Losses from AI deepfake scams reached $577 million in the first quarter of 2026 alone, proving that yesterday’s security habits won’t protect your capital today. You’ve likely felt the persistent anxiety that comes with irreversible transactions, especially as illicit crypto volume hit $158 billion last year. It’s difficult to maintain confidence when realistic AI impersonations and shifting global regulations create a constant state of uncertainty. Mastering how to avoid crypto scams 2026 is no longer a luxury; it’s a fundamental requirement for anyone looking to bridge the gap between digital innovation and institutional financial stability.

This guide empowers you to utilize the latest security protocols and identify sophisticated fraud before it impacts your portfolio. You’ll learn to use institutional-grade strategies to protect your digital wealth and verify the legitimacy of any platform you engage with. We provide a clear checklist for platform verification and explain how to find a regulated partner for large transactions, ensuring you can convert crypto to USD or EUR with absolute certainty.

Key Takeaways

- Identify the shift from simple phishing to sophisticated AI-augmented social engineering that can bypass traditional video identity verification.

- Learn how to avoid crypto scams 2026 by recognizing the red flags of fake investment platforms and malicious smart contract approval permissions.

- Establish a verification framework centered on regulatory compliance, specifically looking for Money Services Business registrations in jurisdictions like the US and Canada.

- Strengthen your defense by implementing hardware-based security keys and processing all high-volume transactions through regulated off-ramps for secure fiat settlement.

- Discover how bridging high-tech payment APIs with physical OTC exchange reliability creates a secure environment for converting digital assets to cash.

The Evolution of Cryptocurrency Fraud in 2026

The year 2026 marks a decisive shift in the digital threat landscape. Traditional phishing attempts have largely been replaced by sophisticated, AI-augmented social engineering. Understanding The Evolution of Cryptocurrency Fraud is the first step in protecting your capital. Scammers no longer rely on misspelled emails or obvious fake websites. They use massive datasets and automation to build institutional-grade trust. Blockchain transparency, once hailed as a security feature, has become a double-edged sword. Malicious actors now use public ledger data to identify high-value targets and tailor their attacks with surgical precision. To survive this environment, you must adopt institutional security as your primary defense. This involves moving away from retail-grade habits and embracing the same rigorous standards used by global financial leaders.

AI-Powered Deepfakes and Synthetic Identities

Scammers now utilize real-time voice and video cloning to impersonate senior exchange staff or trusted financial advisors. These deepfakes are convincing enough to bypass standard video KYC protocols, making it difficult to distinguish between a legitimate request and a fraudulent one. If you receive an urgent video call regarding your account, don’t trust the visual evidence alone. Always use a secondary, out-of-band confirmation method, such as calling a verified number found on the official platform. This is a critical component of how to avoid crypto scams 2026. We are also seeing the rise of “Pig Butchering 2.0,” where AI-generated personas build long-term relationships on professional networks to lure victims into fraudulent liquidity pools with promises of guaranteed returns.

The Vulnerability of Unregulated P2P Networks

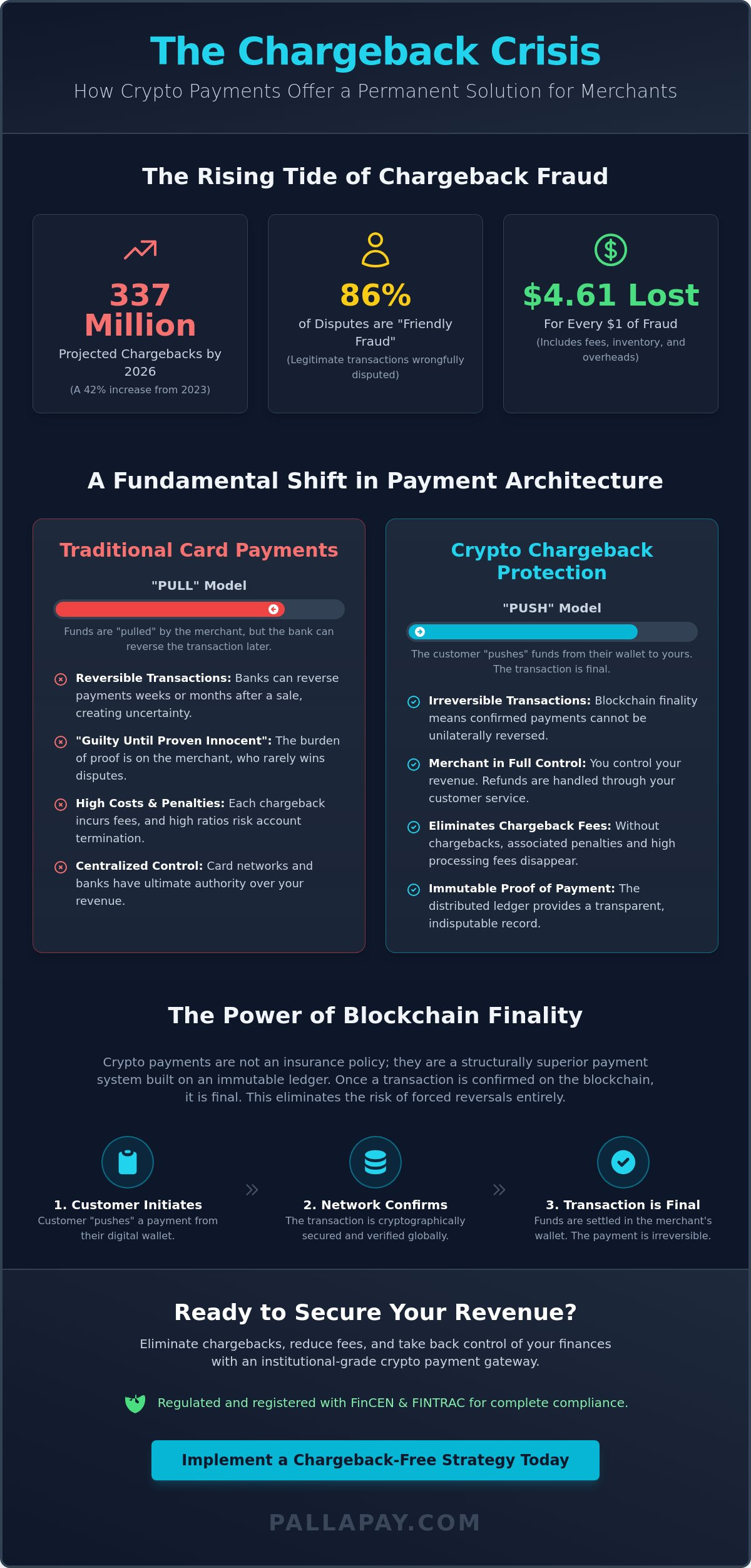

Unregulated peer-to-peer (P2P) platforms have become high-risk zones in 2026. Chargeback fraud is rampant; a buyer sends fiat currency and then reverses the transaction once the crypto is released. Additionally, the danger of “tainted” coins is higher than ever. Swapping assets with unknown parties can lead to your account being frozen by major exchanges due to anti-money laundering (AML) flags. To mitigate these risks, users should utilize a secure crypto to fiat settlement process through regulated entities. Moving your operations to a professional off-ramp ensures that your assets remain compliant. It guarantees that your liquidity is never compromised by the illicit activities of anonymous third parties.

Identifying the 4 Most Prevalent Crypto Scams Today

Protecting your digital wealth in 2026 requires more than just a strong password. You must recognize the specific mechanics of modern fraud. Scammers have refined their methods, moving away from obvious traps toward high-fidelity replicas of legitimate services. Identifying Prevalent Crypto Scams is essential for anyone managing significant digital assets. By understanding these four primary threat vectors, you can develop a proactive defense strategy. Learning how to avoid crypto scams 2026 starts with a healthy skepticism of any offer that bypasses standard market logic.

The “Guaranteed Return” Trap

Legitimate financial platforms don’t offer fixed, high-yield returns in a volatile market. If a service promises a specific percentage of ROI regardless of market conditions, it’s a red flag for a Ponzi scheme. These platforms often survive by requiring you to recruit new participants to unlock your own funds. This mechanic is a cornerstone of modern financial fraud. Pig butchering is a long-term psychological manipulation tactic where scammers build emotional rapport over months before suggesting a fraudulent investment. Don’t let the professional appearance of these platforms distract you from the absence of actual liquidity or regulatory oversight.

Smart Contract Approval Risks

One of the most dangerous technical threats involves the “unlimited allowance” permission. When you connect your crypto wallet to a malicious decentralized application (DApp), a single approval can grant the contract permission to drain your entire balance. Scammers hide these permissions in complex code that looks like a standard transaction. It’s vital to use auditing tools to regularly review and revoke smart contract permissions. You should also maintain a strict separation between your “hot” wallets used for DApp interactions and your “cold” wallets used for long-term storage. If you need to convert large amounts of digital assets, using a regulated crypto offramp is significantly safer than interacting with unverified smart contracts.

Impersonation scams have also evolved to target professional users. Fraudsters now pose as official Money Services Business (MSB) agents or fake regulatory bodies, often sending “compliance notices” to induce panic. They use these high-pressure tactics to trick you into transferring funds to “secure” accounts. Additionally, malicious DApps are frequently promoted through social media ads, appearing as innovative new protocols. Always verify the source code and community reputation of any DApp before granting it any level of access to your assets. A secure ecosystem relies on your ability to verify every transaction at the protocol level.

The Anatomy of a Secure Crypto Exchange: Verification Framework

Identifying a secure partner in 2026 requires a fundamental shift in perspective. You aren’t just looking for a digital interface; you’re vetting a global financial technology provider. This verification framework serves as the definitive answer to how to avoid crypto scams 2026. Institutional legitimacy is built on a foundation of regulatory compliance and physical accountability. While online-only platforms often operate in jurisdictional shadows, a secure exchange maintains a transparent, multi-layered presence that bridges the gap between digital assets and traditional commerce. High-volume traders must prioritize platforms that treat security as a procedural flow rather than a static feature.

Regulatory compliance is the primary indicator of safety. Money Services Business (MSB) registration is the gold standard because it forces a platform to adhere to strict Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols. These aren’t just bureaucratic hurdles; they are essential barriers that prevent illicit actors from entering the ecosystem. Platforms that offer “No-KYC” services may seem convenient, but they represent a massive security risk. Without these safeguards, you’re transacting in an environment where your assets could be frozen due to association with tainted liquidity.

Verifying Regulatory Credentials

You can cross-reference a platform’s legitimacy by checking official government databases. In the United States, verify the MSB registration through the Financial Crimes Enforcement Network (FinCEN). As of June 2026, Pallapay LLC is registered under number 31000315326622. Similarly, in Canada, you should check the Financial Transactions and Reports Analysis Centre (FINTRAC). Verifying these credentials ensures the entity is subject to federal oversight. A global presence in established financial hubs like Singapore or Istanbul indicates institutional stability and a commitment to long-term operations. This geographic diversity suggests the platform is not a “fly-by-night” operation designed to disappear after a liquidity event.

Physical OTC Desks vs. Online-Only Exchanges

Physical presence provides a level of security that digital-only platforms cannot replicate. Over-the-Counter (OTC) desks in major financial centers allow for face-to-face high-volume transactions in secure, professional environments. This physical touchpoint significantly mitigates the risk of account-takeover fraud and social engineering. When you interact with a professional OTC manager, you’re guided through a secure trade process that prioritizes your capital’s safety. Utilizing a regulated crypto offramp with physical locations ensures that large-scale trades are handled with institutional precision. This approach provides a reliable bridge for converting digital wealth into fiat currency without the friction or uncertainty of unverified online swaps.

5 Essential Steps to Secure Your Digital Assets

Securing digital wealth in 2026 requires a shift from passive awareness to active, institutional-grade defense. Understanding how to avoid crypto scams 2026 is only the first step; you must implement a rigorous technical framework to protect your liquidity. This process involves eliminating single points of failure and ensuring every transaction occurs within a regulated ecosystem. By adopting these five essential steps, you can bridge the gap between high-tech innovation and traditional financial reliability. Proactive security is the only way to maintain absolute control over your digital capital.

Start by implementing hardware-based security for all account access. Move beyond standard authentication methods and use physical security keys to prevent unauthorized entry. Whitelisting withdrawal addresses is another critical layer. By restricting where your funds can be sent, you ensure that even if a breach occurs, the capital remains within your controlled network. You should also conduct periodic security audits to review wallet permissions and disconnect any devices or DApps that are no longer in active use. This prevents “approval bloat” from becoming a backdoor for malicious smart contracts.

Advanced 2FA and Multi-Signature Wallets

SMS-based 2FA is completely obsolete in 2026 due to the prevalence of sophisticated SIM swapping attacks. You should replace these with app-based or hardware authenticators that provide a secure, encrypted link to your identity. For business accounts or large holdings, multi-signature wallets are essential to prevent a single-point-of-failure by requiring multiple approvals for a single transaction. Cold storage is the offline preservation of private keys, ensuring your primary assets are never exposed to the internet. This physical separation is the most effective defense against remote hacking attempts.

Secure Off-Ramping and Fiat Conversion

The final stage of any trade is often the most vulnerable. Utilizing unverified crypto off-ramps can lead to bank account flags and permanent fund freezes if the liquidity source is untraceable. You must ensure your crypto to fiat settlement is compliant with global financial standards and processed through official channels. Regulated platforms provide a professional bridge that connects your digital assets to official bank transfers without the risk of regulatory scrutiny. This ensures that your wealth transition is both fast and legally sound.

For institutional-grade liquidity and safety, you can securely sell crypto to bank through our regulated global network, ensuring every transaction meets the highest security standards.

The Pallapay Standard: Secure, Regulated, and Global

Pallapay represents the definitive destination for users seeking to implement the security frameworks discussed throughout this guide. Choosing a regulated partner is the most effective strategy for how to avoid crypto scams 2026. Our commitment to safety is evidenced by our active Money Services Business (MSB) registrations in key global jurisdictions. In the United States, Pallapay LLC is registered with FinCEN under number 31000315326622. In Canada, Pallapay Ltd. maintains its registration with FINTRAC under number M23088601. These credentials ensure that every transaction occurs within a framework of federal oversight and institutional accountability, providing the stability that professional traders require.

Our global ecosystem merges disruptive innovation with the reliability of established commerce. We provide a comprehensive suite of tools, from high-tech payment APIs to the physical reliability of our OTC desks. This multi-layered approach ensures that high-volume institutional and retail trades are handled with absolute precision. By integrating these services, we eliminate the friction often found in fragmented digital asset platforms. The result is a secure, utility-focused environment where your digital wealth is treated with the same rigor as traditional financial assets.

Institutional Grade Security for Every User

The integrity of our ecosystem is maintained through rigorous KYC and AML protocols. These procedures are active defenses that protect our users from the illicit liquidity and “tainted” coins that often plague unregulated P2P networks. Our secure crypto POS infrastructure also allows merchants to accept digital payments with the same confidence as traditional fiat transactions. For those managing significant capital, our Institutional OTC Guide provides deeper insights into maintaining safety during large-scale operations. We don’t just provide tools; we act as a strategic partner in your financial growth.

Bridging Fiat and Crypto with Absolute Trust

Pallapay serves as the professional bridge between established financial practices and modern technological advancements. As a regulated financial technology provider, we offer instant conversion to USD, EUR, and other major global currencies through secure, verified channels. The Pallapay Mastercard further enhances this security by providing a friction-less way to spend your digital assets globally without exposing your primary holdings to unverified third-party applications. This creates a closed-loop environment where your wealth remains protected at every touchpoint. The momentum of the digital economy requires a partner that facilitates real-time operations without compromising safety. Join a secure ecosystem—Explore Pallapay services today.

Securing Your Position in the Future of Finance

The transition toward an AI-augmented threat landscape demands a move away from retail-grade security habits. Trust is built on accountability. You’ve learned that hardware-based authentication and the verification of institutional credentials are now mandatory requirements for asset protection. Implementing these rigorous protocols is the definitive strategy for how to avoid crypto scams 2026 while maintaining global liquidity. By prioritizing regulated partners with a physical presence, you eliminate the jurisdictional uncertainty that fraudsters exploit.

Pallapay provides the professional bridge you need to operate with absolute trust. As a regulated financial technology provider with MSB registrations in the USA and Canada, we maintain the highest standards of compliance. Our physical OTC desks in Singapore and Istanbul offer secure environments for high-volume transactions. This ensures your wealth remains protected at every step of the conversion process.

Secure your assets with a regulated global leader; start with Pallapay.

The digital economy is evolving rapidly. Your security doesn’t have to be a source of anxiety. With the right strategic partner and institutional-grade protocols in place, you can grow your portfolio with confidence and stability.

Frequently Asked Questions

How can I tell if a crypto investment platform is a scam in 2026?

Look for “guaranteed” returns and a lack of verifiable regulatory credentials. Legitimate platforms in 2026 never promise fixed ROI in volatile markets. You should verify the entity’s MSB registration number through official government databases like FinCEN. Learning how to avoid crypto scams 2026 involves scrutinizing the platform’s physical presence and its history of third-party audits. If the platform pressures you to recruit others, it’s likely a Ponzi scheme.

Is it safe to use P2P exchanges for large cryptocurrency trades?

Peer-to-peer exchanges carry significant risks in 2026, including chargeback fraud and exposure to “tainted” assets. High-volume traders should prioritize regulated OTC desks instead of anonymous P2P swaps. These professional environments provide a secure bridge between digital assets and fiat currency. Using a regulated off-ramp ensures your transactions comply with global AML standards, preventing your bank account from being flagged or frozen due to suspicious liquidity sources.

What should I do if I think my crypto wallet has been compromised?

Act immediately by transferring any remaining assets to a fresh, hardware-secured wallet. You must also use a decentralized auditing tool to revoke all smart contract permissions and “unlimited allowances” associated with the compromised address. Change all passwords for linked exchange accounts and enable hardware-based 2FA. Reviewing your security logs for unauthorized device access is a critical step in understanding how to avoid crypto scams 2026 and preventing future breaches.

Why is MSB registration important when choosing a crypto exchange?

MSB registration signifies that a platform is a regulated financial technology provider subject to federal oversight. It forces the exchange to implement rigorous KYC and AML protocols, which protect the integrity of the entire ecosystem. Choosing an MSB-registered partner ensures your capital is handled with institutional-grade accountability. This registration provides a verifiable trail of legitimacy that distinguishes professional global leaders from high-risk, unregulated entities operating in jurisdictional shadows.

Can AI deepfakes really bypass exchange security measures?

Sophisticated deepfakes can impersonate users during video KYC or simulate support staff in real-time calls. Scammers use these synthetic identities to gain unauthorized access or trick users into transferring funds. To defend against this, you should never rely on video evidence alone. Always implement a secondary, out-of-band confirmation method, such as a verified phone call or an encrypted message, before authorizing any high-value transaction or account change.

What is the safest way to convert a large amount of crypto to cash?

The safest method for high-volume conversion is using a regulated OTC exchange with physical offices. This approach allows for face-to-face transactions in secure environments, eliminating the risks associated with online-only swaps. Professional OTC managers guide you through the process, ensuring your crypto to bank transfer is processed through official financial channels. This institutional-grade path provides absolute certainty and prevents the liquidity issues common with unverified digital off-ramps.

Are hardware wallets still the best way to store crypto in 2026?

Hardware wallets remain the industry standard for cold storage by keeping private keys completely offline. They provide a physical layer of security that remote hackers cannot bypass. While hot wallets are useful for frequent DApp interactions, your primary digital wealth should always reside in a hardware-secured environment. Using physical security keys for two-factor authentication further strengthens your defense against the evolving social engineering tactics used by modern fraudsters.

How does a regulated payment gateway protect my business from fraud?

A regulated payment gateway implements real-time transaction monitoring and rigorous AML screening to identify illicit activity. It acts as a professional filter that prevents fraudulent liquidity from entering your business accounts. By utilizing secure APIs and crypto POS machines, you ensure that every customer payment is verified against global compliance standards. This institutional-grade protection allows your business to scale globally while maintaining the highest levels of financial stability and trust.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.