Why wait three business days for a bank to approve your gold trading profits when your next market opportunity is happening in seconds? High-performance traders understand that liquidity is the lifeblood of success. You’ve mastered the volatility of the XAU/USD pair and scaled your accounts, yet the friction between a closed CFD position and actual spending power remains a frustrating bottleneck. Learning how to spend usdt with a debit card is the essential final link in a modern trading ecosystem, allowing you to bypass the slow pace of traditional banking that often holds you back.

This shift transforms your digital gains into immediate real-world utility, specifically supporting the high-frequency lifestyle of Forex and CFD professionals. By bridging the gap between disruptive innovation and institutional reliability, you can finally access your capital the moment a trade closes. This article explores how to integrate your trading profits into traditional commerce while maintaining your edge. We will detail the technical shift toward automated conversion, the impact of 2026 regulations, and the tools that allow you to move from a winning trade to a physical purchase in seconds.

Key Takeaways

- Gain immediate liquidity by integrating digital assets into traditional commerce to support active market participation.

- Master how to spend usdt with a debit card to bridge the gap between high-leverage CFD gains and daily financial requirements.

- Utilize USDT as a stable base currency for XAU/USD and Forex pairs to streamline your profit extraction and asset management.

- Evaluate professional-grade cards based on fee transparency and ATM capabilities that support a high-frequency trading lifestyle.

- Leverage the Pallapay Mastercard ecosystem to facilitate a seamless wealth cycle from market execution to real-world spending.

The Evolution of Digital Liquidity: Why Spending USDT with a Card is the New Standard

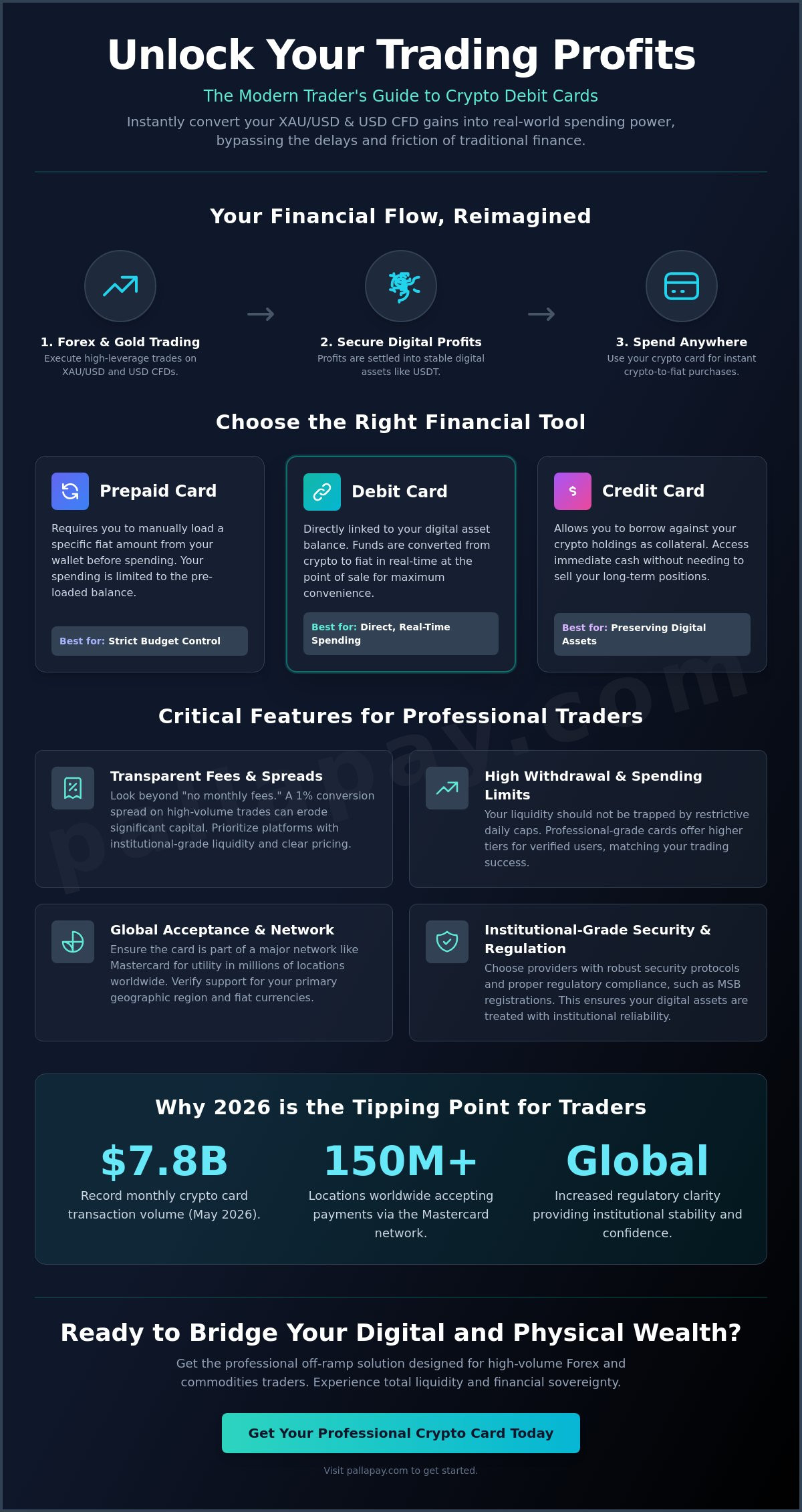

The 2026 economy demands more than passive asset accumulation; it requires immediate utility. For years, the cryptocurrency sector focused on long-term holding, yet this strategy often left professional traders with “paper gains” that were difficult to deploy in the physical world. High-performance traders, particularly those focused on Gold (XAU/USD) and major currency pairs, require a more agile approach. Understanding how to spend usdt with a debit card is now a fundamental skill for those managing high-performance portfolios. This shift from holding to utilizing digital assets marks a transition toward a truly integrated financial lifestyle where your trading account and your daily spending are no longer separated by slow banking intermediaries.

Tether remains the preferred medium for this integration because of its 1:1 USD peg, providing a stable foundation that volatile assets cannot match. By utilizing a sophisticated crypto off-ramp, investors eliminate the conversion friction that once plagued the industry. This technological bridge explains how to spend usdt with a debit card by converting digital tokens into fiat currency at the exact moment of a transaction, ensuring that your capital is always ready for deployment.

Breaking the Barrier Between Crypto and Commerce

Modern card solutions function by executing a real-time settlement process that occurs in the background during a purchase. When you swipe your card at a terminal, the system instantly calculates the required USDT, converts it to the local fiat currency, and completes the transaction within seconds. This process preserves your purchasing power by avoiding the multi-day price fluctuations often seen with traditional bank transfers. A USDT spend card is a streamlined liquidity tool designed to provide the modern investor with instant access to capital across global payment networks.

The benefits of this real-time integration include:

- Instant settlement that bypasses the standard 48 to 72-hour banking clearing cycles.

- The ability to use virtual cards for secure online commerce or physical cards for point-of-sale transactions.

- Direct access to trading profits without needing to move funds through multiple exchange accounts.

The Strategic Advantage of Tether (USDT) for Cardholders

Stability is the primary reason why Tether (USDT) has become the dominant stablecoin for global card programs. While Bitcoin and Ethereum are excellent for speculative growth, their price swings make them impractical for daily budgeting or paying for high-value services. If you’ve just closed a profitable USD CFD trade, you want that profit to remain stable until the moment you spend it. USDT provides this predictability, acting as a digital mirror to the US Dollar while maintaining the technical advantages of blockchain technology.

Security is equally paramount for high-balance cardholders. Modern card issuers employ institutional-grade encryption and multi-signature protocols to ensure that your funds remain protected, whether they’re sitting in your wallet or moving through the TRON or Ethereum networks. This level of security, combined with the global reach of Mastercard and Visa networks, ensures that your trading success translates into a reliable, high-quality financial life. You don’t have to worry about the complexities of cross-border currency exchange; the system handles the technical background, leaving you free to focus on your next market entry.

From Market Gains to Real-World Utility: How USDT Cards Empower CFD Traders

For the professional trader, the separation between a brokerage account and a personal bank account has long been a source of operational friction. CFD trading, particularly when utilizing high leverage, produces rapid shifts in capital that require equally rapid settlement solutions. Mastering how to spend usdt with a debit card provides the essential bridge that allows a trader to close a position and immediately access that value in the physical world. This synergy between high-performance trading and instant off-ramps creates a closed-loop financial system where success is not just a number on a screen, but a liquid resource available for immediate use.

The institutional reliability of Tether (USDT) makes it the ideal base currency for settlement. As the landscape of stablecoin regulation matures in 2026, professional traders increasingly prefer USDT-backed accounts for their predictability and speed. This stability is vital when trading volatile assets like Gold (XAU/USD) or major Forex pairs. By maintaining profits in a stablecoin and utilizing a direct card integration, you eliminate the need to navigate the slow, often unpredictable processing times of traditional wire transfers. It’s a strategic evolution that allows you to see your trading success reflected in your daily spending habits, reinforcing a disciplined and successful trading psychology.

Trading Gold (XAU/USD) and the Path to Financial Freedom

Gold remains the ultimate haven for CFD traders, and the 2026 market has introduced unprecedented volatility that rewards disciplined, technical analysis. Trading XAU/USD through a CFD model allows you to capitalize on both rising and falling prices without the logistical burden of physical storage. This flexibility is what enables a life-changing career shift; the ability to generate supplemental income can quickly evolve into total financial independence when you have the right tools to manage your gains. When you understand how to spend usdt with a debit card, the profits from a successful afternoon of gold trading can be spent by evening, providing a tangible reward for your market expertise—such as upgrading your home fitness setup with equipment from Gym Pros.

USD CFD Trading: Capitalising on Global Currency Fluctuations

Navigating the fluctuations of major USD pairs requires an account structure that is as efficient as the trades themselves. Professional traders now prioritize accounts that offer seamless movement from a brokerage platform to a crypto off-ramp, ensuring that liquidity is never more than a few clicks away. CFD trading on USD pairs serves as a strategic hedge against local currency devaluation in an increasingly globalised economy. This efficiency is best realized through the Pallapay Mastercard, which allows for the instantaneous conversion of trading profits into usable fiat at any point of sale. By automating the flow from your trading wallet to your card, you ensure that your capital is always working for you, whether it is positioned in the market or funding your lifestyle.

Evaluating the Best Crypto Cards for Active Traders

Choosing the right platform to learn how to spend usdt with a debit card involves more than comparing cashback rewards. For a professional trader, a card is a strategic tool that must handle significant volume without operational delays. High-performance trading in gold or currency pairs generates substantial liquidity, and your card must reflect that scale. You should prioritize providers that offer high daily spending limits and substantial ATM withdrawal caps. A card with restrictive limits won’t support a lifestyle funded by successful CFD trading; it only creates another barrier between your success and your capital.

Compliance and global reach are the next pillars of evaluation. In 2026, regulatory clarity is essential for asset protection. Active traders should look for providers with MSB registration in major jurisdictions like the US and Canada to ensure institutional-grade oversight. This oversight is part of a broader shift in how stablecoins are regulated, providing a layer of security that was missing in the early days of digital assets. Additionally, ensure your card is accepted in 180+ countries. True financial freedom means your trading profits are accessible whether you’re in London, Tokyo, or New York, without regional blocks or unexpected declines.

Security Features for High-Volume Cardholders

Security is the foundation of any professional financial tool. High-volume traders require more than just a password; they need multi-layered protection. Standard features should include two-factor authentication (2FA) and biometric card management through a dedicated mobile app. The ability to freeze and unfreeze your card instantly is a non-negotiable requirement for protecting high balances. Regulated providers like Pallapay implement these rigorous protocols to ensure that your trading gains remain secure while providing the convenience of a modern crypto wallet. It’s about maintaining total control over your assets at all times.

Fee Structures and Trading Margins

Every fee you pay is a direct deduction from your trading ROI. When you’re calculating the success of a gold (XAU/USD) position, you must account for the cost of moving those profits into the real world. Professional traders look for fee transparency, distinguishing clearly between conversion fees, monthly maintenance costs, and load fees. A low-to-zero spread on crypto-to-fiat conversions is often more valuable than a high cashback percentage. You should also consider the utility of your card types; virtual cards are often more efficient for secure e-commerce, while physical cards remain the standard for retail and high-value physical purchases. By optimizing your how to spend usdt with a debit card strategy, you protect your margins and maximize the impact of every successful trade.

Maximising Financial Impact: Strategies for Spending USDT Profits

Success in the Forex market is ultimately measured by the liquidity of your gains. A disciplined trader doesn’t just accumulate digital balances; they establish a robust wealth cycle. This cycle involves reinvesting a portion of CFD profits to compound growth while simultaneously funding a high-quality lifestyle. Automating the flow from your trading account to your card ensures that your rewards are as immediate as your market execution. Learning how to spend usdt with a debit card is the definitive solution for those who want to bypass the antiquated delays of traditional bank wires, which can often take several business days to clear. By removing these bottlenecks, you ensure that your capital remains under your direct control at all times.

The efficiency of the Pallapay ecosystem allows for a seamless transition from market gains to physical spending. Consider a case study of a professional trader focused on XAU/USD volatility. Instead of navigating the friction of local banking limits and conversion fees, this trader moves profits directly into a USDT-backed card. This strategy provides a secure crypto off-ramp that operates in real-time, allowing for a life of financial agility that traditional systems simply cannot match.

Transforming Your Financial Life Through Strategic Trading

Cross-Border Spending for the Global Nomad

Modern traders are rarely tethered to a single location. High-frequency trading allows for a nomadic lifestyle, but traditional credit cards often penalize this freedom with high foreign transaction fees. Integrating the Pallapay Wallet into your financial stack solves this by providing a multi-currency gateway for global asset management. You can manage your funds and spend in local currencies at any point of sale with institutional-grade efficiency. This integration is essential for international business travel, ensuring that your trading profits are accessible in over 180 countries. To experience this level of financial integration and secure your trading liquidity, you can apply for the Pallapay Mastercard today. This approach ensures that your capital is never idle, moving from market gains to real-world utility in a single, secure flow.

The Pallapay Mastercard: Your Gateway to Global Spending and Trading Liquidity

The Pallapay Mastercard serves as the definitive point of convergence between your trading success and your financial reality. For the professional trader, a card isn’t just a payment method; it’s a strategic liquidity tool that must handle significant capital flows with institutional reliability. This card is engineered to support the high-volume requirements of active Forex and CFD participants, providing a seamless link to the broader Pallapay OTC and exchange ecosystem. By integrating your trading gains directly into a high-limit spending solution, you eliminate the traditional barriers that have historically separated digital asset growth from real-world utility.

If you’ve been evaluating how to spend usdt with a debit card that matches the scale of your gold or USD CFD positions, the Pallapay Mastercard offers the necessary infrastructure. It provides the high spending limits and ATM withdrawal caps required by high-net-worth individuals and career traders. This ensures that your financial life isn’t restricted by the low ceilings often found with retail-focused crypto cards. Instead, you gain a professional-grade tool that reflects your performance in the markets, allowing for the immediate deployment of capital across global networks.

The Professionals Choice for Crypto Off-Ramping

Security and regulatory compliance form the backbone of the Pallapay ecosystem. Our MSB registration provides high-scale users with the peace of mind that their assets are managed within a transparent and secure framework. This institutional grounding is essential when handling the significant profits generated from successful XAU/USD trading. The speed of the Pallapay Off-Ramp service ensures that even large-scale withdrawals are processed with the efficiency that modern commerce demands.

For traders who also operate as business owners, the ecosystem offers even deeper integration. You can link your financial management to the Pallapay POS infrastructure, creating a holistic cycle of digital and fiat transactions. This comprehensive approach positions Pallapay not just as a service provider, but as a strategic partner in your long-term financial evolution. The ability to move from a closed trade to a business purchase or a personal investment in seconds is the ultimate competitive advantage in the 2026 economy.

Steps to Secure Your Financial Future

Securing your liquidity through the Pallapay Mastercard is a streamlined and compliant process designed for the efficiency-oriented professional. The path from market gains to global spending power is direct:

- Complete the streamlined account verification process to ensure full compliance and asset protection.

- Link your trading wallet to the Pallapay ecosystem to facilitate instant transfers.

- Fund your card using USDT profits from your Forex or CFD trading accounts.

- Begin spending your digital gains at millions of locations worldwide with real-time conversion.

Mastering how to spend usdt with a debit card is the final step in a successful trading career. It allows you to transform market volatility into a stable, high-quality lifestyle. By choosing a partner that understands the mechanics of high-performance trading and the necessity of instant liquidity, you ensure that your capital is always ready for its next deployment. Apply for your Pallapay Mastercard today and unlock your trading potential.

Secure Your Trading Legacy with Institutional Liquidity

The convergence of digital asset stability and global payment networks has redefined what it means to be a successful trader. By mastering how to spend usdt with a debit card, you ensure that your performance in the gold and USD CFD markets translates into immediate spending power. This transition from passive accumulation to active utility is the hallmark of a modern financial legacy. It’s about ensuring your capital is as mobile as your strategy, allowing you to move from a winning trade to a physical purchase without the friction of traditional banking delays.

As a regulated MSB in the USA and Canada, Pallapay provides a secure, institutional-grade bridge that serves professional users in over 180 countries. Our ecosystem offers seamless integration with OTC desks and POS systems, ensuring your high-volume requirements are always met with absolute reliability. We prioritize the speed and safety that high-performance traders demand, providing a foundation for long-term growth and immediate access.

Empower your trading lifestyle with the Pallapay Mastercard. Your trading journey deserves a financial partner that moves as fast as the markets do; it’s time to align your digital gains with your real-world ambitions. Take control of your liquidity and experience the freedom of a truly integrated financial future.

Frequently Asked Questions

Is spending USDT with a card legal and regulated?

Spending USDT with a card is legal in jurisdictions where digital assets are recognized as a valid medium for payments and commerce. In 2026, the regulatory environment is defined by established frameworks like the MiCA regulation in Europe and MSB registrations in the United States and Canada. These regulations ensure that card providers maintain high standards of security and transparency while adhering to global anti-money laundering protocols.

What are the typical fees associated with a USDT spend card?

Fee structures typically include conversion fees, load fees, and monthly maintenance charges. Active traders should also be aware of ATM withdrawal fees and potential foreign transaction costs when using the card internationally. Understanding these components is essential for managing the overall ROI of your trading activities and ensuring that your profit extraction remains cost-effective.

Can I use a USDT card for Forex and CFD trading withdrawals?

Yes, you can facilitate withdrawals by moving your trading profits from a brokerage account to your card-linked wallet. This method is the preferred solution for those learning how to spend usdt with a debit card because it bypasses the multi-day delays associated with traditional bank wires. It provides immediate liquidity for gains made in gold or USD currency pairs, allowing for a more agile financial lifestyle.

How does a USDT card handle currency conversion when travelling?

Currency conversion occurs automatically at the point of sale through a real-time settlement process that calculates the exchange rate between USDT and the local fiat currency. This allows traders to spend their assets across 180 countries without the need for manual pre-conversion. The system handles the technical background work, ensuring that your purchasing power remains stable regardless of your geographic location.

What is the difference between a virtual and a physical crypto card?

Virtual cards are issued instantly for secure online transactions and digital subscriptions, while physical cards are required for retail point-of-sale use and ATM access. Both options are integral to how to spend usdt with a debit card strategies, allowing you to choose the format that best fits your immediate needs. Physical cards provide the added benefit of tangible cash access, which is often necessary for high-value commerce.

Are there spending limits on USDT cards for high-volume traders?

Spending limits are standard and vary based on the provider’s tier system and the user’s verification status. High-performance traders should select cards with elevated daily and monthly limits to accommodate the significant liquidity generated from successful CFD trading. These limits are designed to support a sophisticated lifestyle while maintaining compliance with institutional security requirements.

How secure is my USDT when held in a card-linked wallet?

Security is maintained through multi-layered protocols, including two-factor authentication, biometric card management, and institutional-grade encryption. Regulated providers ensure that your trading gains are protected against unauthorized access while remaining fully liquid. This level of security is a cornerstone of professional financial tools, allowing you to manage large balances with absolute confidence.

Can I spend USDT with a card at any merchant that accepts Mastercard?

Yes, you can spend your assets at any merchant within the global Mastercard network, as the conversion to fiat happens instantly in the background. The merchant receives their local currency as they would with any traditional debit transaction, making the process seamless for both parties. This integration bridges the gap between modern digital assets and established global commerce systems.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.