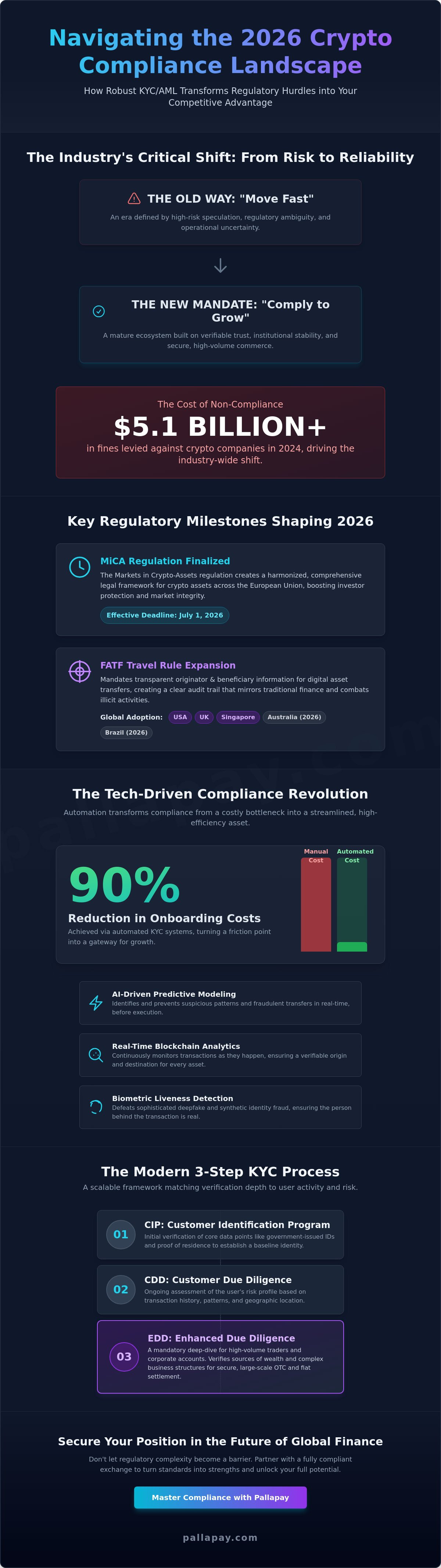

Approximately 47% of crypto organizations onboarded in 2026 now use alerting standards that would have placed them in the top 10% for strictness just six years ago. This shift proves that crypto compliance for businesses has evolved from a simple checkbox into a sophisticated engine for institutional growth. You’ve likely felt the pressure of the MiCA grandfathering period ending on July 1, 2026, or the complexity of fragmented global standards. It’s a daunting environment when you’re trying to find reliable settlement partners while avoiding regulatory fines.

We’ll show you how to master these complexities to unlock high-yield opportunities in Forex and Gold CFD trading with total confidence. This guide provides a clear roadmap for regulatory success, enabling the seamless integration of crypto and fiat systems. You’ll discover how to leverage XAUUSD CFDs and other advanced financial products to transform your commercial operations. We’re moving beyond simple survival to show you how a professional compliance framework acts as an essential component of your global evolution.

Key Takeaways

- Understand how the 2026 regulatory landscape transforms digital assets into a stable, institutional-grade foundation for global commercial operations.

- Master the essential pillars of crypto compliance for businesses to manage KYC and AML protocols with absolute confidence and precision.

- Discover the strategic synergy between deep crypto liquidity and high-yield opportunities in the XAUUSD and Forex CFD markets.

- Learn how to implement seamless infrastructure that bridges blockchain assets with traditional systems through instant crypto-to-fiat conversion.

- Identify the competitive advantages of partnering with an MSB-registered facilitator to secure long-term growth and operational reliability.

Navigating the 2026 Crypto Compliance Landscape for Global Business

The year 2026 marks a definitive end to the speculative era of digital assets. Professional entities now operate within a framework where institutional-grade digital finance is the baseline requirement. Crypto compliance for businesses has matured into a comprehensive operational strategy that encompasses tax reporting, real-time transaction monitoring, and verifiable proof of reserves. It’s no longer about simple box-ticking; it’s about building a resilient bridge between blockchain innovation and the rigorous demands of global commerce.

Companies that prioritize these standards gain access to sophisticated financial vehicles like XAUUSD and Forex CFD trading. By maintaining Money Services Business (MSB) registration, an organization signals its commitment to the highest level of regulatory excellence. This status is the gold standard for global operations, ensuring that every fiat-to-crypto conversion and high-yield trade occurs within a secure, audited environment. Blockchain transparency facilitates this by providing a permanent, immutable ledger that simplifies modern regulatory audits and eliminates the ambiguity often found in traditional systems.

The Evolution of Global Digital Asset Standards

Unified regulatory frameworks have fundamentally changed how cross-border payments function. These 2026 standards prioritize consumer protection while enabling the speed and efficiency that modern markets demand. According to the current status of Global Cryptocurrency Regulations, authorities expect businesses to maintain compliance across 180+ countries to achieve true global scale. This harmonization allows for the rapid deployment of liquidity across diverse currency corridors without the friction of outdated legacy protocols. It’s a system designed for growth, not just restriction.

Why Institutional Reliability Matters More Than Ever

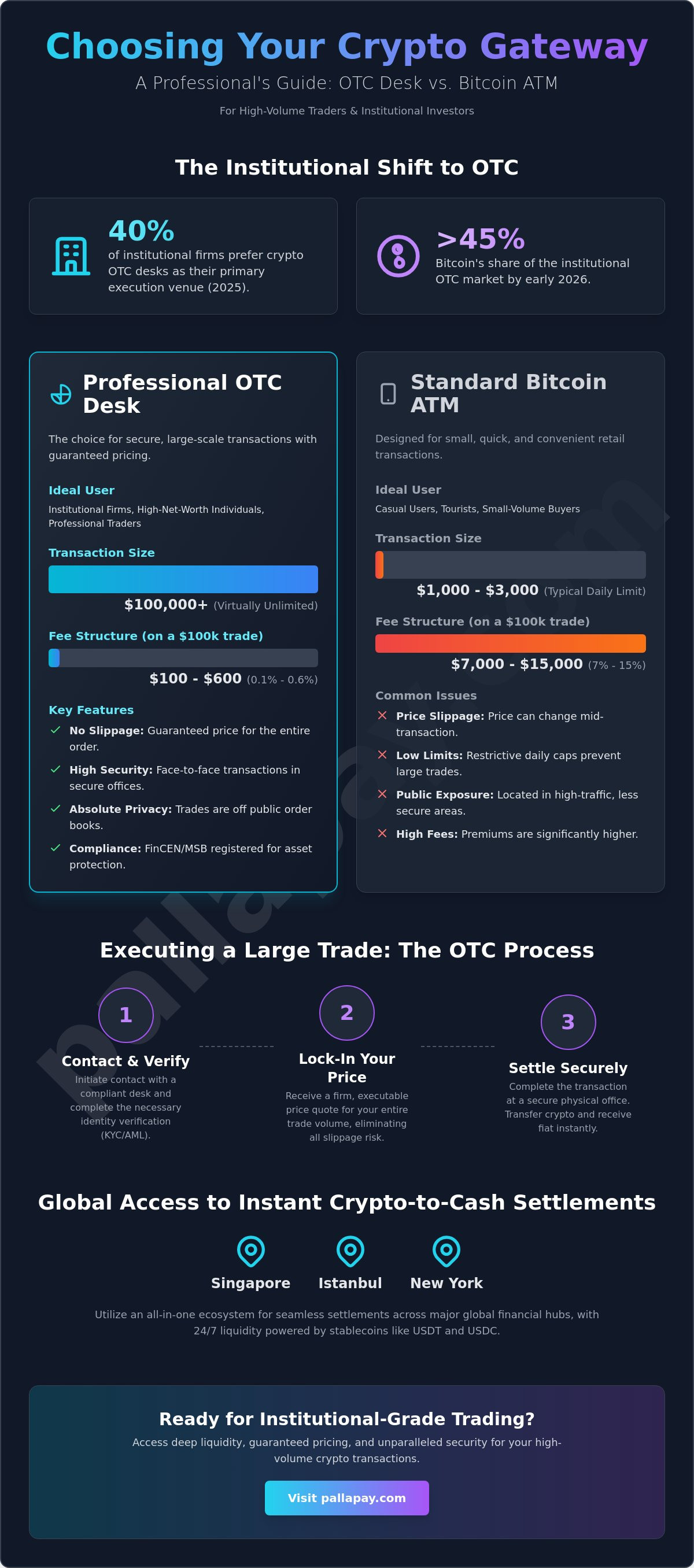

Moving from retail-focused tools to sophisticated business ecosystems is essential for firms seeking high-volume institutional partnerships. Compliance builds the absolute trust required to manage significant capital flows in the gold and USD CFD markets. In 2026, MSB registration is a mandatory requirement for any provider operating a crypto-fiat gateway, serving as a critical verification of their operational integrity. By utilizing a professional crypto offramp, businesses ensure their digital assets are converted into liquid fiat currency with total transparency and speed. This reliability transforms trading from a speculative activity into a powerful engine for financial growth.

The Structural Pillars of Institutional Crypto Compliance

Institutional excellence relies on a multi-layered defense system. Crypto compliance for businesses begins with the rigorous verification of identity and the continuous monitoring of fund flows. By 2026, the standard for professional entities has moved beyond basic checks into a proactive strategy that ensures every asset entering the ecosystem is clean and verifiable. This structural integrity is what allows firms to engage in high-volume Forex trading and gold CFD positions with absolute certainty.

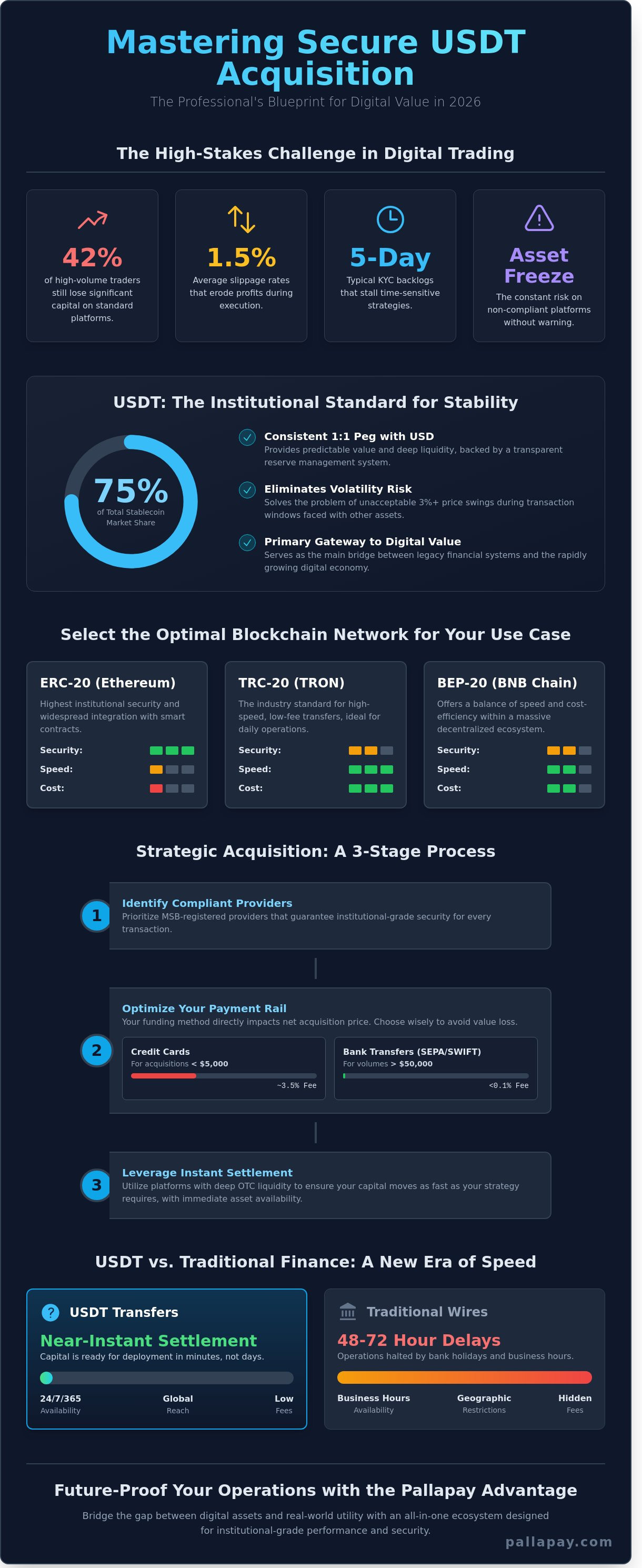

KYC protocols verify the identity of participants to prevent fraud and illicit activity. AML systems implement robust monitoring to report suspicious flows before they can compromise the integrity of the firm. These pillars create a secure environment where institutional financial reliability is the norm rather than the exception. KYT (Know Your Transaction) provides real-time on-chain analysis to ensure fund purity. It’s a technical safeguard that balances the need for total transparency with global data protection laws. This ensures that while the business satisfies regulatory audits, it also protects the privacy of its legitimate users.

Implementing Automated KYC and AML Workflows

AI-driven identity verification significantly reduces friction for professional users by accelerating the onboarding process. Modern systems set up automated risk scoring for incoming digital asset payments, allowing for immediate decision-making. Integrating secure crypto payment gateways into existing compliance stacks ensures that crypto compliance for businesses occurs in the background, maintaining a smooth user experience. This automation is essential for scaling operations without increasing manual overhead.

Blockchain Intelligence and Transaction Monitoring

Using KYT allows a business to identify the source of funds before they hit a corporate wallet. The necessity of crypto security is paramount in maintaining a clean audit trail that regulators can trust. Real-time monitoring tools provide an immediate shield by screening every incoming transaction against global watchlists to prevent any exposure to sanctioned addresses. This level of precision is the key to unlocking the transformative potential of the markets. When you operate with a compliant crypto offramp, you bridge the gap between digital innovation and fiat stability. It empowers you to focus on the financial impact of your trades, knowing the underlying mechanics are handled by a strategic partner.

How Compliance Unlocks High-Yield Forex and Gold CFD Trading

Compliance is often perceived as a restrictive burden, yet in the high-stakes world of institutional finance, it serves as the ultimate facilitator. To access the depth of the global Forex and Gold CFD markets, a firm must demonstrate an uncompromising commitment to regulatory standards. By mastering crypto compliance for businesses, you remove the friction that prevents institutional brokers from offering the high-yield leverage required for serious capital growth. This isn’t just about avoiding penalties; it’s about qualifying for the most sophisticated financial instruments available.

The synergy between digital asset liquidity and traditional currency markets represents a significant evolution in wealth management. When a business integrates compliant protocols, it creates a secure channel to deploy crypto capital into the $7.5 trillion-a-day Forex market. This bridge allows for a dynamic allocation strategy where digital assets fund active trading positions in major currency pairs and commodities, maximizing the utility of every unit of capital. It’s a professional evolution that turns compliance into a powerful engine for profit.

The Transformative Potential of CFD Trading

CFD trading acts as a powerful catalyst for financial transformation, offering the ability to generate significant returns on both rising and falling markets. For an individual or a business, mastering these markets can fundamentally alter a financial trajectory by providing exposure to global price movements without the need for physical asset ownership. The mechanics are efficient: you use digital assets to fund high-speed trading accounts, allowing for rapid execution and real-time response to market shifts. A compliant infrastructure ensures that once your strategy yields results, you can execute a seamless profit withdrawal to fiat, maintaining the liquidity necessary for ongoing operations.

Strategic Hedging with Gold and USD Pairs

Navigating the XAU/USD market remains a cornerstone of professional portfolio management because gold continues to serve as the definitive anchor of global finance. During periods of fiat volatility, trading gold CFDs provides a robust mechanism for wealth preservation and capital appreciation, effectively shielding a portfolio from inflationary erosion. Managing these gains requires a reliable system for fiat settlement, ensuring that trading profits are moved from the brokerage environment into the corporate ecosystem without delay. This integrated approach to crypto compliance for businesses ensures that your hedging strategies are supported by a foundation of institutional reliability and technical precision.

Implementing Compliant Infrastructure: From APIs to Fiat Settlement

Building a high-performance financial engine requires more than just a strategy. It demands a technical architecture that bridges the gap between decentralized assets and institutional banking. Crypto compliance for businesses is most effective when it’s invisible to the end-user but rigorous in its background execution. By automating the verification and documentation process, a business can maintain the speed necessary for global commerce while satisfying the strictest regulatory audits.

Instant crypto-to-fiat conversion is not just a convenience; it’s a requirement for operational liquidity. In the fast-moving world of XAUUSD and Forex CFD trading, capital must be mobile. Automated settlement systems reduce the friction of cross-border transactions, allowing profits to move from a digital wallet to a corporate bank account with total transparency. This infrastructure ensures that every transaction is pre-vetted, creating a permanent audit trail that reinforces your standing as a reliable institutional partner.

Leveraging APIs for Seamless Compliance

Integrating a payment API allows your business to handle complex background compliance checks without manual intervention. This automation saves significant time, shifting the focus from administrative hurdles to strategic growth. Whether you are scaling an e-commerce platform or managing high-volume institutional trades, an API-driven approach ensures that your operations remain compliant at every scale. It provides the technological answer to fragmented global standards, ensuring consistency across all currency corridors.

The Power of Efficient Off-Ramping

Ensuring your crypto off-ramp meets global MSB standards is the final piece of the regulatory puzzle. Moving trading profits securely from digital environments to traditional financial systems requires a partner that understands the nuances of crypto compliance for businesses. Instant settlement is the lifeblood of high-frequency Forex operations, where the ability to realize gains in fiat currency determines your capacity for the next high-yield position. This seamless flow of capital transforms the potential of Gold CFD trading into tangible financial success.

Accelerate your institutional growth and secure your trading profits by integrating a professional crypto off-ramp today.

Pallapay: Your Strategic Partner in Compliant Digital Asset Growth

Pallapay serves as the professional bridge between disruptive blockchain technology and institutional financial systems. By providing a comprehensive ecosystem that prioritizes crypto compliance for businesses, we enable firms to navigate the complexities of global regulation with ease. Our status as a registered Money Services Business (MSB) in both the United States and Canada offers a level of security that software-only vendors cannot match. We don’t just provide tools; we facilitate a complete financial evolution for our partners.

Our infrastructure supports a wide range of operational needs, from high-volume OTC crypto exchange services to on-the-ground retail POS solutions. This versatility ensures that whether you are settling international invoices or funding a high-leverage Forex account, the process is seamless and secure. We handle the technical conversions so you can focus on the strategic impact of your capital in the gold and USD CFD markets. It is a system designed to empower growth through reliability.

Institutional Reliability Meets Technological Innovation

Global leaders choose Pallapay because we handle the intricate background mechanics of compliance across 180+ countries. This global reach ensures that your business can scale without being hindered by fragmented local standards. Our systems provide absolute trust, allowing you to manage significant digital asset flows with the confidence of an industry leader. By integrating our solutions, you adopt a forward-thinking partner that is deeply grounded in the practicalities of modern commerce. We ensure your operations remain efficient, safe, and ready for institutional-grade expansion.

Next Steps: Accelerating Your Financial Progress

Starting your journey toward regulatory excellence is straightforward. By setting up a Pallapay wallet and accessing our merchant dashboard, you gain immediate control over your digital and fiat liquidity. This foundation is essential for anyone looking to unlock the transformative potential of Gold and Forex trading. The ability to trade XAUUSD CFDs with institutional-grade support can fundamentally change your financial trajectory, providing the growth and stability required in a digital-first economy. We invite you to join the inevitable global evolution of finance by partnering with Pallapay to secure your future in the world’s most liquid markets.

Mastering the New Standard of Global Financial Excellence

The shift toward institutional-grade digital finance is complete. By prioritizing crypto compliance for businesses, you’ve moved beyond regulatory survival to a position of market leadership. You now possess the tools to navigate the XAUUSD and Forex markets with the speed and precision required for significant financial transformation. This strategic foundation ensures that your capital remains liquid, your transactions stay transparent, and your growth remains unhindered by legacy barriers. It’s the professional gateway to a more efficient and profitable commercial future.

Success in 2026 requires a partner that combines technical innovation with institutional reliability. Pallapay provides this bridge through official MSB registration in the USA and Canada; a global presence spanning 180+ countries; and secure OTC desks for high-volume institutional trades. It is time to leverage these professional advantages to accelerate your commercial momentum. Secure your business future with Pallapay’s compliant crypto ecosystem and lead the inevitable evolution of global commerce. Your path to sustainable, high-yield trading starts with a foundation of absolute trust and technical excellence.

Frequently Asked Questions

What is crypto compliance for businesses in 2026?

Crypto compliance for businesses in 2026 is a multi-layered strategic framework that ensures every digital asset operation meets global institutional standards. It goes beyond basic identity checks to include real-time transaction monitoring and automated tax reporting. This evolution allows firms to bridge the gap between disruptive technology and financial reliability. By adopting these standards, an organization secures its position within the formal economy and gains access to high-yield investment vehicles like Forex and gold CFDs.

How does MSB registration impact a crypto company’s credibility?

MSB registration establishes a company as a verified participant in the global financial system by proving adherence to strict AML and KYC protocols. It instills absolute trust in institutional partners who require a secure bridge between digital assets and traditional banking. This registration, particularly in jurisdictions like the USA and Canada, ensures that a provider is monitored by federal authorities. It transforms a tech-centric entity into a reliable strategic partner for high-volume commercial operations.

Can I trade Gold CFDs using my business cryptocurrency holdings?

You can trade gold CFDs using business crypto holdings by leveraging a compliant payment gateway to fund your brokerage account. This process allows you to convert digital liquidity into the necessary collateral for XAUUSD positions. Using a professional facilitator ensures that the transfer of funds is documented and meets all necessary crypto compliance for businesses standards. It provides a seamless path to diversifying your corporate treasury into the world’s most stable commodity markets.

What are the main risks of non-compliance in the crypto industry?

Non-compliance carries severe risks including multi-million dollar regulatory fines, immediate suspension of operational licenses, and permanent exclusion from the traditional banking system. In a digital-first economy, failing to meet standards like the FATF Travel Rule can result in your business being blacklisted by institutional liquidity providers. These consequences don’t just stall growth; they can lead to the total collapse of an organization’s financial infrastructure. Maintaining excellence is a requirement for long-term commercial survival.

How does a crypto-to-fiat payment API simplify regulatory reporting?

A payment API simplifies regulatory reporting by automating the collection and documentation of every transaction flow in real time. It eliminates hundreds of hours of manual labor by generating pre-vetted reports that satisfy modern audit requirements. This technical integration ensures that every crypto-to-fiat conversion is recorded with precise metadata. It provides a clean audit trail that demonstrates your commitment to institutional reliability while maintaining the speed your operations demand for global scale.

What is the difference between KYC and KYT in blockchain finance?

KYC focuses on verifying the identity of the individual or entity, while KYT provides real-time monitoring of the underlying blockchain transactions. KYC prevents fraud at the point of entry, but KYT ensures the ongoing purity of funds by detecting suspicious on-chain behavior. Both are essential pillars of a robust compliance stack. Together, they create a secure environment where businesses can engage in high-volume Forex trading without exposure to sanctioned or illicit addresses.

How can I securely settle trading profits into my corporate bank account?

Securely settling trading profits requires a professional off-ramp service that offers instant conversion to fiat and direct bank transfers. This system ensures that your gains from gold or USD CFD trades are moved from the digital environment into your corporate bank account with total transparency. Using an MSB-registered provider guarantees that the settlement process adheres to international financial standards. It provides the liquidity necessary to fund ongoing operations and capitalize on new market opportunities.

Why is gold (XAU/USD) a popular choice for crypto-funded trading?

Gold remains the anchor of global finance because it provides a definitive hedge against fiat currency volatility and inflationary pressures. For firms using digital assets, the XAUUSD pair offers a way to preserve wealth while participating in the transformative potential of the markets. Trading gold CFDs allows for significant capital growth without the logistical burdens of physical ownership. It is a strategic choice for businesses seeking to stabilize their portfolios while maintaining high-yield exposure.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.