With over $2.17 billion lost to web3 security breaches by mid-2025, it’s clear that traditional methods of crypto security have reached their limit. You’ve likely mastered the art of hardware wallets and seed phrase redundancy, yet the relentless volatility of the digital market remains a constant source of anxiety. It’s a common frustration for many of the one billion global crypto owners who feel their wealth is trapped in a cycle of high-risk fluctuations without a clear path to institutional stability.

We’re here to help you bridge that gap between disruptive innovation and financial reliability. You’ll learn how to implement a comprehensive security protocol that goes beyond simple asset protection to include strategic wealth diversification. We’ll examine how transitioning digital gains into Gold and USD CFDs can transform your financial life, providing a professional offramp into traditional safe havens. This article previews a future where your digital assets aren’t just safe from hackers, but are actively shielded from market downturns through sophisticated, high-volume trading strategies.

Key Takeaways

- Learn how crypto security has evolved from passive key storage to a proactive strategy of active risk management and institutional-grade oversight.

- Discover how to utilize XAU/USD (Gold) and USD CFDs to create a professional hedge, protecting your portfolio against digital market fluctuations.

- Understand the operational benefits of transitioning high-volume transactions through regulated MSB providers and physical OTC desks for maximum stability.

- Master the mechanics of CFD trading to bridge the gap between disruptive digital assets and established commodity markets for long-term wealth preservation.

- Explore the efficiency of an integrated ecosystem that facilitates instant crypto-to-fiat conversions and professional forex account management.

The Evolving Definition of Crypto Security in 2026

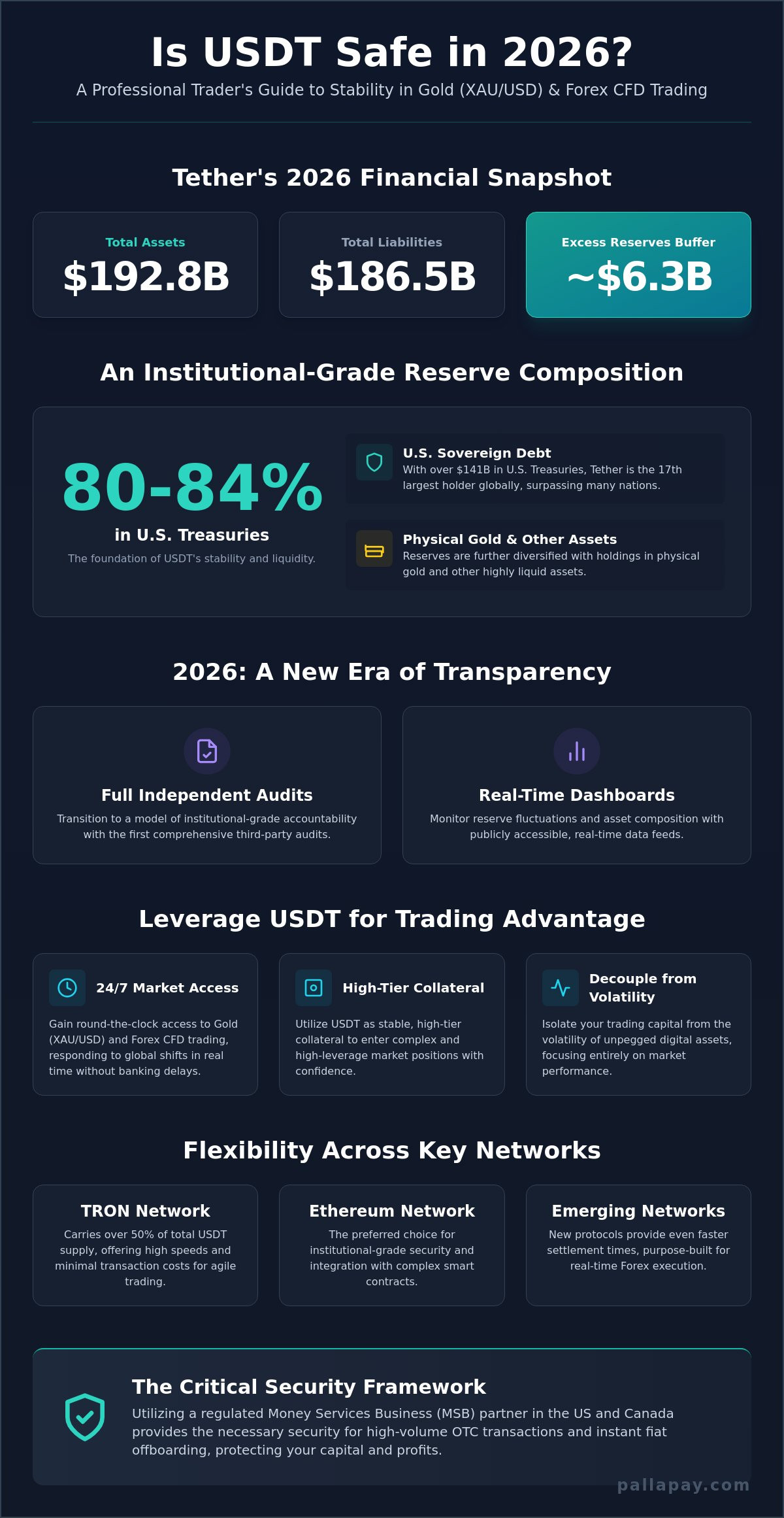

In 2026, the paradigm of crypto security has shifted from a defensive posture to a strategic operational framework. While early adopters focused almost exclusively on preventing unauthorized access to private keys, today’s professional traders recognize that protection is multi-dimensional. The influx of institutional capital has matured the market, with 76% of global institutions planning to expand their digital asset allocations this year. This maturity brings a more sophisticated threat landscape where simple hardware wallets are no longer sufficient for high-volume portfolios. Individuals now require the same institutional-grade safety nets used by major funds, utilizing regulated MSB providers to bridge the gap between digital innovation and financial stability.

The transition from passive holding to active risk management is driven by the realization that security is not a static state. It requires a supportive facilitator that can manage complex background processes while the user focuses on growth. By adopting a professional bridge that connects established practices with modern advancements, you transform your digital assets from speculative tokens into a resilient pillar of a broader financial strategy.

Network vs. Asset Security

Understanding the difference between the integrity of a blockchain and the safety of your specific holdings is vital. Public blockchains face internet-level vulnerabilities that individual users cannot control. While the network protocol might remain secure, common crypto crimes often exploit the friction between user interfaces and on-chain execution. Private key management is merely the baseline of a modern security protocol. For high-volume accounts, the finish line involves multi-layer security architectures that include:

- Multi-Party Computation (MPC): This technology eliminates single points of failure by distributing key shards across multiple secure environments.

- Segregated Institutional Custody: Assets are isolated from exchange operational funds, providing a layer of protection against platform insolvency.

- Regulated Fiat Bridges: Utilizing a secure off-ramp allows for rapid liquidation into stable currencies when network-level threats emerge.

The Financial Impact of Insecure Holdings

Security isn’t just about preventing theft; it’s about defending against the erosion of value. Market volatility acts as a persistent security threat to your net worth when assets are left stagnant in a cold state during significant downturns. The transformative potential of 2026 lies in moving from passive holding to strategic trading. By integrating digital assets with traditional markets like Gold and Forex CFDs, you create a dynamic shield. This allows you to hedge against crypto-specific crashes without exiting the financial ecosystem entirely.

Financial Crypto Security is the preservation of purchasing power.

This approach ensures that your wealth is not just “locked away” but is actively defended against both external bad actors and internal market decay. Professional-grade crypto security now demands an integrated ecosystem where your digital wallet and trading accounts work in tandem to accelerate your progress.

Institutional-Grade Protection: Beyond the Hardware Wallet

Hardware wallets provide a vital foundation for individual asset control, yet they don’t address the operational risks inherent in large-scale liquidity. Even the physical safety of the devices used to manage your keys is a factor; for example, udoq.com highlights the hidden risks of using low-quality charging stations that could compromise your hardware. In 2026, high-net-worth individuals have recognized that true crypto security requires more than just a private key; it demands the backing of a regulated institution. This shift toward Money Services Businesses (MSBs) represents a move toward institutional financial reliability. It’s about ensuring that your wealth is accessible and protected by the same legal frameworks that govern traditional finance. This professional bridge is essential for those looking to transform their digital holdings into a stable, long-term financial legacy.

The Role of MSB Registration

Registration with FinCEN in the United States and FINTRAC in Canada has become the gold standard for trust in the digital asset space. These regulatory bodies enforce strict compliance standards that protect users from the exchange-level insolvency seen in previous market cycles. When you operate within a Pallapay secure ecosystem, you’re interacting with a platform that must adhere to rigorous auditing and proof-of-reserve requirements. Following official government advice on avoiding cryptocurrency scams is much simpler when your partner is a regulated entity. This compliance ensures that your assets are segregated and your transactions are transparent, providing a safety net that anonymous, unregulated exchanges simply cannot offer.

Physical Presence as a Security Feature

Digital-only platforms often lack the accountability required for institutional-grade operations. Global physical offices build a level of reliability that software alone cannot replicate. Face-to-face OTC transactions significantly reduce the risks associated with peer-to-peer scams, where fraudulent activity is often masked by digital anonymity. By using physical off-ramp solutions, you can manage high-volume liquidations with the confidence of a global industry leader. This physical infrastructure bridges the digital gap, making complex technical conversions feel like standard, effortless business operations. It’s a supportive facilitator for those who require absolute certainty when moving large sums of capital.

Security also means protecting your net worth from the hidden erosion of opaque pricing. Transparent fee structures prevent the “slippage” and “hidden spread” costs that often plague unregulated brokers. Regulated payment gateways protect both merchants and consumers by facilitating real-time settlement and verified processing. If you are looking to accelerate your progress, consider how a secure fiat settlement can streamline your path from digital assets to tangible wealth. This integrated approach ensures that every sentence of your financial story is written with clarity and security.

Diversification as Security: Gold and Forex CFDs

True crypto security in 2026 has expanded to encompass the protection of your total net worth against market volatility. While previous sections focused on the necessity of institutional crypto custody to prevent theft, financial security requires a proactive strategy to mitigate the inherent risks of digital asset cycles. Stagnant holdings are vulnerable holdings. By integrating your digital portfolio with traditional commodity and currency markets, you transform a stationary asset base into a dynamic wealth engine. This evolution from simple storage to strategic diversification is what separates retail participants from institutional-grade investors.

Strategic trading isn’t just about seeking higher returns; it’s about creating a resilient financial foundation. When digital markets face downward pressure, the ability to pivot into established safe havens ensures that your purchasing power remains intact. This approach allows you to maintain your market position while shielding your capital from the erratic swings that characterize the emerging tech sector.

The Power of XAU/USD in a Digital Portfolio

Gold remains the ultimate historical security asset, and its pairing with the US Dollar (XAU/USD) provides a critical hedge for crypto holders. In 2026, we see a growing correlation between Bitcoin and Gold during periods of global economic uncertainty, as both are viewed as hedges against traditional fiat inflation. Trading Gold CFDs offers a significant efficiency advantage over holding physical bullion. You gain the price exposure and security of the precious metal without the friction of physical storage, transport, or insurance costs. This real-time liquidity is essential for those who need to move capital quickly between digital assets and stable commodities to preserve their wealth.

Forex CFDs: Managing Global Currency Risk

Forex trading can change your financial life by providing a level of consistent liquidity that digital-only portfolios often lack. By leveraging USD pairs, you can stabilize your total portfolio value even when your crypto holdings are underperforming. Sophisticated risk management involves using leverage not as a speculative tool, but as a way to maximize capital efficiency. This allows you to control larger positions with less upfront capital, freeing up your remaining assets for other strategic moves.

Contracts for Difference (CFDs) are particularly powerful because CFDs allow for profit in both rising and falling markets. This means you don’t have to wait for a “bull run” to grow your net worth. Whether the market is trending upward or facing a correction, you have the tools to protect your gains and capitalize on price movements. This flexibility is a cornerstone of modern crypto security, ensuring that your financial progress remains steady regardless of broader market sentiment.

Practical Steps to Secure and Grow Your Wealth

Transitioning from basic asset protection to a sophisticated wealth strategy requires a structured approach. In 2026, crypto security is defined by how effectively you can move between highly volatile digital assets and stable traditional markets. The first step involves establishing a reliable bridge between your digital wallet and a professional trading environment. This connection ensures that you aren’t just storing value, but actively managing it through real-time market access. By integrating these systems, you eliminate the friction that often leads to missed opportunities or exposure during market corrections.

A critical component of this workflow is the ability to lock in gains instantly. Utilizing a secure fiat settlement system allows you to convert digital profits into USD or other stable currencies without leaving the institutional ecosystem. This process protects your purchasing power from the sudden “flash crashes” that still occur in the crypto space. Monitoring your global exposure through an integrated dashboard provides the clarity needed to make informed decisions, ensuring that your net worth is balanced across both emerging and established asset classes.

Setting Up Your Strategic Hedge

Effective diversification isn’t about random allocation; it’s about following a “Safe Haven” model. For many professional traders in 2026, this means allocating 20% to 30% of their digital portfolio into Gold (XAU/USD) and USD CFDs. Identifying entry points for Gold requires a calm, utility-focused analysis of global currency trends. You can streamline this process by using advanced payment APIs to automate the flow of wealth between your exchange accounts and trading platforms. This automation accelerates your progress, allowing you to respond to market shifts with the speed of a global industry leader.

Risk Management Tools for CFD Trading

Trading CFDs offers transformative potential, but it demands institutional-grade discipline. Implementing strict stop-loss orders is the technological answer to the problem of market unpredictability. This tool automatically closes positions at a predetermined price, ensuring that a single market swing doesn’t compromise your entire portfolio. The shift from a passive “HODL” mindset to an active institutional trading perspective is what truly changes your financial life. It empowers you to view market movements not as threats, but as opportunities for growth.

You should review your crypto security posture quarterly. The threat landscape evolves quickly, and a supportive facilitator will help you stay ahead of new risks. If you’re ready to secure your financial future, you can start your institutional journey today by exploring our comprehensive off-ramp and trading solutions. This logical, step-by-step progression ensures that your wealth remains protected, liquid, and poised for expansion.

The Pallapay Bridge: Your Partner in Secure Evolution

Pallapay serves as the definitive bridge between disruptive digital assets and institutional financial reliability. By facilitating a seamless transition from decentralized networks to global currency markets, we empower you to manage your wealth with absolute confidence. This isn’t just about providing tools; it’s about offering a comprehensive, integrated ecosystem that handles complex background processes so you can focus on strategic growth. With an operational presence in 180 countries, we’ve established ourselves as a global industry leader that connects modern advancements with established commerce. Our platform is the technological answer to the operational needs of professional and individual users alike.

A Unified Financial Ecosystem

True crypto security is achieved when your assets are part of a liquid, transparent, and regulated environment. Integrating the Pallapay Wallet into your daily operations connects you directly to global commerce. You’re no longer restricted by the friction of traditional banking delays or the uncertainty of unregulated platforms. The Pallapay Mastercard allows you to spend your gains instantly, transforming digital value into real-world purchasing power with incredible speed. Since our founding in 2018, we’ve maintained a relentless focus on safety and utility, ensuring that every transaction mirrors the real-time nature of the markets it facilitates. This reliability provides a secure destination for all your technical and financial needs.

Start Your Transformation

Securing your financial future requires a partner that understands the mechanics of high-volume transactions and institutional-grade oversight. Opening a professional account for OTC trading is the logical first step toward sophisticated wealth management. This is not a rebel stance against traditional systems; it’s a forward-thinking strategic partnership designed to empower your progress. Our infrastructure provides the necessary stability for Gold and Forex CFD setups that can fundamentally change your financial life. We handle the technical integrations so that your focus remains on market opportunities and capital preservation.

We invite you to view the institutional guide to OTC to understand how high-volume trading integrates into a broader crypto security framework. By adopting these professional solutions, you accelerate your own progress and move beyond simple asset protection. The evolution of your digital wealth starts with a logical, step-by-step progression into global commodity and currency markets. Your journey toward strategic wealth diversification is supported by a regulated MSB that prioritizes stability, efficiency, and your long-term success in an inevitable global evolution.

Securing Your Financial Legacy in a Global Market

Mastering crypto security is no longer a matter of simple key management; it’s the strategic integration of digital wealth into stable, global markets. The transition into Gold and USD CFDs provides a professional hedge that preserves your purchasing power during market cycles. This shift from passive holding to active institutional trading is what fundamentally changes your financial life. It empowers you to view market movements as opportunities rather than threats.

Pallapay stands as your reliable partner in this evolution. Regulated as an MSB in both the US and Canada, we’ve provided secure infrastructure to users in over 180 countries since 2018. Our institutional-grade OTC infrastructure and seamless fiat settlement systems ensure your high-volume operations are effortless and safe. We handle the complex background processes so you can focus on accelerating your progress.

Secure your assets and start trading Gold CFDs with Pallapay today.

Step into the future of commerce with a partner that prioritizes your stability and growth. Your financial transformation starts now.

Frequently Asked Questions

What is the most secure way to store crypto for high-volume traders?

High-volume traders should utilize institutional-grade custody solutions that combine multi-party computation (MPC) with a regulated MSB bridge. While hardware wallets are a baseline, professional crypto security in 2026 requires the liquid protection provided by physical OTC desks and regulated ecosystems. This approach eliminates single points of failure while maintaining the operational speed required for large-scale market execution and wealth preservation.

How does CFD trading help in securing my crypto portfolio?

CFD trading secures your portfolio by providing a professional hedge against market downturns without requiring you to exit the digital ecosystem entirely. It allows you to profit from falling prices, effectively shielding your total net worth from extreme volatility. This active risk management transforms a stagnant portfolio into a dynamic wealth engine, ensuring your purchasing power remains intact regardless of broader market sentiment.

Is Gold (XAU/USD) still a good hedge for crypto in 2026?

Gold remains a premier safe-haven asset in 2026, offering a historical counterweight to the erratic swings of digital asset cycles. Trading XAU/USD via CFDs is significantly more efficient than holding physical bullion because it provides real-time liquidity and eliminates storage friction. This allows you to rebalance your holdings instantly as market conditions shift, providing a stable foundation for your broader financial strategy.

Why is MSB registration important for my security?

MSB registration in the US and Canada ensures that a provider adheres to strict anti-money laundering (AML) and proof-of-reserve standards. This regulatory compliance protects users from exchange-level insolvency and the operational risks found on anonymous platforms. It provides a legal safety net and institutional reliability, ensuring that your assets are handled by a supportive facilitator that meets global industry standards for safety.

Can I spend my crypto gains directly on traditional markets?

You can spend your gains directly through integrated solutions like the Pallapay Mastercard or instant fiat settlement services. These tools act as a professional bridge between digital profits and traditional commerce. It allows for the effortless conversion of digital assets into global spending power, ensuring that your wealth is as liquid as it is secure in your daily financial life.

How do I protect my private keys while actively trading CFDs?

The most effective strategy is to keep the majority of your assets in segregated institutional custody while using a regulated bridge to fund your trading account. This separation ensures that your primary wealth remains offline and secure while you interact with the CFD market. It limits your digital exposure only to the specific capital you have allocated for active trading and strategic growth.

What are the common crypto security threats for businesses in 2026?

Businesses currently face sophisticated social engineering and supply chain vulnerabilities that target the friction between digital wallets and fiat systems. With over $2.17 billion lost to web3 security incidents by mid-2025, robust crypto security now requires multi-layer protocols. Regulated institutional bridges are essential to mitigate these risks, providing a secure destination for high-volume operations that anonymous, decentralized platforms simply cannot offer.

How does Pallapay ensure the security of large OTC transactions?

Pallapay secures large OTC transactions through a combination of physical desks in major financial hubs and a regulated MSB framework. Face-to-face interactions eliminate the risks of P2P scams and digital anonymity that often plague large liquidations. This institutional-grade infrastructure ensures that every transaction is transparent, verified, and handled with the confidence of a global industry leader focused on absolute stability.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.