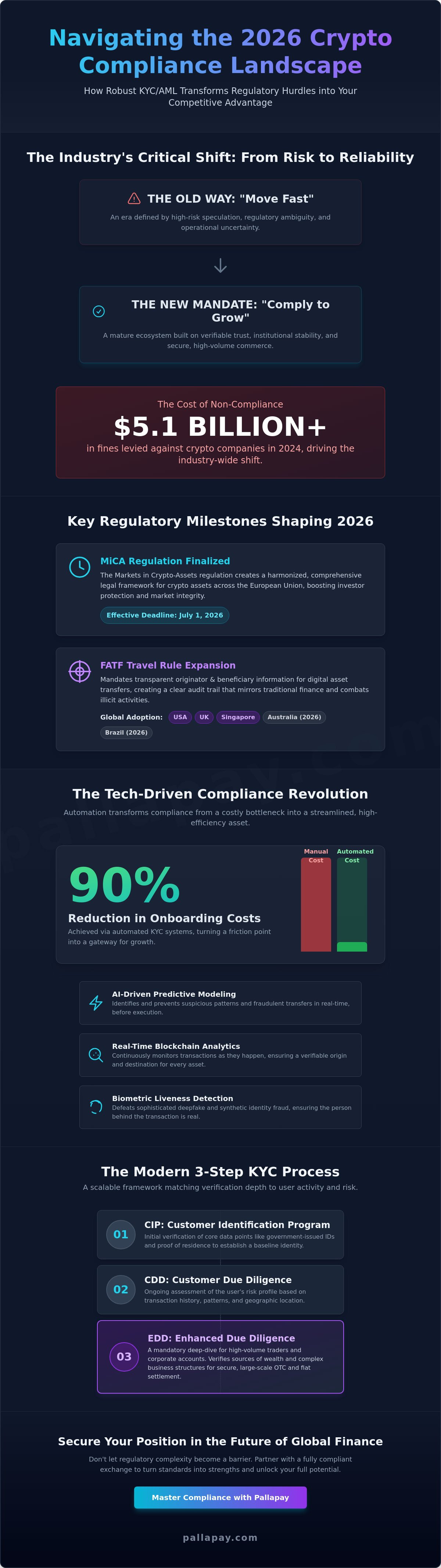

With over $5.1 billion in fines levied against crypto companies in 2024, the industry has shifted from a “move fast” mentality to a “comply to grow” mandate. It’s understandable if you’re frustrated by slow verification processes or the constant worry that a regional policy change might freeze your operational capital. You deserve a partner that turns these regulatory hurdles into competitive advantages. This guide ensures you master the evolving requirements of a modern kyc aml crypto exchange, proving that robust compliance is the essential infrastructure for accessing deep, institutional-grade liquidity.

By reading on, you’ll gain clarity on the July 1, 2026, MiCA deadline and the global expansion of the FATF Travel Rule across major jurisdictions. We’ll explore how automated systems now reduce onboarding costs by up to 90%, transforming what used to be a friction point into a streamlined gateway for growth. From OTC desks to instant fiat conversions, you’ll see how regulated platforms provide the absolute stability your high-volume transactions demand in a mature financial ecosystem. This is your roadmap to navigating the 2026 standards with confidence and precision.

Key Takeaways

- Understand the global impact of the July 2026 MiCA deadline and the expanded FATF Travel Rule on international digital asset transfers.

- Discover why selecting a fully regulated kyc aml crypto exchange is the only secure path to protect your capital from account freezes and regulatory seizure.

- Learn how institutional-grade exchanges utilize advanced encryption to safeguard your data while maintaining rigorous legal transparency.

- Master the specific documentation protocols required to verify high-limit corporate accounts for seamless, large-scale OTC transactions.

- Leverage MSB-registered platforms and physical OTC desks to convert crypto to fiat with institutional-grade reliability.

The Evolution of KYC and AML in the 2026 Crypto Landscape

The digital asset market has reached a definitive stage of maturity. By mid-2026, the transition from experimental speculation to institutional stability is complete, driven largely by the final implementation of the Markets in Crypto-Assets (MiCA) regulation on July 1, 2026. Global regulators no longer view compliance as an optional feature. They see it as the fundamental requirement for any kyc aml crypto exchange seeking to operate within the legitimate financial system. This shift ensures that every participant is verified, creating a secure environment for high-volume commerce.

The Financial Action Task Force (FATF) has successfully harmonized expectations across major jurisdictions. The Travel Rule is now standard in the US, UK, and Singapore, with Australia and Brazil following suit in 2026. This consistency eliminates the regulatory arbitrage that previously plagued the industry. Global transparency isn’t just a legal hurdle; it’s the catalyst for mass adoption. It provides the security that professional investors require before committing significant capital to the market. Trust is the new currency of the digital age.

Why Regulation is the Bridge to Institutional Finance

Institutional liquidity requires a clear connection to established financial networks. When a kyc aml crypto exchange adheres to global anti-money laundering standards, it removes the friction between digital assets and traditional banking. This integration reduces market volatility by inviting long-term holders rather than short-term speculators. Regulated financial technology has replaced the unverified platforms of the past. This evolution ensures that assets are safe and every transaction is verifiable. For businesses, this means having a reliable crypto off-ramp that traditional banks will accept without hesitation or suspicion.

2026 Regulatory Trends: AI and Real-Time Reporting

Compliance is now proactive rather than reactive. Modern systems use blockchain analytics to monitor transactions as they happen. In 2025, automated KYC systems reduced onboarding costs by 90%, making high-level security both accessible and fast. AI-driven predictive modeling now identifies suspicious patterns before they execute. This technology doesn’t just flag illicit activity; it protects users by preventing fraudulent transfers in real-time. The result is a cleaner, more efficient ecosystem where speed and safety coexist perfectly. By adopting these standards, exchanges move faster while maintaining absolute institutional integrity.

Compliance serves as the silent engine of institutional trust. It ensures that every asset moving through the digital network has a verifiable origin and a clear destination. A high-performance kyc aml crypto exchange does not simply collect documents; it orchestrates a multi-layered defense strategy designed to mitigate risk in real-time. This structural integrity allows professional traders to move large volumes with confidence, knowing their capital is protected by rigorous legal standards.

The FATF Travel Rule is a central component of this modern framework. It mandates that essential originator and beneficiary information travels with every digital asset transfer, creating a transparent audit trail that mirrors traditional wire transfers. This transparency is reinforced by automated sanctions screening, which prevents any interaction with restricted entities or high-risk jurisdictions. By 2026, the focus has shifted to counter synthetic identity fraud. Sophisticated platforms now use biometric liveness detection to defeat deepfake technology. This ensures that the person behind the transaction is a real, living individual, not a synthetic reconstruction designed to bypass security.

KYC: The Three-Step Identity Verification Process

Identity verification is a progressive process that scales with the user’s activity. It begins with the Customer Identification Program (CIP), where core data points like government-issued IDs and residential proof are verified. Once the identity is established, Customer Due Diligence (CDD) assesses the user’s risk profile based on their transaction history and geographic location. For high-volume traders or corporate entities, Enhanced Due Diligence (EDD) becomes mandatory. This deeper analysis verifies sources of wealth and complex business structures, providing the security required for premium services such as fiat settlement.

AML and the Fight Against Financial Crime

Anti-money laundering protocols function as a continuous monitoring layer that never sleeps. Systems analyze transaction frequency and volume to detect anomalies that deviate from a user’s established behavioral profile. This logic is heavily informed by FinCEN’s advisory on illicit virtual currency activity, which provides the red flag indicators used to identify potential money laundering. If suspicious patterns are detected, exchanges are legally bound to file Suspicious Activity Reports (SARs) with the appropriate authorities. These efforts are part of a broader commitment to Combating the Financing of Terrorism (CFT). By maintaining these high standards, a platform ensures it remains a safe harbor for legitimate global commerce.

If you are managing high-value assets, you should partner with an OTC crypto exchange that integrates these comprehensive security pillars into every transaction.

Privacy vs. Compliance: Addressing the #1 Trader Objection

The tension between personal privacy and regulatory oversight is often framed as a zero-sum game. In the 2026 financial environment, this perspective is outdated. A premier kyc aml crypto exchange doesn’t view privacy as an obstacle. It views it as a data security challenge that requires institutional-grade solutions. While some traders still seek out unverified platforms to avoid documentation, they often realize too late that anonymity comes at a steep price. Without a transparent audit trail, your wealth remains disconnected from the global economy.

Institutional liquidity requires accountability. Large-scale market makers and corporate entities don’t interact with unverified pools because the risk of “tainted” assets is too high. If you acquire digital assets through an unregulated source, those funds are frequently flagged by blockchain analytics tools. When you eventually attempt to move these assets to a compliant crypto off-ramp, you risk permanent account freezes. Transparency is the only way to ensure your liquidity remains portable and legitimate across all borders.

The Dangers of Unregulated ‘No-KYC’ Platforms

Choosing an unverified platform exposes you to significant operational vulnerabilities. These exchanges often possess inferior security infrastructure, making them prime targets for hackers. If your funds are stolen from an unregulated entity, there’s no regulatory body to facilitate recovery. The lack of oversight means “No-KYC” often translates to “No-Recourse” when an exit scam occurs. This gap makes it impossible to prove the legal source of your funds to traditional financial institutions, effectively trapping your wealth in a digital silo.

Institutional Standards for Data Protection

A compliant exchange protects your identity with the same rigor it uses to protect your assets. Leading platforms utilize Zero-Knowledge Proofs (ZKPs) to verify user eligibility without storing or transmitting sensitive raw data. This technology allows for “private-yet-compliant” interactions where the system confirms you’re a verified user without exposing your specific details to the network. All documentation is held in encrypted, offline environments that meet the strictest GDPR and regional data protection requirements. You can learn more about protecting your assets with secure crypto practices through our dedicated security resources. By choosing a regulated partner, you aren’t sacrificing privacy; you’re securing it through professional accountability.

How to Navigate Verification for High-Volume OTC Trades

High-volume OTC (Over-the-Counter) trading demands a level of scrutiny that standard retail accounts never encounter. For institutional players, a robust kyc aml crypto exchange is the only way to move significant capital without triggering systemic red flags. This process is designed to protect both the user and the platform by ensuring that every large-scale trade is backed by legitimate, verifiable assets. By 2026, the industry has standardized these high-limit verifications to ensure that moving seven or eight-figure sums is as legally sound as a traditional bank wire.

Trust is the foundation of any high-value transaction. When you operate through a regulated entity, you aren’t just following rules; you’re securing your path to exit. Unverified trades often lead to liquidity traps where funds are frozen by intermediary banks. By contrast, a compliant exchange provides a clear audit trail that satisfies global financial standards, ensuring your wealth remains mobile and accessible.

Onboarding for OTC and Institutional Clients

Institutional onboarding moves beyond simple identity checks. You’ll need to provide comprehensive Proof of Funds (PoF) and Source of Wealth (SoW) documentation. This ensures that the capital entering the ecosystem is clean and legally obtained. For corporate entities, Know Your Business (KYB) protocols require identifying the Ultimate Beneficial Owners (UBOs) to prevent anonymous shell companies from accessing deep liquidity. Automated document parsing now allows for rapid KYB checks, even for complex multi-jurisdictional corporate structures. Establishing a relationship with an exchange that maintains a physical presence in global financial hubs like Istanbul or Singapore adds a layer of trust and accountability that purely digital platforms lack.

Streamlining the Off-Ramp Process

Efficiency is the primary goal for high-volume traders. When your account is pre-verified to institutional standards, you bypass the manual reviews that often delay fiat settlements for unverified users. This is particularly critical for large-scale USDT to cash conversions, where market timing is everything. A verified status ensures that converting crypto to bank transfers becomes a routine operational task rather than a stressful event. You can find more detailed strategies in our Institutional Guide to OTC Crypto Trading. Pre-verification allows you to schedule high-limit withdrawals with minimal notice, ensuring your business maintains the agility needed in volatile markets.

If you’re ready to secure high-volume liquidity with a regulated partner, explore our OTC crypto exchange solutions today.

Pallapay: Setting the Standard for Secure, Regulated Exchange

Pallapay serves as the definitive bridge between disruptive digital innovation and institutional financial reliability. As a premier kyc aml crypto exchange, we prioritize official MSB registration in both the United States and Canada to ensure our partners operate within a framework of absolute legal certainty. By July 1, 2026, the global crypto market will have fully transitioned into its most regulated era. Pallapay is already operating at this peak standard, providing the infrastructure necessary for high-volume commerce to thrive without the risk of regulatory interruption.

Our commitment to security extends beyond digital protocols to include a comprehensive, integrated ecosystem. From sophisticated payment APIs to physical POS terminals, we handle the complex background processes of compliance so you don’t have to. This utility-focused approach allows professional and individual users alike to convert assets with total confidence. We don’t just follow the 2026 standards; we define them by aligning our technological speed with established financial practices.

Global Presence, Local Compliance

Operating in over 180 countries requires a deep understanding of regional requirements and a commitment to institutional stability. Our physical branches in Singapore and Istanbul matter because they provide a tangible layer of security for high-value transactions that purely digital platforms cannot match. Working with a regulated MSB gives you the peace of mind that your assets are protected by the same rigor found in traditional finance. This global reach ensures that whether you are executing a corporate off-ramp or a high-limit OTC trade, your liquidity remains secure and your documentation remains private under the strictest encryption standards.

The Pallapay Advantage for Businesses

Businesses in e-commerce and hotels require more than just a gateway; they need a strategic partner that eliminates market volatility. Our platform facilitates instant fiat settlements, allowing you to accept digital assets while receiving the exact currency your operations demand. This eliminates the friction often associated with technical conversions, turning complex crypto operations into standard business procedures. We provide 24/7 support to ensure that high-volume traders and corporate partners always have the assistance they need to navigate the evolving kyc aml crypto exchange landscape. By adopting our solutions, your business gains the momentum needed to lead in an inevitable global evolution.

Securing Your Position in the Future of Global Finance

The transition toward a fully regulated ecosystem is a strategic evolution that protects your capital and ensures long-term operational growth. By adopting these standards, you move away from the vulnerabilities of unverified platforms and enter a space defined by institutional trust. Choosing a kyc aml crypto exchange that prioritizes transparency allows you to access deep liquidity while maintaining the highest levels of data security. This infrastructure is essential for anyone looking to navigate the complexities of modern commerce with precision.

Pallapay is a registered MSB in the USA and Canada, currently serving professional and individual users across 180+ countries. Our physical OTC desks in major financial hubs provide the tangible reliability that digital-only platforms lack. We handle the complex background processes of compliance so you can focus on accelerating your own progress. It’s time to secure your assets with a partner that bridges the gap between disruptive technology and institutional stability.

Start your secure, compliant crypto journey with Pallapay today. Your path to reliable, high-volume liquidity begins with a commitment to excellence.

Frequently Asked Questions

Can I trade cryptocurrency without KYC verification in 2026?

Trading without verification is no longer a viable option on any reputable kyc aml crypto exchange due to the 2026 global regulatory mandate. While some unverified platforms still operate in high-risk zones, they lack any form of legal protection and frequently face sudden seizure by international authorities. Choosing a regulated path is the only way to ensure your capital remains mobile and connected to the broader financial system.

What documents are typically required for crypto exchange KYC?

Standard documentation includes a valid passport or national ID, a recent utility bill for residential proof, and a real-time biometric scan to prevent identity theft. For high-limit institutional accounts, you’ll also need to provide audited financial statements or bank records to establish your source of wealth. These extra steps are essential for unlocking premium liquidity and ensuring your high-volume trades proceed without technical friction.

How long does the AML screening process take for large trades?

AML screening is typically instantaneous for standard transactions thanks to advanced blockchain analytics that monitor the network in real-time. For institutional-grade volume, the process remains highly efficient; it usually finishes within one business day as dedicated compliance teams verify the legitimacy of the transfer. This speed ensures that your business maintains its momentum while adhering to the highest global standards of financial integrity.

What is the ‘Travel Rule’ and why does it affect my crypto transfers?

The Travel Rule mandates that crypto service providers share originator and beneficiary information for every asset transfer between exchanges. This requirement aligns digital assets with international financial standards used by traditional banks, ensuring that large transfers are transparent and less susceptible to regulatory blocks. It’s a fundamental part of the 2026 compliance landscape that allows for the safe, global movement of digital wealth.

Is my personal data safe with a regulated crypto exchange?

Regulated platforms prioritize data security through AES-256 encryption and secure, offline storage protocols for all sensitive documentation. By following strict GDPR guidelines and regional data protection acts, a kyc aml crypto exchange ensures your personal information is used only for legal verification. This professional approach protects your identity from unauthorized access while maintaining the transparency required by modern financial regulators.

What happens if a transaction is flagged for AML review?

A flagged transaction triggers an internal review where the platform analyzes the transfer’s origin and destination against known risk patterns. You’ll receive a direct request for additional context or supporting documentation to clarify the nature of the activity. Once the compliance team verifies the legitimacy of the transaction, the funds are promptly released to their destination, ensuring your account remains in good standing.

Do I need KYC to buy Bitcoin with cash at an OTC desk?

Yes, verifying your identity is mandatory when purchasing Bitcoin with cash at a professional OTC desk to comply with global anti-money laundering laws. This requirement ensures that the cash used in the transaction is legitimate and has a clear source. By completing this step, you protect yourself from inadvertently participating in illicit activity and ensure your assets are recognized as clean by other financial institutions.

What is the difference between KYC and KYB in the crypto industry?

KYC focuses on verifying the identity of an individual user through personal documentation like government IDs and biometric data. KYB, or Know Your Business, involves a deeper investigation into corporate structures to identify the ultimate beneficial owners and verify the company’s legal status. Both processes are critical for maintaining the integrity of the crypto ecosystem and facilitating secure, high-volume transactions for corporate partners.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.