With over 700 million people worldwide owning digital assets as of January 2026, the shift from niche experiment to global standard is officially complete. You’ve likely felt the persistent sting of traditional payment processors taking a significant chunk of your international margins or the frustration of waiting days for a B2B settlement to clear. These inefficiencies are more than just a nuisance; they’re a barrier to the liquidity you need to scale your operations in a volatile economy. It’s time to bridge that gap.

This article details how the core benefits of accepting cryptocurrency extend far beyond simple payment processing. You’ll discover how moving to digital assets slashes operational costs and unlocks high-growth financial opportunities in Gold and Forex CFD markets. We’ll examine the strategic path from receiving instant settlements to leveraging that liquidity for XAU/USD and currency trading. By the end, you’ll understand how to transform your business from a passive payment receiver into an active participant in global financial markets, using your crypto holdings to drive transformative growth.

Key Takeaways

- Learn how the operational benefits of accepting cryptocurrency include reducing transaction fees to below 1% and achieving near-instant settlement.

- Discover how to leverage merchant liquidity to access high-growth opportunities in Gold (XAU/USD) and Forex CFD markets.

- Understand the shift from traditional banking bottlenecks to a 24/7 digital economy that prioritizes speed and efficiency.

- Identify the critical role of regulated MSB partnerships and Payment APIs in maintaining a secure and compliant financial infrastructure.

- Gain insights into transforming stagnant balances into active capital that drives long-term financial growth and stability.

The Evolution of Business Payments: Why Crypto is Essential in 2026

The global economy has undergone a fundamental transformation. In 2026, decentralized finance is no longer a peripheral concept; it’s the core infrastructure for modern commerce. Traditional banking rails often act as a bottleneck for companies operating in a 24/7 marketplace. These legacy systems rely on clearing houses and manual reconciliations that can stall international business for days. In contrast, cryptocurrency is a programmable asset that facilitates instant settlement through automated protocols. For international merchants, moving beyond legacy systems isn’t just an upgrade. It’s a competitive necessity to maintain liquidity in a fast-moving market.

One of the primary benefits of accepting cryptocurrency is the ability to bypass the friction inherent in old-world finance. By adopting digital payment structures, you align your business with the real-time requirements of global trade. This alignment is particularly vital if you intend to transition your merchant capital into high-growth sectors like Forex or Gold CFD trading. When your revenue is settled instantly, you can pivot that capital into the XAU/USD market or major currency pairs without waiting for a bank’s permission.

The Global Reach of Digital Assets

Digital assets remove the geographic barriers that once limited retail and e-commerce expansion. Traditional cross-border transactions require a chain of intermediary banks, each extracting a fee and adding delay. By using a sophisticated API for Crypto Payments, a merchant can access customers in over 180 countries without needing a local bank account in every region. This direct connectivity ensures that your revenue isn’t eroded by currency conversion spreads or third-party handling costs. It’s about creating a frictionless path for global capital to flow directly into your business accounts.

The Security Advantage of Blockchain

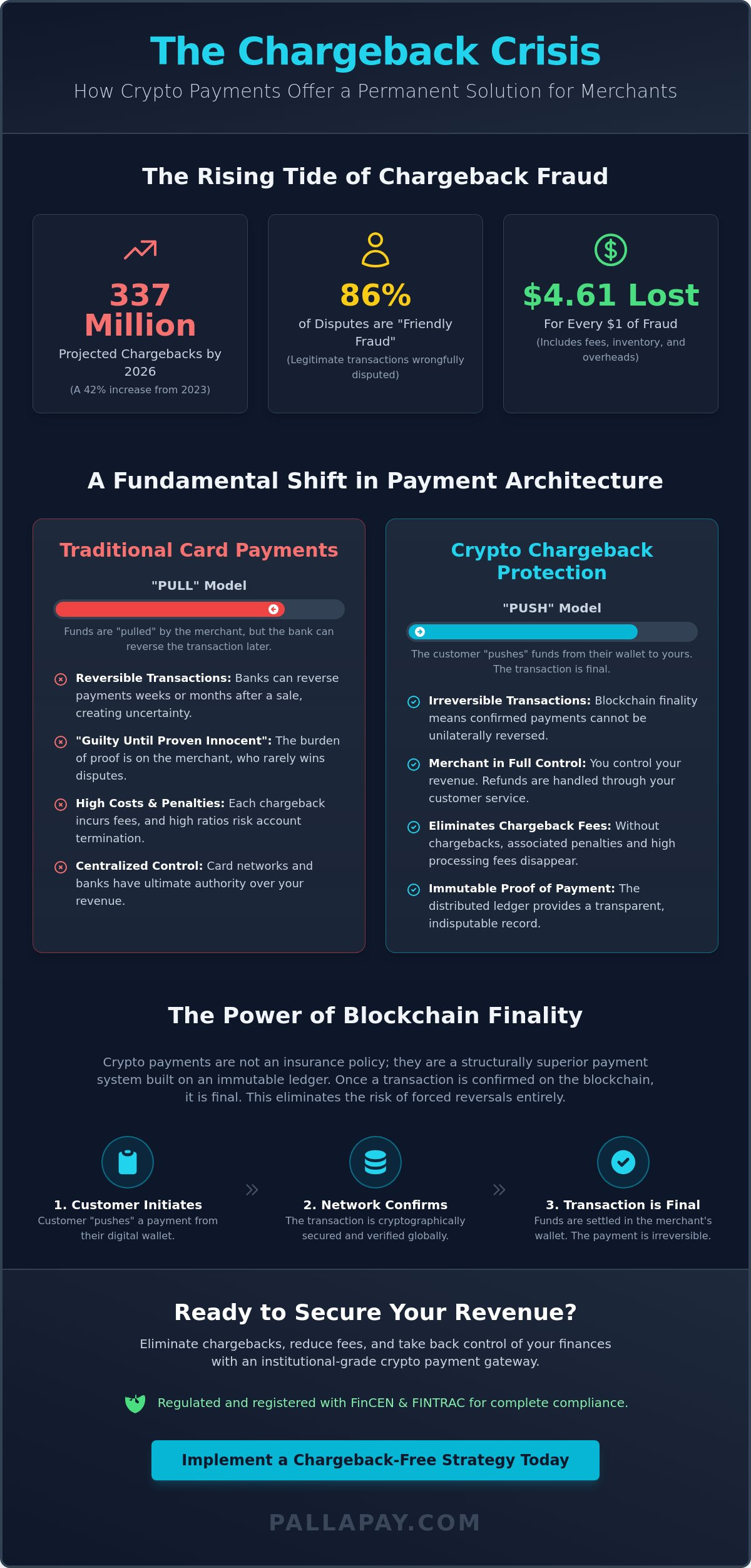

Security remains a cornerstone of the history of cryptocurrency and its eventual institutional adoption. Unlike traditional credit card payments, blockchain transactions are immutable. This means once a payment is confirmed on the ledger, it cannot be reversed by the customer through a fraudulent chargeback. This transparency provides a level of certainty that opaque banking systems cannot match. Merchants can choose between self-custody for total control or managed gateway security for a hands-off, professional experience. This secure foundation allows you to focus on strategic growth, such as diversifying your settled fiat into USD CFD positions or gold trading, rather than managing payment disputes. The transition to blockchain-based payments provides the institutional-grade stability required to scale in 2026.

Core Operational Benefits: Fees, Speed, and Efficiency

Operational efficiency defines the winners of the 2026 global economy. One of the most immediate benefits of accepting cryptocurrency is the drastic reduction in transaction overhead. Traditional credit card processors frequently charge between 3% and 5% per transaction, a figure that becomes prohibitive as business volume scales. In contrast, crypto-based transaction costs typically remain below 1%. This difference represents a significant boost to net profit margins, allowing for more aggressive reinvestment strategies. By cutting out the multiple intermediary banks involved in traditional rails, you retain a larger portion of every sale.

Beyond the base percentage, traditional finance hides costs in monthly maintenance and PCI compliance fees. For a high-ticket item, such as luxury retail or specialized industrial equipment, these fees can erode hundreds of dollars from a single sale. When you evaluate the pros and cons of bitcoin for business, the financial advantage becomes clear. By utilizing a low-fee gateway, you eliminate the layers of bureaucracy that traditional banks require. This efficiency translates to a leaner operation with higher capital retention and fewer administrative hurdles.

Optimizing Transaction Costs

Low-fee gateways don’t just save money; they simplify the entire accounting process. In a high-ticket retail environment, a 3% fee on a $20,000 transaction costs the merchant $600. A crypto transaction at 0.5% reduces that cost to $100. Over hundreds of transactions, these savings accumulate into a substantial capital reserve. This capital is then available for more productive uses, such as funding a Forex account to hedge against currency fluctuations or exploring the transformative potential of commodity markets.

Accelerating Cash Flow

Speed is a strategic asset in modern commerce. Traditional banking operates on a T+3 settlement cycle, meaning your capital is often locked in a clearing state for days. Blockchain technology facilitates real-time confirmation, providing you with immediate access to your working capital. This accelerated cash flow is essential for businesses that need to restock inventory quickly or pivot funds toward emerging market opportunities. Integrating a reliable off-ramp solution ensures that your digital earnings are ready for use in the fiat economy without unnecessary delay.

Merchants often worry about the price swings of digital assets. However, professional fiat settlement services allow you to accept crypto and receive the equivalent value in USD instantly. This process removes volatility risk while maintaining the speed of the blockchain. This liquidity is the catalyst for advanced financial growth. Instead of letting capital sit idle in a low-interest bank account, you can deploy it into the CFD trading market. Accessing XAU/USD or major currency pairs allows you to turn operational revenue into a diversified investment portfolio. If you’re ready to streamline your operations, consider how a secure digital wallet can anchor your new financial strategy.

Leveraging Crypto Liquidity for Gold and Forex CFD Trading

The concept of “active liquidity” transforms how a merchant views their balance sheet. Instead of allowing revenue to sit idle in a traditional bank account, forward-thinking businesses treat their settled assets as a springboard for growth. One of the primary benefits of accepting cryptocurrency is the seamless transition it provides from retail revenue to institutional-grade trading. When you accept digital payments, your capital remains in a high-velocity environment. This allows you to deploy funds into the XAU/USD market or major currency pairs with a speed that traditional banking cannot replicate. It’s about ensuring every dollar of revenue is working toward your next financial milestone.

This shift in strategy has the transformative potential to change a business’s financial life. By moving beyond the role of a passive payment receiver, you become an active participant in global markets. Using USD-pegged stablecoins like USDT as a base, you can enter Forex positions that hedge against the volatility of your local currency. It’s a sophisticated method of turning operational cash flow into a high-growth financial engine. The integration of payment gateways with trading accounts creates a unified ecosystem where capital never has to leave the digital fast lane.

Gold CFDs: Hedging Against Inflation

Merchants operating in 2026 face persistent inflationary pressures that can erode the purchasing power of fiat reserves. Trading Gold CFDs (XAU/USD) offers a professional solution to this challenge. Unlike physical gold, which requires secure storage and complex logistics, CFDs allow you to profit from price movements without the burden of physical ownership. This flexibility ensures your capital remains liquid while benefiting from the historical stability of gold. It’s a secure way to preserve value when local fiat currencies fluctuate unpredictably, providing a reliable anchor for your corporate wealth.

Forex Trading for Global Merchants

Forex trading provides a strategic avenue to optimize your currency exposure. By trading USD pairs, you can protect your margins from unfavorable shifts in the foreign exchange market. For experienced financial officers, the high-yield potential of leveraged CFD positions offers a way to accelerate capital growth beyond standard business operations. Crypto-native platforms facilitate this process by providing a unified ecosystem where settlement and trading happen in the same digital space. This integration reduces the time spent on transfers, allowing you to react to market signals in real time. The ability to move from a merchant sale to a leveraged Forex position in minutes is a definitive advantage in the modern financial evolution.

Implementing a Secure and Compliant Crypto Ecosystem

Establishing a robust financial infrastructure is the prerequisite for long-term success in the digital economy. While previous sections highlighted liquidity and trading potential, those advantages are only sustainable with a foundation of institutional-grade security. One of the core benefits of accepting cryptocurrency is the ability to operate within a transparent, cryptographic ledger that reduces fraud. However, this transparency must be paired with rigorous KYC/AML protocols to ensure your business remains compliant with evolving global standards. By integrating Payment APIs, you create a frictionless experience for your customers while maintaining the back-end integrity required for professional financial audits.

Compliance is the bridge between disruptive tech and traditional reliability. In 2026, regulatory clarity has improved significantly, as seen with the California Digital Financial Assets Law and new licensing requirements in Russia. These frameworks demand that merchants verify the source of funds to prevent illicit activity. One of the strategic benefits of accepting cryptocurrency through a licensed partner is the assurance that every transaction meets these global standards. This institutional reliability is what allows a business to move seamlessly from retail sales to the XAU/USD trading markets without facing account freezes or legal roadblocks. Security is not optional.

The Importance of Regulatory Compliance

Partnering with a regulated Money Services Business (MSB) is a non-negotiable step for scaling merchants. Registration with FinCEN (31000315326622) and FINTRAC (M23088601) provides the institutional trust unregulated processors lack. These licenses ensure your provider adheres to strict financial reporting standards. Compliant gateways protect your business from legal scrutiny. For high-volume transfers, OTC desks provide the liquidity depth needed for professional conversions without market disruption.

POS Integration for Retail and Hospitality

Digital assets are rapidly moving into physical commerce. POS terminals allow brick-and-mortar locations to accept payments with the same ease as traditional mobile wallets. In the hotel and retail store sectors, “scan and pay” functionality provides instant settlement and mirrors modern consumer habits. Managing these assets requires a secure wallet with high-level encryption to anchor your daily retail operations.

To secure your business infrastructure, explore our compliant settlement solutions.

Pallapay: Your Strategic Partner for Modern Finance

Pallapay is more than a service provider. It’s the definitive destination for merchants who refuse to let their capital sit idle. By consolidating your financial operations under one roof, you eliminate the friction that typically separates retail income from institutional investment. One of the primary benefits of accepting cryptocurrency through our ecosystem is the immediate transition from receiving a payment to managing a diversified portfolio. This isn’t just about changing how you get paid; it’s about changing your financial life. We provide the infrastructure that allows you to lead in the global evolution of finance, moving with the speed and confidence of an industry leader.

Our platform bridges the gap between disruptive innovation and institutional reliability. We understand that for a global merchant, every second of settlement delay is a lost opportunity for growth. That’s why our real-time infrastructure is designed to handle complex background processes while you focus on high-level strategy. Whether you’re utilizing an API for Crypto Payments for your e-commerce store or a physical retail store POS terminal, the result is the same: instant liquidity ready for deployment. This seamless flow is the hallmark of a professional partnership built for 2026.

From Payment Gateway to Trading Hub

Pallapay facilitates the entire journey from the first customer transaction to the final trade execution. By integrating our off-ramp solutions with your merchant account, you gain a single partner for all your OTC, POS, and API needs. This unified approach reinforces our institutional reliability brand pillar. You don’t have to manage multiple vendors to move from retail settlement to Gold or Forex CFD trading. Instead, you use a single, secure environment to turn your digital earnings into active positions in the XAU/USD market. This integration ensures that your capital is always positioned for maximum impact.

Getting Started with Pallapay

Integration is designed to be straightforward and efficient. Merchants can begin by setting up a secure digital wallet and choosing the gateway solution that fits their specific industry. We encourage you to view crypto not just as a tool for convenience, but as a strategic asset that preserves purchasing power. In a world of inflationary pressure, the ability to settle in USD-pegged assets and instantly enter the Forex market is a definitive advantage. It’s time to stop reacting to the market and start anticipating it. Empower your business with Pallapay’s crypto solutions today.

Secure Your Place in the Global Financial Evolution

The transition to digital assets is no longer a future prospect; it’s the operational standard for merchants who prioritize growth and liquidity. By internalizing the benefits of accepting cryptocurrency, you move beyond the limitations of slow, expensive banking systems. You gain the ability to settle transactions instantly and pivot that capital into high-performance markets like Gold and Forex CFDs. This integration turns stagnant revenue into an active financial engine, providing the transformative potential to change your business’s financial trajectory forever.

Success in this new landscape requires a partner that balances innovation with institutional reliability. Pallapay provides this bridge as an MSB registered in the USA and Canada, serving merchants in over 180 countries with professional OTC desk support. Whether you’re hedging against inflation with XAU/USD trades or optimizing currency exposure through USD pairs, our ecosystem handles the complexity so you can focus on leadership. It’s time to leverage your merchant liquidity for sustainable, long-term wealth. Your journey toward a more efficient financial future begins with a single integration.

Start Accepting Crypto and Access Global Markets with Pallapay

Frequently Asked Questions

Is it safe for my business to accept cryptocurrency in 2026?

Yes, accepting digital assets is safe when you utilize regulated gateways that adhere to institutional security standards. In 2026, clear regulatory frameworks like the California Digital Financial Assets Law provide a secure environment for merchants. By partnering with a licensed provider, your transactions are protected by robust encryption and full compliance with global AML and KYC protocols. This ensures your business remains protected from fraud while maintaining high operational integrity.

How do I avoid the volatility of Bitcoin when accepting payments?

You can eliminate volatility risk by using instant fiat settlement services or USD-pegged stablecoins like USDT. These tools allow you to lock in the exact fiat value of a transaction at the moment of sale. One of the core benefits of accepting cryptocurrency is this flexibility; you receive the precise amount of USD or EUR required, while your customers enjoy the convenience of paying with their preferred digital assets.

Can I trade Gold or Forex using the crypto I receive from customers?

Yes, you can transition your merchant liquidity directly into XAU/USD or major Forex CFD markets. Integrating your payment gateway with a professional trading account allows you to put stagnant capital to work immediately. This strategy enables you to hedge against inflation and explore high-growth financial opportunities. It’s an efficient way to turn your daily retail revenue into a diversified, active investment portfolio without leaving the digital ecosystem.

What are the tax implications of accepting digital assets?

Tax requirements vary by jurisdiction, but most regions treat digital assets as property or capital assets for reporting purposes. In 2026, merchants generally report gains or losses based on the fair market value of the asset at the time of the transaction. Professional gateways provide detailed transaction history and reporting tools to simplify this process. You should consult a qualified tax professional to ensure you meet all local corporate filing requirements.

Do I need a special bank account to receive crypto settlements?

You don’t need a specialized crypto bank account to receive funds if you use a professional off-ramp service. A regulated provider can convert your digital assets into fiat currency and transfer the balance directly to your existing corporate bank account. This ensures your revenue is accessible for traditional business expenses like rent or payroll. It bridges the gap between modern digital payments and established banking practices seamlessly.

How does a crypto POS terminal differ from a standard card machine?

A crypto POS terminal facilitates transactions via QR codes or NFC technology, mirroring the simplicity of modern mobile wallets. Unlike standard card machines that rely on legacy credit networks and 3-5% fees, crypto terminals settle transactions on the blockchain for significantly lower costs. This technology provides near-instant confirmation and protects your business from fraudulent chargebacks. It’s a faster, more secure alternative for brick-and-mortar retail and hospitality environments.

What is the benefit of using an MSB-registered provider like Pallapay?

Using an MSB-registered provider ensures your business is supported by a partner that meets strict regulatory standards in the USA and Canada. This registration serves as a non-negotiable trust factor, confirming that the provider follows rigorous financial reporting and security protocols. It protects your merchant operations from the legal risks associated with unregulated platforms. This institutional reliability is essential for businesses seeking a stable bridge to global financial markets.

Can I use crypto to pay my international suppliers directly?

Yes, you can pay international suppliers using digital assets to bypass the delays of the traditional SWIFT network. This method reduces intermediary bank fees and ensures your partners receive funds in minutes rather than days. It’s a highly efficient way to manage a global supply chain while maintaining 24/7 operational momentum. By paying in crypto, you simplify cross-border logistics and maintain better control over your corporate cash flow.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.