The most successful traders in 2026 no longer view digital assets as an isolated ecosystem; they see them as high-velocity fuel for traditional commodity markets. If you’ve struggled with high slippage on large trades or felt drained by hidden fee structures, you’re not alone. Friction limits growth. We understand that your goal isn’t just to exit a position, but to rotate capital with precision. Mastering a professional crypto to fiat exchange is the essential first step toward this institutional level of agility.

This guide will help you master the technical mechanics required to unlock elite trading opportunities in gold and forex markets. By establishing a reliable bridge to fiat, you can access XAUUSD and USD CFDs with the speed and security your portfolio demands. We’ll explore how to achieve instant liquidity and low-cost conversion while navigating the 2026 regulatory landscape, including MiCA and CARF requirements. You’re about to transform your digital gains into a diversified financial legacy through strategic commodity trading and sophisticated market participation.

Key Takeaways

- Master the technical mechanics of a modern crypto to fiat exchange to ensure seamless capital rotation between digital assets and traditional markets.

- Identify the most efficient off-ramp solutions by distinguishing between automated liquidity pools and professional Over-the-Counter (OTC) desks for high-volume transactions.

- Optimize your trading margins by decoding hidden spreads and selecting transparent fee structures that align with institutional financial standards.

- Capitalize on the 24/5 liquidity of the forex market to trade XAUUSD and USD CFDs, transforming digital gains into diversified commodity positions.

- Implement a secure, regulated strategy for global liquidity that integrates professional conversion tools with immediate spending capabilities.

Navigating the Crypto to Fiat Exchange Landscape in 2026

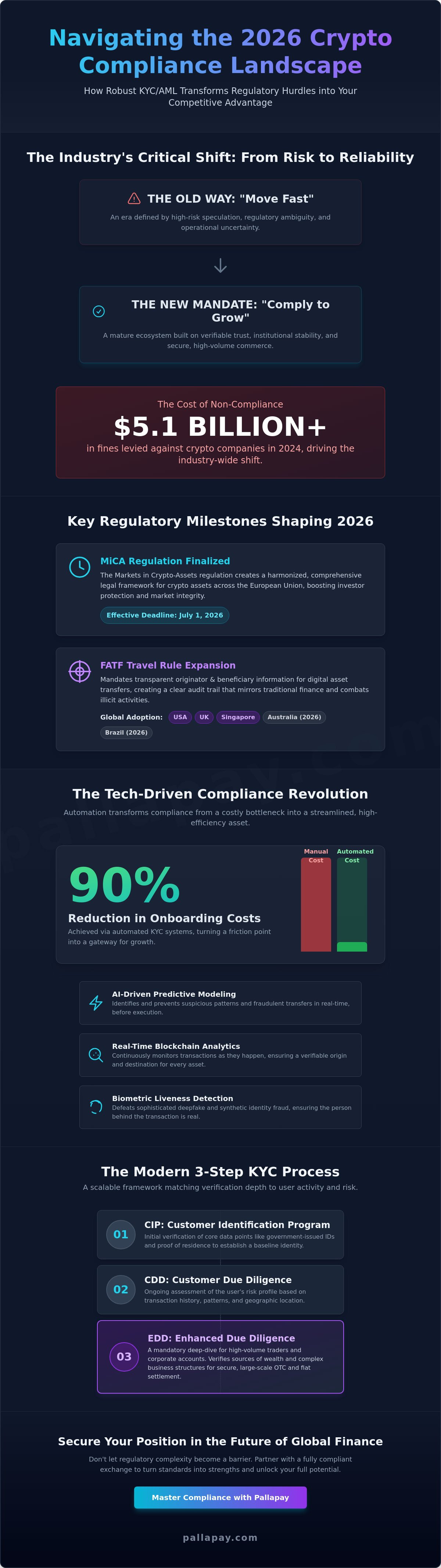

By July 2026, the global cryptocurrency market is valued at approximately $3.6 trillion. This massive scale has shifted the focus for serious investors from simple speculative holding to sophisticated capital management. Professional traders no longer view their portfolios as static digital vaults. Instead, they utilize a high-performance crypto to fiat exchange to facilitate rapid entries into traditional markets. This evolution turns digital volatility into a tactical bridge for high-leverage opportunities in gold and forex. A comprehensive cryptocurrency exchange overview reveals how these platforms have transitioned from niche tech experiments into the backbone of global finance, providing the necessary infrastructure for this inevitable evolution. As the CAGR for exchange platforms holds steady at 25.6%, the need for institutional-grade utility has replaced the era of simple retail curiosity.

Liquidity as a Strategic Advantage

Instant access to fiat currency acts as a shield against market instability. When gold prices fluctuate or USD pairs offer high-yield CFD opportunities, the ability to convert assets immediately is the difference between profit and missed potential. High-volume traders use a professional crypto off-ramp to move from digital tokens to tangible liquidity without the friction of traditional banking delays. This agility allows for real-time response to XAUUSD trends, where a single hour of delay can erode a position’s value. Beyond preservation, this liquidity empowers you to engage in USD CFD trading, a path that has historically transformed individual financial trajectories by providing access to the world’s most liquid currency markets. Capital rotation is the primary driver of modern wealth creation.

The 2026 Regulatory Environment

The 2026 landscape is defined by institutional-grade oversight. Regulations like the EU’s MiCA framework are now fully operational, mandating transparent fee structures and asset segregation. For an investor, security isn’t a luxury; it’s a prerequisite for growth. Choosing a partner with MSB registrations in the US and Canada provides the legal certainty required for large-scale operations. These compliant structures protect your capital while ensuring that every transaction meets global tax and reporting standards like CARF, which began requiring data collection in January 2026. Reliability is the new gold standard in an industry that demands both speed and absolute regulatory adherence. By aligning with a regulated bridge, you ensure your transition to fiat is both secure and permanent, allowing you to focus on market strategy rather than operational risk.

The Mechanics of Modern Crypto Off-Ramps

A crypto off-ramp is a service that facilitates the exchange of digital assets for government-issued currency. It acts as the technical bridge between a decentralized ledger and the traditional banking system. For the modern investor, this isn’t just a way to cash out; it’s a vital tool for capital rotation. While retail users often depend on automated liquidity pools, these systems can struggle with high slippage on larger orders. Professional traders instead utilize an OTC crypto exchange to execute trades at a fixed price. This method bypasses public order books, ensuring that a large sell order doesn’t negatively impact the market price or alert other participants to your strategy.

When moving significant capital, security is the foundation of every transaction. Understanding the best practices for avoiding cryptocurrency scams ensures your assets remain protected during the sensitive conversion phase. Once the trade is executed, fiat settlement rails handle the final transfer. These rails represent the technical pathways that connect blockchain addresses to traditional financial institutions. They manage the complex transition from cryptographic proof to standard bank ledger entries, ensuring that your crypto to fiat exchange is both rapid and compliant with global standards.

OTC Desks for High-Volume Conversion

High-net-worth individuals prioritize OTC desks because they offer personalized service and minimal price slippage. Unlike public exchanges where large trades are visible to the entire market, OTC transactions remain private. This confidentiality is vital for maintaining market stability and personal security. A dedicated broker manages the process, providing a single price for the entire block of assets. This level of institutional reliability is essential for those rotating significant capital into USD or gold-backed positions to fund advanced trading strategies.

Instant Liquidity via Crypto Mastercards

For many, the ultimate goal is the ability to use gains in real-time. A Pallapay Mastercard bridges this gap by allowing you to spend converted fiat instantly at millions of locations worldwide. These cards function as a direct link to your digital wealth, bypassing the multi-day wait times associated with traditional bank wires. Whether you’re funding a high-leverage forex account or managing daily operational costs, a virtual or physical card provides unmatched speed. If you want to streamline your exit strategy, exploring a professional crypto off-ramp can significantly enhance your operational efficiency and financial agility.

Evaluating Exchange Fees, Spreads, and Security

High-performance trading requires more than just market insight; it demands a precise understanding of the costs associated with capital rotation. When executing a crypto to fiat exchange, the headline fee is rarely the total cost. Savvy investors look deeper into the architecture of the transaction to identify where value might be eroded. This level of scrutiny is essential for those moving significant volume into USD CFD or gold positions, where even minor friction can impact the transformative potential of a trade. Professional platforms prioritize transparency, allowing you to calculate net returns with institutional accuracy.

Efficiency in conversion is often a choice between commission-based and spread-based models. Commission models charge a flat or percentage-based fee on top of the market price, while spread-based models integrate the cost into the asset price itself. Identifying which model suits your volume is a critical step in understanding cryptocurrency and blockchain as a tool for wealth management. Beyond these primary costs, you must also account for withdrawal friction and network fees. These background expenses can accumulate during periods of high network congestion, making the timing of your off-ramp as important as the trade itself.

The Real Cost of Conversion

Determining the true price of liquidity requires a holistic view of the exchange environment. The spread is the difference between the buy and sell price of an asset. While “zero-fee” claims often attract retail attention, they frequently hide wider spreads that result in a higher total cost for large transactions. Professional-grade partners eliminate this ambiguity by providing real-time data and direct access to deep liquidity pools. This clarity ensures that your capital remains intact as it transitions from digital volatility to the stability of fiat currency.

Security Protocols for Fiat Settlements

Institutional reliability is built on a foundation of rigorous security and regulatory compliance. MSB registration in the US and Canada isn’t just a legal requirement; it’s a signal of absolute trust for global investors. Utilizing a professional fiat settlement service ensures that your assets are protected by 2FA, cold storage, and multi-signature protocols throughout the conversion process. These platforms maintain high KYC and AML standards to prevent fraud and ensure that every dollar reaching your bank account is fully compliant. Protecting your assets during the transit from a digital wallet to a traditional bank account is the final, most critical step in securing your financial future. By choosing a partner that prioritizes these standards over market hype, you create a secure bridge to the high-leverage opportunities found in gold and forex markets.

Leveraging Fiat for Gold and Forex CFD Trading

The transition from digital assets to traditional markets marks the evolution of a retail trader into a sophisticated global investor. Converting digital gains is only the beginning of a broader wealth management strategy. By utilizing a professional crypto to fiat exchange, you bridge the gap between speculative digital growth and the disciplined environment of Contract for Difference (CFD) trading. This strategic rotation allows you to move capital with institutional precision. Unlike the spot crypto market where you’re limited to the assets you physically hold, CFD trading provides access to leverage. This financial tool enables you to control larger positions in gold or major currency pairs with a smaller initial capital outlay, significantly amplifying the transformative potential of your original digital gains.

The ability to rotate capital quickly is what separates elite traders from the rest of the market. When you unlock fiat liquidity, you’re no longer restricted by the boundaries of a single asset class. You gain the power to respond to global economic shifts in real time. This agility can fundamentally change your financial life, providing a path to consistent returns that are independent of the crypto market’s specific cycles. To begin your transition into these high-performance markets, you can convert crypto to fiat instantly through our secure off-ramp infrastructure.

The Power of Forex Markets

Forex markets offer a level of liquidity that remains unmatched, operating on a 24/5 cycle that aligns with the lifestyle of a modern investor. Accessing major USD currency pairs requires a stable fiat base, which is why a reliable conversion strategy is essential. Moving from volatile tokens into liquid fiat allows you to engage with the forex market’s consistent price movements. Professional traders use this environment to generate reliable returns, using the stability of government-issued currencies to balance the high-risk nature of their digital portfolios. This steady engagement with global currency markets provides a foundation for long-term financial security.

Gold as the Ultimate Hedge

Gold remains the definitive hedge against global inflation and economic uncertainty. When crypto markets experience high-frequency volatility, many investors rotate into XAU/USD pairs to preserve their purchasing power. This isn’t just a defensive move; it’s about building a resilient portfolio that combines modern innovation with historical reliability. By converting crypto to fiat, you gain the agility to enter the gold market the moment a hedge becomes necessary. This strategic move ensures your digital profits are anchored in a tangible commodity that has served as a benchmark for value for centuries, protecting your wealth from the erosion of inflation.

Pallapay: Your Professional Bridge to Global Liquidity

Achieving absolute financial agility in 2026 requires more than just a platform; it demands a strategic partner that understands the nuances of institutional capital. Pallapay serves as this definitive destination. By integrating a high-performance crypto to fiat exchange with regulated settlement rails, we provide the stability necessary for high-stakes market participation. Our ecosystem is built on a foundation of trust, holding MSB registrations in the US and Canada to ensure your operations meet the highest global standards. Whether you’re a professional trader rotating into USD CFDs or a business managing international e-commerce flows, our infrastructure handles the technical complexity so you can focus on growth.

We operate in over 180 countries, providing a truly global off-ramp for digital wealth. This presence allows us to offer direct fiat settlement for merchants and individuals alike, bypassing the friction often found in fragmented financial systems. We don’t just facilitate transactions; we empower you to transform digital innovation into tangible, diversified power. By bridging the gap between blockchain technology and traditional finance, we provide the tools required to master the gold and forex markets with confidence. Reliability is the core of our mission, ensuring that your transition to fiat is as secure as it is rapid.

Tailored Solutions for Individuals and Businesses

High-volume traders require a level of reliability that public exchanges cannot provide. Our OTC desks are designed for institutional-grade conversion, offering fixed pricing and deep liquidity for significant capital movements. The Pallapay Wallet acts as your secure hub, allowing you to manage digital assets with the same precision you’d expect from a private bank. For those managing complex cross-border settlements, our dedicated support team ensures that every fiat transfer is executed with speed and absolute regulatory adherence. This personalized approach ensures your liquidity needs are met without compromise.

Getting Started with Pallapay

The transition to a sophisticated trading life begins with a streamlined onboarding process. We’ve designed our professional client intake to be efficient, moving you from registration to active trading without unnecessary delays. Businesses can integrate our Payment API to automate their financial flows, creating a seamless connection between crypto receipts and fiat liquidity. Taking this first step allows you to unlock the high-leverage opportunities found in gold and forex CFDs. It’s time to move beyond speculative holding and embrace a future where your digital assets serve as the foundation for a diversified, resilient financial legacy.

Mastering the Future of Global Capital Rotation

The transition from passive digital holding to active market participation is the defining strategy for 2026. You’ve seen how a high-velocity crypto to fiat exchange acts as the essential bridge to the high-leverage world of USD and gold CFD trading. By mastering these mechanics, you transform digital volatility into a versatile tool for wealth preservation and growth. Success in the forex and commodity markets requires both tactical speed and institutional-grade security to ensure your capital is always positioned for the next opportunity.

Since 2018, Pallapay has been redefining institutional crypto services by providing a secure, regulated bridge to traditional finance. With MSB registrations in the US and Canada, we serve professional traders across 180+ countries with absolute reliability. You don’t have to manage these complex background processes in isolation. Secure your global liquidity with Pallapay’s professional exchange services today. By aligning with a strategic partner, you’re ready to unlock a new standard of financial agility and build a resilient legacy in the global markets.

Frequently Asked Questions

What is the fastest way to exchange crypto to fiat in 2026?

The fastest method is utilizing a professional off-ramp that offers instant conversion and direct bank settlements. Professional OTC desks provide a streamlined path for high-volume traders, ensuring that liquidity is available without the delays common in retail order books. By using an integrated ecosystem, you can move from digital assets to spendable fiat in a matter of minutes, allowing for rapid capital rotation into traditional markets.

How do exchange spreads affect the final amount of fiat I receive?

The spread represents the difference between the market price and the price at which the exchange executes your trade. A wider spread means you receive less fiat for your digital assets, which can be a significant hidden cost during a large crypto to fiat exchange. Professional platforms offer tighter spreads and transparent pricing, ensuring that your net capital remains as high as possible when transitioning into high-leverage positions like gold CFDs.

Is it safe to use an OTC desk for large cryptocurrency conversions?

Utilizing a regulated OTC desk is the safest method for executing high-volume conversions because it provides privacy and eliminates price slippage. These desks operate outside of public order books, preventing your trade from moving the market against your position. When you partner with a provider holding MSB registrations in the US and Canada, you gain the institutional-grade security and regulatory certainty required for substantial capital movements.

Can I spend my converted fiat immediately using a crypto card?

Yes, a Mastercard solution allows you to spend your converted gains at millions of locations globally the moment the transaction is confirmed. These cards use real-time settlement technology to bridge your digital wealth with everyday commerce. This immediate liquidity is essential for traders who need to manage operational costs or fund new opportunities in the forex market without waiting for traditional bank wire cycles.

What are the tax implications of converting crypto to fiat?

As of 2026, global tax reporting frameworks like CARF and DAC8 require exchanges to report transaction data to relevant authorities. Converting digital assets to fiat is typically a taxable event in most jurisdictions, and you must maintain accurate records for annual filings. It’s essential to consult with a qualified tax professional to ensure your trading activities remain compliant with the evolving regulatory standards in your specific region.

Why should I use fiat liquidity to trade gold or forex CFDs?

Fiat liquidity provides the gateway to the world’s most liquid markets, offering 24/5 trading and access to institutional leverage. Trading gold and USD CFDs allows you to hedge against digital market volatility and diversify your portfolio with tangible commodities. This rotation can fundamentally change your financial life by providing a path to consistent returns through the sophisticated mechanics of the global forex market.

What regulatory registrations should a crypto to fiat exchange hold?

A reliable crypto to fiat exchange should maintain Money Services Business (MSB) registrations with agencies like FinCEN in the US and FINTRAC in Canada. In 2026, compliance with the EU’s MiCA regulation is also a critical indicator of institutional reliability. These registrations ensure the platform follows strict anti-money laundering (AML) and know-your-customer (KYC) protocols, protecting your assets from fraud and legal risk.

How does Pallapay ensure the security of my fiat settlement?

Pallapay utilizes a multi-layered security architecture that includes cold storage for digital assets and multi-signature authorization for all settlements. Our platform is grounded in regulatory compliance, holding active MSB registrations to provide a secure bridge between disruptive tech and traditional finance. By combining 2FA protocols with direct fiat settlement rails, we ensure your capital moves safely from your digital wallet to its final destination.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.