards ensures that your business remains transparent to stakeholders while minimizing tax liabilities that often arise from poorly tracked basis prices or missed network fees. By mastering this process, you bridge the gap between disruptive blockchain innovation and the institutional reliability required by global banking partners.

The Role of MSB Registration in Compliance

Maintaining a regulated status, such as Money Services Business (MSB) registration in the United States or Canada, is a hallmark of institutional financial reliability. When you work with providers that hold these official registrations, your financial statements carry the weight of global banking standards. This level of oversight is essential for passing rigorous anti-money laundering (AML) audits. It ensures that every transaction history is verified and clean, protecting your ability to convert digital revenue into liquid assets through professional fiat settlement services.

Internal Records vs. Blockchain Data

Discrepancies often occur because merchant records are typically off-chain entries that don’t always account for the real-time shifts of on-chain confirmations. Even a variance of a few cents can trigger a red flag during a tax audit, suggesting a lack of control over your financial ecosystem. Accurate reconciliation requires matching the exact timestamp of a sale with the specific block confirmation on the network. The reconciliation gap is the difference between transaction time value and settlement time value. Bridging this gap is the first step toward advanced financial strategies, such as reinvesting settled profits into high-performance markets like Gold and USD CFD trading. Clean records don’t just satisfy regulators; they unlock the leverage needed for significant wealth growth.

Common Challenges in Reconciling Digital Asset Sales

Merchants face a unique set of hurdles when scaling their digital asset acceptance. Managing high-frequency transactions from crypto POS machines requires a level of data precision that traditional retail software often lacks. Unlike credit card settlements that batch daily, crypto transactions occur on individual block times, creating a fragmented data trail across multiple wallets and payment gateways. This fragmentation makes reconciling crypto sales in accounting a labor-intensive process if not supported by an integrated ecosystem. Without a centralized view of these movements, the risk of data silos increases, leading to inaccuracies in the general ledger.

The struggle is amplified by the misalignment between 24/7 blockchain activity and standard business banking hours. While the network never sleeps, traditional financial institutions operate on restricted schedules, creating delays in fiat settlement visibility. This temporal gap requires merchants to maintain rigorous internal logs to ensure that every digital payment is accounted for before it ever hits a bank statement. Mastering the nuances of reconciling crypto sales in accounting is the only way to ensure that these disparate data points align into a cohesive financial narrative.

Volatility and Fair Market Value

Determining the cost basis at the exact moment of sale is the primary accounting challenge. Because markets operate 24/7, the fair market value of an asset can shift significantly between the customer’s checkout and the merchant’s internal ledger entry. Current IRS guidance on digital assets treats these tokens as property, meaning every price fluctuation must be tracked to calculate capital gains or losses accurately. Price slippage during the conversion to fiat can create small but persistent discrepancies that complicate year-end reporting and skew profit margins if left unaddressed.

Network Fees and Processing Commissions

Hidden costs often skew financial statements if they aren’t categorized correctly. Network gas fees should be treated as operational expenses rather than lost revenue, yet many manual systems fail to separate these from the gross sale amount. When using a crypto payment gateway, merchants must also reconcile processing commissions and exchange spreads. Even hardware setup or maintenance fees for physical terminals must be tracked within the general ledger to maintain a clear path to profitability. Overcoming these administrative hurdles allows you to focus on high-impact growth, such as reinvesting settled capital into Gold and USD CFD trading. This transition from commerce to active trading can fundamentally change your financial life, provided your accounting foundation is built on accurate, integrated fiat settlement data.

A Step-by-Step Guide to Reconciling Crypto Sales

Mastering the mechanics of reconciling crypto sales in accounting requires a logical, step-by-step approach that prioritizes data integrity. The process begins with aggregating every transaction point into a single, verifiable dataset. Whether you are processing high-volume API-driven sales through an e-commerce store or managing physical retail transactions via hardware terminals, every entry must be captured. This unified view prevents the data silos that often lead to audit failures and ensures that your financial ledger reflects the true state of your digital assets.

Once you’ve aggregated the raw data, the next critical step is normalization. This involves converting various cryptocurrency values into your functional currency, such as USD or EUR, based on the exact fair market value at the time of each transaction. Establishing this baseline is essential for generating a final reconciliation report that satisfies both internal stakeholders and external regulators. By standardizing these inputs, you create a professional financial foundation that supports both routine compliance and long-term strategic growth.

Data Aggregation and Normalization

Efficiency begins with a centralized merchant dashboard. Use this interface to export a comprehensive transaction history that includes timestamps, asset types, and gross amounts. To maintain accuracy across global operations, you must standardize all timestamps to a single time zone, typically UTC. You should also apply a consistent valuation methodology, such as First-In, First-Out (FIFO) or Last-In, First-Out (LIFO), to ensure your cost basis calculations remain uniform throughout the fiscal year. This technical discipline eliminates the erratic reporting often seen in less mature financial setups.

Matching and Verification

Verification is where you link the blockchain’s immutable Transaction ID (TXID) to the specific invoice within your ERP system. This step is vital for identifying “orphaned” transactions, which are payments received without a corresponding order number. After matching internal records, you must confirm the final conversion of these assets into local bank deposits. Utilizing a professional off-ramp service ensures that your fiat settlements are documented and traceable from the initial block confirmation to the final bank credit.

Clean financial statements are more than a compliance requirement; they are the catalyst for personal and corporate wealth transformation. When you have mastered reconciling crypto sales in accounting, you possess the clear financial visibility needed to reinvest your settled profits into higher-yield opportunities. This precision allows you to confidently enter the world of Forex and Gold CFD trading. By leveraging accurate data, you can transition from simple merchant operations to active wealth management, using XAU/USD trading to change your financial life and secure a more prosperous future.

Leveraging Reconciliation for Advanced Trading and Growth

Clean financial records act as more than just a regulatory shield; they are a vital strategic asset. Moving from digital asset acceptance to active wealth management requires a level of data precision that only professional accounting can provide. When you finish reconciling crypto sales in accounting, you possess a transparent map of your capital. This clarity allows you to transition from a passive recipient of digital payments to a proactive participant in global markets. High-performance growth is built on the back of audit-ready data, turning your daily revenue into a launchpad for sophisticated investment strategies.

Establishing this institutional-grade foundation is the definitive step toward diversifying your business treasury. By reconciling crypto sales in accounting, you eliminate the ambiguity of “hidden” costs and volatility gaps, revealing the true liquid strength of your operation. This verified liquidity is the essential fuel for high-leverage markets. It enables you to move beyond the limitations of standard commerce and enter a space where your capital works with institutional efficiency.

The Path to Forex and CFD Trading

Professional trading accounts require the same level of financial diligence found in traditional institutional finance. To access high-leverage Forex markets, you must demonstrate a consistent and verifiable track record of capital movement. Exploring the mechanics of Gold (XAU) and USD CFD trading offers a sophisticated path for asset protection and wealth accumulation. This calculated market exposure has the transformative potential to change an individual’s financial life. It shifts the focus from simple transaction processing to strategic capital appreciation within the world’s most liquid currency and commodity markets.

Reinvesting Reconciled Profits

Success in modern commerce involves moving settled capital from stablecoin holdings into commodity-backed assets to hedge against inflation. Rapid reinvestment in Forex signals requires the kind of liquid settlement that only a streamlined reconciliation process can guarantee. Reconciled crypto sales provide the liquidity needed for XAU/USD leverage trading. This fluid movement of capital ensures you can act on market opportunities the moment they arise, rather than waiting for manual audits to clear. To begin your journey toward institutional-grade growth, partner with a strategic financial facilitator that handles the complex background processes of settlement and conversion.

Pallapay: Your Partner in Secure and Compliant Crypto Operations

Pallapay positions itself as the definitive destination for merchants who require more than just a digital tool. We offer a sophisticated, integrated ecosystem that handles the complex background processes of digital commerce with institutional reliability. By maintaining a physical presence with OTC desks in major financial hubs like Singapore and Istanbul, we provide a level of security and accessibility that purely digital competitors can’t match. This global footprint ensures that reconciling crypto sales in accounting becomes a streamlined, professional operation rather than a technical burden.

Our platform bridges the gap between disruptive technological shifts and the practical needs of modern commerce. We understand that for a business to scale, it needs a strategic partner that prioritizes stability and utility. We’ve built our services to instill a sense of absolute trust, allowing you to focus on high-level growth while we manage the intricacies of blockchain verification. Mastering the process of reconciling crypto sales in accounting is the first step in a larger journey toward global financial evolution.

Integrated Merchant Solutions

Efficiency is the backbone of our merchant offerings. The Pallapay merchant dashboard includes automated reporting features that aggregate transaction data in real time, eliminating the need for manual spreadsheet entry. We provide direct fiat settlement options to reduce reconciliation complexity and ensure your bank deposits always match your internal sales logs. For high-volume institutional clients, our dedicated OTC desks offer personalized support, ensuring that even the largest capital movements are handled with speed and precision.

Building Absolute Trust and Stability

Our commitment to MSB compliance ensures that every transaction meets the highest global banking standards. We adhere to rigorous crypto security protocols to protect your digital assets from the moment of sale to the point of reinvestment. By utilizing our payment API, you ensure that every sale is tracked and auditable, creating a transparent financial trail for stakeholders. This level of diligence is what allows our partners to confidently transition into advanced markets.

When your accounting is audit-ready, you can explore the transformative potential of trading to change your financial life. Reconciled profits provide the necessary foundation to engage in Gold and USD CFD trading with confidence. By diversifying into XAU/USD markets, you move beyond simple payment processing and into a realm of strategic wealth accumulation. Pallapay is here to facilitate that transition, serving as the professional bridge to your financial future.

Securing Your Financial Future Through Integrated Accounting

Establishing a professional foundation for reconciling crypto sales in accounting is the definitive step toward institutional-grade growth. By eliminating the friction of manual data entry and volatile price tracking, you ensure your business remains audit-ready and compliant with the latest global standards. This clarity does more than satisfy regulators; it reveals the true liquid strength of your operation. As an award-winning global fintech provider serving customers in over 180 countries, Pallapay offers the stability you need to scale. Our official MSB registrations in the USA and Canada guarantee that your financial evolution is built on a secure, regulated framework.

With clean financial records, you’re no longer just processing payments. You’re building a gateway to transformative wealth through Gold and USD CFD trading. Reaching the next level of financial success requires moving beyond simple commerce and into high-performance market participation. It’s time to turn your digital revenue into a high-leverage portfolio that can change your financial life forever. Streamline your crypto settlements with Pallapay today and begin your journey toward active market leadership.

Frequently Asked Questions

What is the most common mistake in crypto sales reconciliation?

The most common mistake is failing to record the fair market value of the asset at the exact moment of the transaction. This oversight creates significant discrepancies when reconciling crypto sales in accounting because the asset’s value often shifts before settlement occurs. Merchants who don’t track these real-time valuations risk overstating capital gains or facing penalties during a tax audit. Accurate data entry at the point of sale is the only way to ensure institutional-grade reliability.

How often should a business reconcile its cryptocurrency transactions?

High-volume merchants should ideally reconcile their transactions daily to maintain data integrity and avoid fragmentation. At a minimum, a monthly reconciliation is required to close the books and ensure your financial statements are accurate. Real-time tracking through an integrated dashboard prevents the accumulation of “orphaned” transactions and simplifies the transition of settled capital into active investment accounts. This consistent discipline ensures that your business remains audit-ready throughout the fiscal year.

Can I use standard accounting software like QuickBooks for crypto reconciliation?

You can use standard accounting software like QuickBooks, but it requires a specialized bridge to import blockchain data effectively. Because these platforms don’t natively track wallet addresses or network fees, merchants must use an API or merchant dashboard to export standardized files. This process ensures that digital asset movements are correctly mapped to traditional charts of accounts. Without this integration, manual entry errors can quickly compromise the accuracy of your financial ledger.

What is the difference between FIFO and LIFO in crypto accounting?

FIFO (First-In, First-Out) treats the oldest assets as the first ones sold, which is the standard methodology for most tax jurisdictions. LIFO (Last-In, First-Out) assumes the most recently acquired assets are sold first, which can be useful in specific market conditions. Choosing a consistent method is essential when reconciling crypto sales in accounting to ensure your cost basis calculations remain uniform. Professional merchants must document this choice to maintain transparency with stakeholders and regulators.

How do I handle gas fees and network costs during reconciliation?

Gas fees and network costs should be categorized as deductible operational expenses within your general ledger. Rather than ignoring these small amounts, you must subtract them from the gross transaction value to determine your true net profit. Tracking these fees individually ensures that your financial records are precise and that you aren’t paying taxes on revenue lost to network congestion. This technical precision is what separates institutional operations from amateur setups.

Why is MSB registration important for my crypto-accepting business?

MSB registration is critical because it signals institutional-grade reliability and compliance with anti-money laundering (AML) regulations. Working with a registered provider ensures that your digital asset operations meet global banking standards in the USA and Canada. This regulated status is essential for merchants who wish to convert their crypto revenue into fiat and access professional trading markets. It provides the security needed to scale without the risk of regulatory friction.

How does reconciling crypto sales help with Forex or Gold trading?

Accurate reconciliation provides the verified financial history needed to qualify for high-leverage professional trading accounts. When your records are audit-ready, you can confidently reinvest settled profits into Gold and USD CFDs to hedge against inflation. This transition from passive commerce to active wealth management is only possible when you have a transparent view of your available liquidity. It allows you to use your business revenue to change your financial life through strategic market exposure.

What documentation is required for a crypto accounting audit?

You must maintain a comprehensive digital trail that includes Transaction IDs (TXIDs), exact timestamps, and fair market value at the time of sale. Additionally, you should keep all corresponding invoice numbers and bank deposit confirmations for fiat settlements. This documentation proves the legitimacy of your revenue and ensures a seamless experience during any regulatory audit. Comprehensive records are the professional bridge between disruptive technology and established financial reliability.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.