Why should your capital remain idle just because a traditional bank decided to close its doors for the weekend? Many traders experience the frustration of a missed opportunity in the volatile XAU/USD market because their funds are trapped behind a slow ACH or SEPA wall. When you need to sell crypto after hours to capture a sudden market shift, banking delays feel like an obsolete barrier to your growth. You deserve a professional bridge that connects the speed of digital assets with the stability of institutional finance.

This article reveals how to access spendable fiat or cash instantly to pivot your liquidity into the transformative potential of Gold and Forex CFD trading. You’ll learn to bypass the typical 11% increase in weekend trading costs by using regulated off-ramp solutions that prioritize speed and safety. We will examine the mechanics of secure technical integrations and show you how to leverage the current $4,086.93 gold price to accelerate your financial progress through a sophisticated, integrated ecosystem.

Key Takeaways

- Identify the operational friction of traditional banking hours and how to bypass weekend liquidity traps to keep your capital active.

- Discover professional strategies to sell crypto after hours for instant access to spendable fiat through secure off-ramping and the Pallapay Mastercard.

- Master the transition into high-liquidity markets like Gold (XAU/USD) and Forex to diversify your portfolio with institutional-grade CFD trading.

- Unlock the transformative potential of leveraging market volatility to generate growth in both bullish and bearish environments.

- Ensure your transactions remain secure and compliant by utilizing a regulated financial bridge that connects digital assets to global commerce.

The Weekend Liquidity Gap: Why Traditional Banks Fail Crypto Holders

Digital assets never sleep. While blockchain protocols facilitate global transactions every second of the year, the legacy banking infrastructure remains anchored to a 19th-century schedule. This friction creates a liquidity trap for investors. If a market opportunity arises on a Saturday afternoon, waiting for a bank to open on Monday morning isn’t just an inconvenience; it’s a strategic failure. Market liquidity is the lifeblood of successful trading, yet traditional rails like SEPA and ACH are designed for stability over speed, not the real-time demands of the modern economy.

Traders who need to sell crypto after hours often find themselves paralyzed by settlement delays. Research shows that cryptocurrency trading costs increase by an average of 11% on weekends, while overall displayed liquidity drops by over 5%. When you’re forced to wait 48 to 72 hours for funds to clear, you face the very real risk of market slippage. By the time your fiat hits your account, the entry point for a lucrative gold CFD trade may have vanished. Relying on these outdated systems in 2026 is a disadvantage that professional market participants can no longer afford.

The Reality of Instant Bank Transfers

Many modern banking apps promise “instant” transfers, but there’s a vital distinction between an authorized transaction and a settled one. While the numbers might appear in your dashboard, the actual movement of value often remains pending until the next business day. Banks frequently flag significant crypto-to-fiat movements during after-hours periods, triggering automated compliance holds. Intermediary banks further complicate this process; they add layers of verification that slow down global off-ramping when time is of the essence.

Breaking Free from the Banking Schedule

The evolution of finance has shifted toward non-bank-dependent ecosystems. Professional traders now utilize regulated fintech providers to bridge the gap without relying on traditional rails. These platforms operate as a professional facilitator, allowing you to access a crypto offramp that functions independently of the 9-to-5 clock. A pre-verified strategy is essential for high-volume traders. It ensures that when you need to sell crypto after hours, your capital is ready to be redeployed into gold or forex markets instantly, protecting your purchasing power from the erosion of time and volatility.

Instant Off-Ramp Solutions: How to Sell Crypto for Cash Today

Accessing liquidity shouldn’t be a waiting game. While centralized exchanges often tether your funds to the processing speeds of legacy banks, dedicated crypto off-ramp services provide a direct path to spendable value. These solutions operate outside the standard banking cycle, allowing you to liquidate assets when you need them most. Whether you require physical cash for a private transaction or digital fiat for immediate reinvestment, modern financial bridges eliminate the friction of weekend downtime. This infrastructure ensures that your capital remains as agile as the markets you trade.

For many investors, the primary goal is to sell crypto after hours without triggering the red flags or delays common with retail banking transfers. The shift toward regulated fintech ecosystems has made this possible. By utilizing a professional off-ramp strategy, you maintain control over your assets 24/7, ensuring that you’re never caught in a liquidity trap when a high-stakes opportunity arises in the commodities or forex markets.

Over-the-Counter (OTC) Desks: The Professional Choice

OTC desks represent the gold standard for high-volume traders who need to sell crypto after hours without affecting global market prices. Unlike public exchanges where large orders can cause significant slippage, OTC operations facilitate private, large-scale trades with deep liquidity. Security is a cornerstone of these transactions. Professional desks utilize rigorous protocols that align with broader regulatory perspectives, such as those discussed by FINRA on Crypto Assets, to ensure every conversion is compliant and safe. For those seeking immediate physical liquidity, the process is streamlined. You can often convert digital holdings into physical cash in under 30 minutes at secure financial hubs, bypassing the risk of bank account freezes entirely.

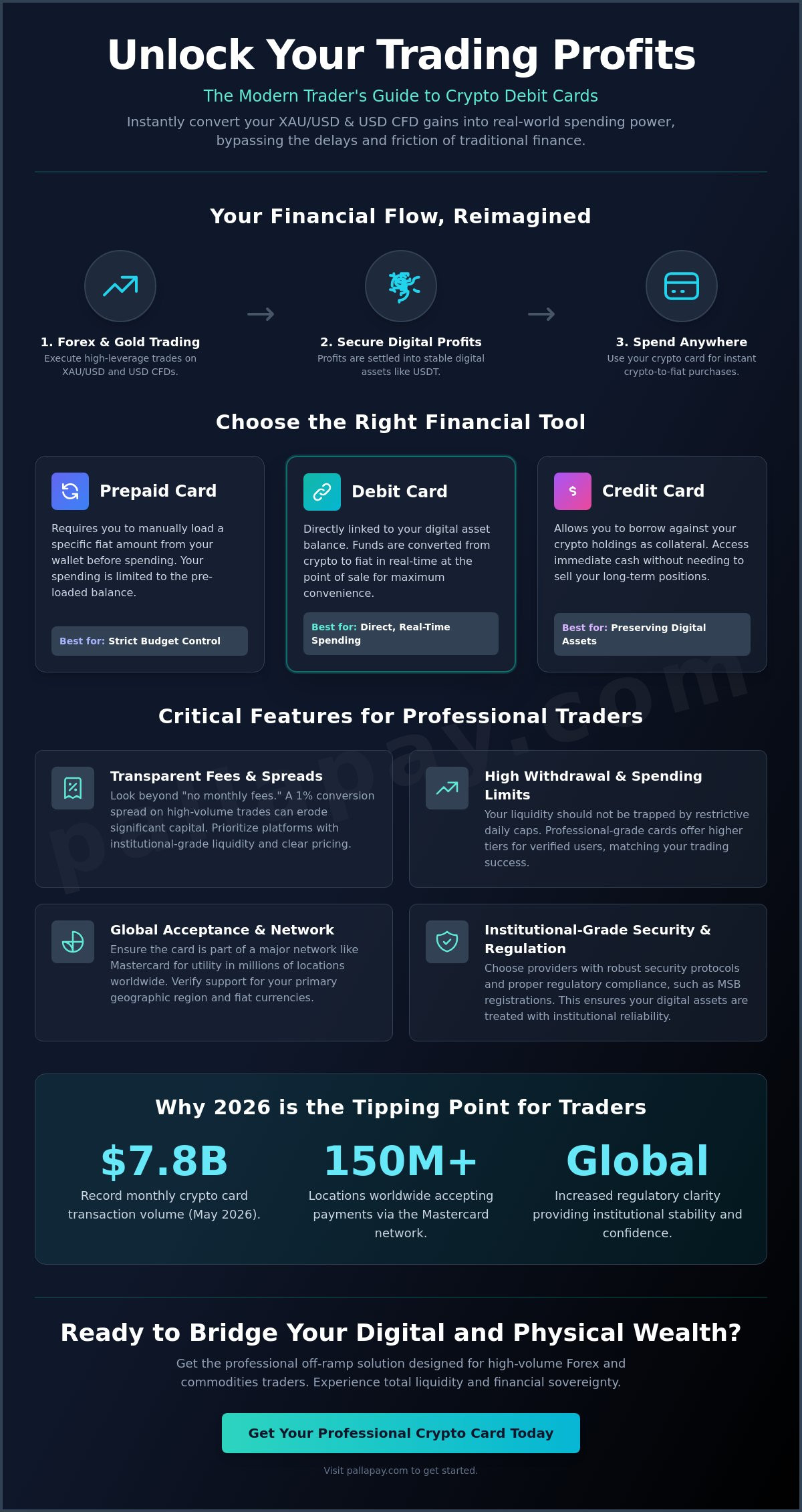

Crypto Debit Cards and Fintech Settlement

The most efficient way to maintain 24/7 spending power is through an integrated fintech ecosystem. The Pallapay Mastercard serves as a vital tool in this regard, converting your crypto at the point of sale instantly. By keeping your capital within a regulated fintech framework, you avoid the scrutiny and delays often associated with traditional retail banks. This setup allows for seamless management of your wealth, providing a bridge between your digital portfolio and real-world expenses.

- Instant conversion to fiat at any global POS terminal.

- Secure management of daily spending limits for maximum liquidity.

- Reduced exposure to banking holidays and settlement traps.

This level of integration is essential for traders who view their crypto not just as a static investment, but as a dynamic source of funding for active market participation. If you’re ready to secure your financial agility, you might consider how an integrated digital wallet can simplify your daily operations.

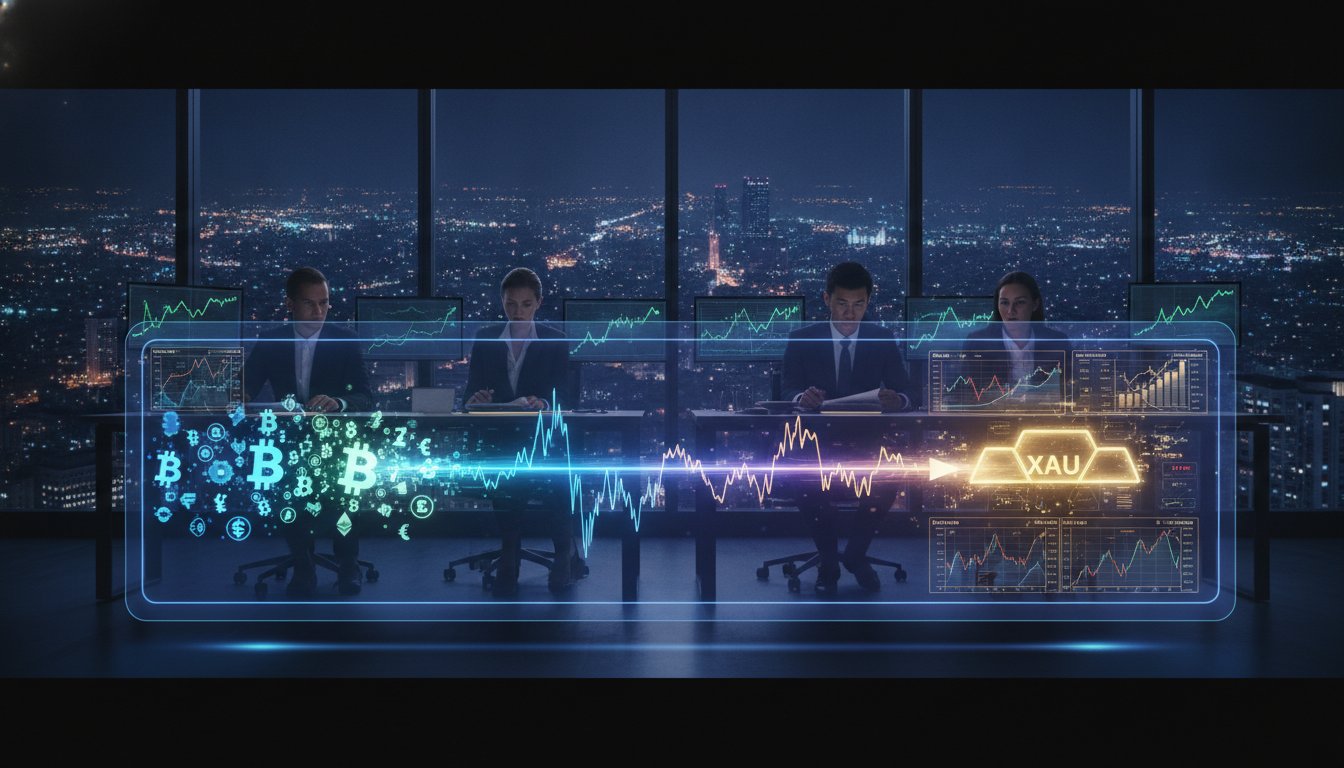

Beyond Liquidity: The Transformative Potential of CFD Trading

Strategic participants view liquidity as a gateway to broader market engagement rather than a final destination. Converting digital holdings into fiat is the first step toward a more active financial strategy that transcends the limitations of passive holding. When you choose to sell crypto after hours, you aren’t just exiting a position; you’re unlocking the capital necessary to enter high-volume commodity markets. This pivot allows you to treat your digital assets as the high-performance fuel required for global trade.

Contracts for Difference (CFDs) represent a sophisticated evolution for the modern investor. Unlike traditional asset ownership, CFD trading enables you to capitalize on price movements in both rising and falling markets. This flexibility is essential for navigating the volatility of 2026. As discussions regarding global crypto regulation continue to evolve, utilizing regulated platforms for these transitions ensures that your growth is built on a foundation of institutional reliability and security.

Why CFDs Are the Ideal Crypto Pivot

High-leverage environments allow you to maximize your purchasing power by controlling larger positions with a smaller initial capital outlay. By using a portion of your liquidated crypto, you can engage with traditional Forex pairs to hedge against broader market risks. This margin-based approach transforms your portfolio from a static collection of tokens into a dynamic trading engine. CFD trading is a specialized mechanism that provides the financial agility required to thrive in the volatile markets of 2026. It allows for a seamless transition between the disruptive world of crypto and the established reliability of global commodities.

The Path to Financial Independence Through Trading

The ultimate goal for many is a diversified, self-sustaining portfolio that isn’t dependent on a single asset class. Gold (XAU/USD) remains the premier safe-haven asset for those looking to preserve and grow wealth during periods of digital uncertainty. By utilizing a professional off-ramp service to secure immediate liquidity, you can pivot into the gold market at a moment’s notice. This strategy moves you away from the erratic swings of the crypto sector and toward the consistent volume of the Forex markets.

- Diversify risk by moving crypto gains into XAU/USD and major currency pairs.

- Capitalize on market downturns through short-selling capabilities.

- Access 24/5 liquidity in global Forex markets to complement your 24/7 crypto agility.

Success in this arena requires more than just a desire to trade; it requires an integrated infrastructure. It’s not enough to sell crypto after hours and wait for a traditional bank to process the funds. You need a strategic partner that offers both the immediate off-ramping capabilities and the institutional-grade trading tools necessary to act on real-time data. This holistic approach is what separates casual participants from strategic traders who are building lasting financial independence.

Focusing on the Standard: Trading Gold (XAU/USD) and Forex

Establishing a foothold in traditional markets requires more than just capital; it requires a shift toward assets with proven, institutional stability. While digital assets offer high-growth opportunities, Gold (XAU/USD) remains the ultimate safe-haven for preserving wealth against market turbulence. The ability to sell crypto after hours and immediately transition into the gold market provides a strategic layer of protection that passive holding cannot match. By analyzing the correlation between Bitcoin volatility and gold price action, traders can identify risk-off environments where capital flight toward precious metals is most likely to occur.

Professional traders utilize a fiat settlement infrastructure to move their liquidated gains directly into active trading accounts. This seamless flow of capital ensures that you are never sidelined by banking delays. Instead of waiting for a traditional wire to clear, your liquidity is ready to be deployed into the 24/5 Forex markets, where currency pairs like EUR/USD and GBP/USD offer a level of depth and reliability that is fundamental to institutional finance.

Mastering the XAU/USD Pair

Gold is the benchmark for wealth preservation in the digital age, currently trading at $4,086.93 as of June 2026. Crypto traders entering the Gold CFD market should focus on technical indicators such as the Relative Strength Index (RSI) and long-term moving averages to identify overextended price action. During periods of fiat currency inflation, gold serves as a critical hedge. A disciplined strategy involves moving a percentage of crypto gains into gold CFDs when the digital market shows signs of overheating, effectively locking in purchasing power while maintaining market exposure.

Forex Market Dynamics for Crypto Users

The transition from crypto to Forex allows you to engage with the most liquid market in the world. The global foreign exchange market generates approximately $7.5 trillion in daily turnover, providing a liquidity pool that is significantly more robust and less prone to individual manipulation than the emerging digital asset sector. Major pairs such as EUR/USD, GBP/USD, and JPY/USD provide consistent opportunities for those who understand the mechanics of interest rate differentials and macroeconomic data releases. By using leverage responsibly, you can grow a modest crypto off-ramp into a significant trading fund, provided you maintain strict risk management protocols.

The integration of these markets represents the future of professional wealth management. If you are prepared to secure your financial agility and capitalize on global commodity trends, you can start your off-ramp process today to ensure your capital is always where the opportunity is greatest.

Pallapay: Your Regulated Bridge to Global Financial Markets

Reliability is the foundation of any successful trading strategy. While earlier sections highlighted the necessity of liquidity and the potential of XAU/USD markets, those opportunities are only accessible through a secure, institutional-grade gateway. Pallapay provides the essential infrastructure for traders who need to sell crypto after hours without compromising on compliance or security. By bridging the gap between disruptive technology and established financial oversight, the platform ensures your capital remains mobile and protected 24/7.

High-volume traders and institutional participants require specialized tools to manage large-scale transitions. Pallapay supports these needs through professional off-ramp services and dedicated OTC desks designed to handle significant volume without market slippage. For those utilizing automated strategies, the integration of secure Payment APIs facilitates real-time settlements, allowing you to move from crypto gains to forex trading accounts with surgical precision. This level of technical integration is what allows a modern business to accelerate its progress in an increasingly complex global economy.

Compliance and Security in 2026

In the current regulatory environment, MSB registration in the United States and Canada is the gold standard for service providers. This status provides a layer of institutional trust that unregulated platforms simply cannot offer. Your assets are protected by advanced multi-sig wallet architectures and high-level encryption protocols, ensuring that every transaction is as secure as it is fast. You can explore more about crypto security to understand how these safeguards protect your high-volume trades during after-hours operations.

Getting Started with the Pallapay Ecosystem

Setting up your account is a streamlined process designed for efficiency. Once verified, you gain immediate access to a comprehensive suite of tools that allow you to sell crypto after hours and convert digital holdings into spendable fiat or physical cash. Integrating this liquidity into your broader strategy is made effortless through the OTC crypto exchange, which provides the deep liquidity necessary for pivoting into gold or forex CFDs. This is more than just a service; it’s a strategic partnership that handles the complex background processes so you can focus on market growth.

The transition from a passive holder to an active, diversified trader requires the right tools and a reliable partner. By adopting a regulated, utility-focused ecosystem, you secure the agility needed to thrive in the world’s most liquid markets. Start your journey toward financial transformation today and experience the stability of a global industry leader.

Securing Your Financial Agility in 2026

The transition from passive asset holding to active market engagement is the definitive path to long-term wealth preservation. You’ve explored how bypassing banking delays allows you to capture volatility in the XAU/USD and Forex markets without the friction of traditional settlement cycles. When you choose to sell crypto after hours, you’re not just accessing cash; you’re positioning yourself to thrive in a 24/7 global economy that rewards speed and precision.

Pallapay serves as your institutional partner, offering a presence in 180+ countries and the security of official MSB registration in the USA and Canada. Whether you utilize our physical OTC desks for instant cash settlement or our digital off-ramps for seamless trading pivots, we provide the stability you need to grow. Access instant liquidity and start your trading journey with Pallapay today.

The future of finance is integrated, efficient, and entirely within your control. Take the next step toward your financial transformation and start trading with confidence.

Frequently Asked Questions

Can I sell crypto for cash on a Sunday?

Yes, you can access physical liquidity on weekends by utilizing professional OTC desks that operate independently of the traditional banking schedule. While retail banks remain closed, digital asset markets continue to function 24/7. Specialized providers ensure that you can bypass the weekend liquidity gap and receive physical cash for your assets even on a Sunday, providing the agility required for immediate reinvestment or personal use.

What is the fastest way to get fiat from crypto without a bank?

The most efficient method to acquire fiat without a bank is through a crypto debit card or a physical OTC crypto exchange. These solutions provide a direct bridge to spendable value, allowing you to sell crypto after hours and receive cash or POS spending power in minutes. This strategy eliminates the standard 48 to 72-hour settlement delays associated with legacy ACH or SEPA transfer systems.

Is CFD trading safer than holding cryptocurrency?

Safety in trading is defined by risk management and market flexibility rather than simple asset ownership. CFD trading provides a strategic advantage over passive holding by allowing you to profit from both rising and falling markets. While holding crypto leaves you vulnerable to downward volatility, trading CFDs on Gold or Forex enables you to hedge your positions and protect your capital during periods of digital uncertainty.

How do I trade Gold (XAU/USD) using my crypto gains?

You can transition into the gold market by liquidating your digital assets through a regulated off-ramp and funding a CFD trading account. This process allows you to pivot from the volatile crypto sector into the XAU/USD pair, which serves as the global standard for wealth preservation. It’s a sophisticated way to diversify your portfolio and secure your gains in a high-volume, institutional commodity market.

Will my bank close my account if I receive a large crypto transfer?

Traditional banks frequently flag or freeze accounts that receive large, unexplained transfers from cryptocurrency exchanges due to automated compliance protocols. To avoid this risk, professional traders utilize regulated off-ramps and OTC services that provide transparent documentation. Moving your funds through a dedicated fintech ecosystem ensures that your crypto-to-fiat activities remain professionally separated from your primary retail banking relationship.

What are the fees for selling USDT for cash at an OTC desk?

Fees for OTC transactions are generally structured to accommodate high-volume traders and are often more competitive than the slippage costs found on public exchanges. While specific rates depend on market depth and transaction size, using an OTC desk allows you to sell crypto after hours with a locked-in price. This provides a level of cost certainty that is essential for maintaining a disciplined and profitable trading strategy.

How does the Pallapay Mastercard work when banks are closed?

The Pallapay Mastercard operates on a regulated fintech rail that converts digital assets to fiat at the exact moment of purchase. This system functions independently of the legacy banking clock, meaning you can spend your crypto at any global POS terminal on weekends or holidays. It ensures that your liquidity is always available, regardless of whether traditional financial institutions are open for business.

Do I need a traditional bank account to use Pallapay services?

You don’t require a traditional bank account to utilize the core features of the ecosystem, such as the Mastercard or physical OTC cash settlements. These services are designed to provide a comprehensive, standalone financial bridge for the modern trader. By managing your wealth within a secure fintech framework, you maintain absolute agility and avoid the friction often associated with the legacy banking sector.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.