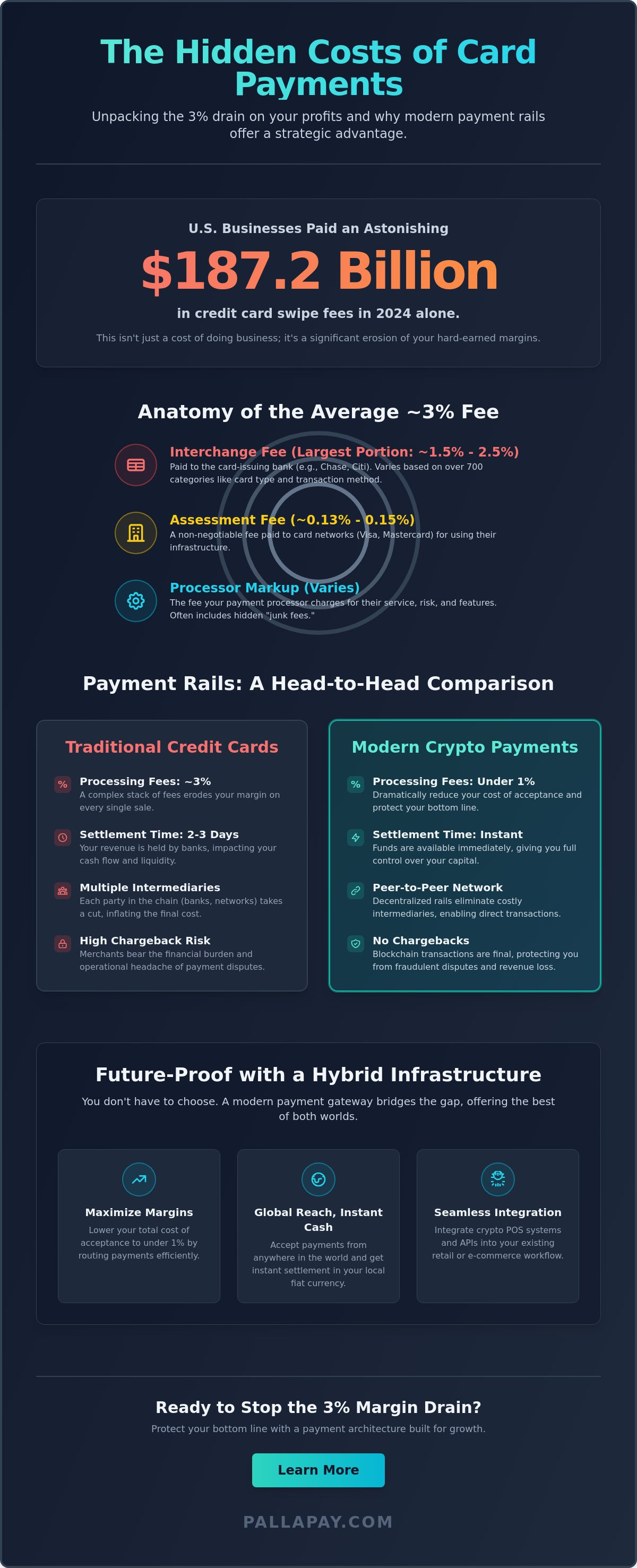

In 2024, U.S. business owners surrendered $187.2 billion to credit card swipe fees, a figure that highlights a growing crisis for merchant profitability. If you’re managing a growing enterprise, you’ve likely felt the sting of margin compression and the frustration of opaque monthly statements. Understanding the real impact of crypto vs credit card processing fees is no longer just a technical exercise; it’s a vital strategic move to protect your bottom line. You deserve a payment architecture that works for your growth rather than acting as a tax on your success.

This guide provides a clear roadmap to bypass the standard 3% margin drain by utilizing modern payment rails and structural fee-mitigation strategies. You’ll discover how to lower your net cost of acceptance to under 1% while facilitating instant global settlements. We will explore the integration of crypto payment gateways and POS systems that bridge the gap between digital assets and traditional fiat, ensuring your business remains agile in an evolving global economy.

Key Takeaways

- Identify the complex layers of interchange and assessment fees to stop the hidden erosion of your merchant margins.

- Evaluate the operational advantages of crypto vs credit card processing fees to reduce your total cost of acceptance to under 1%.

- Implement surcharging or cash discounting models to provide immediate relief from high-cost legacy payment networks.

- Integrate professional-grade APIs and crypto POS machines to bridge the gap between traditional commerce and blockchain efficiency.

- Utilize a hybrid payment infrastructure to ensure instant settlements in fiat and maintain absolute liquidity in a global market.

Why Traditional Credit Card Fees Are Eroding Your 2026 Margins

Traditional payment processing is not a single cost; it is a cumulative drain on your revenue. In 2024, U.S. business owners paid a staggering $187.2 billion in swipe fees. By 2026, the structural inefficiencies of legacy systems have only intensified. When analyzing crypto vs credit card processing fees, it becomes clear that the traditional model is built on a foundation of centralized intermediaries, each requiring a slice of your transaction. This model is structurally unable to offer zero fees because it must sustain the profit margins of card issuers, networks, and processors simultaneously.

The anatomy of a standard transaction consists of three distinct layers. First is the Interchange fee, which represents the largest portion of the cost and is paid directly to the card-issuing bank. Second are assessment fees, which are non-negotiable charges paid to the card networks like Visa or Mastercard for the use of their infrastructure. Finally, the processor adds a markup to cover their own operational risks and services. Beyond these visible costs, merchants often find their effective rates inflated by hidden expenses such as PCI compliance fees, monthly statement charges, and gateway maintenance costs. In a 2026 economic environment marked by persistent overhead inflation, processors frequently pass their own rising operational costs onto merchants through increased markups.

The Complexity of the Interchange-Plus Model

The interchange-plus pricing model is often marketed as transparent, yet it relies on a web of over 700 different interchange categories. These categories are determined by variables you cannot control, such as the type of card used or the industry code of your business. Transactions where the card is not present (CNP) trigger higher risk-based pricing, often pushing rates toward the 3% threshold. Card networks set these rates, while merchant acquirers manage the flow, leaving you with little leverage to reduce the baseline cost of acceptance.

Calculating Your Effective Rate

To understand your true financial position, you must look past the teaser rates offered by flat-rate processors. Calculating your effective rate involves dividing your total processing fees by your total sales volume for a specific period. This simple formula reveals the impact of “junk fees” like batch headers or non-qualified surcharges that can often be removed through aggressive negotiation. For digital storefronts, integrating a payment solution for e-commerce that bypasses these layers is essential for long-term health. The effective rate is the true cost of acceptance including all dues.

Immediate Fee Mitigation: Surcharging, Cash Discounting, and ACH

Merchants don’t have to wait for a total infrastructure overhaul to see immediate relief from margin compression. Tactical adjustments within your current payment framework can provide instant results. While the long-term debate of crypto vs credit card processing fees often points toward blockchain as the ultimate solution, surcharging and cash discounting offer intermediate ways to reclaim lost revenue. These strategies shift the financial burden of high interchange rates away from the business and toward the payment method choice itself.

Surcharging involves adding a specific percentage fee to transactions made with credit cards. By 2026, legal landscapes have evolved to require strict transparency; merchants must provide clear signage at both the entrance and the point of sale. It’s vital to remember that surcharging debit cards remains prohibited under most regulatory frameworks. Alternatively, cash discounting incentivizes lower-cost payment methods by offering a reduced price for customers who avoid credit cards. This approach is often viewed more favorably by consumers, as it frames the savings as a benefit rather than a penalty.

Pros and Cons of Surcharge Programs

Implementing a surcharge program requires a delicate balance between margin protection and customer experience. While it effectively neutralizes the 3% interchange drain, it can lead to increased checkout abandonment if not communicated clearly. Technical integration is another hurdle. Your retail store POS system must be capable of itemizing the surcharge on both digital and physical receipts to remain compliant. Strategic merchants often prefer convenience fees over surcharges for specific service channels, such as online portals, to mitigate the risk of alienating their core loyalists.

ACH Transfers for High-Value Transactions

For high-ticket B2B invoices exceeding $5,000, moving away from plastic is a logistical necessity. ACH and e-check transfers offer a flat-fee structure that is significantly more attractive than percentage-based card fees. However, this method introduces its own set of operational frictions. The primary trade-off is speed; while credit cards authorize instantly, ACH settlements typically take 3 to 5 business days. This delay can disrupt cash flow for businesses requiring immediate liquidity. Furthermore, risk management is paramount when dealing with ACH, as Non-Sufficient Funds (NSF) returns can occur days after a service is rendered. If your business requires the cost-efficiency of ACH with the speed of modern rails, exploring instant fiat settlement options can bridge the gap between low fees and real-time availability.

Decentralized Payment Rails: The Ultimate Structural Alternative

The structural battle of crypto vs credit card processing fees is won at the architectural level. Traditional payment systems rely on a centralized web of issuing banks, acquiring banks, and card networks, each requiring a commission for their participation. By removing the interchange middleman, decentralized payment rails bypass the complex fee categories that plague standard merchant accounts. This shift isn’t just a minor adjustment; it’s a fundamental move from a legacy model to a streamlined, direct-to-ledger system.

The cost disparity is stark. While traditional card transactions often drain 3% or more from every sale, crypto processing fees typically remain under 1%. These savings accumulate rapidly, especially for high-volume retailers. Beyond the immediate fee reduction, decentralized rails solve the problem of settlement latency. Instead of waiting through 3-day bank cycles for funds to clear, merchants gain access to real-time liquidity. This acceleration of cash flow allows businesses to reinvest capital instantly rather than letting it sit in a processor’s holding account.

Global accessibility is another primary advantage of blockchain-based payments. Merchants can accept transactions from customers in over 180 countries without facing the high cross-border surcharges common in the credit card industry. Because the network is global by design, a payment from London is processed with the same efficiency as a payment from New York. This eliminates the need for expensive international merchant accounts and simplifies global expansion.

The Mechanism of Fiat Settlement

One common concern for businesses is the perceived complexity of managing digital assets. Modern gateways solve this by allowing merchants to accept Bitcoin or USDT while receiving deposits in their local currency. This process removes the technical burden of managing wallets or private keys. By utilizing a crypto payment gateway, you can eliminate volatility risk through instant conversion at the time of sale. Learn how fiat settlement protects your margins by ensuring the value you see at checkout is exactly what arrives in your bank account.

Stablecoins as a Business Standard

Stablecoins like USDT and USDC are rapidly becoming the preferred digital cash for B2B operations. They offer the speed of a blockchain transaction without the price fluctuations of traditional cryptocurrencies. Stablecoins maintain a 1:1 peg to fiat while utilizing blockchain speed. This stability makes them ideal for lowering the cost of cross-border vendor payments. Instead of paying hefty wire fees and losing money on unfavorable exchange rates, businesses can send stablecoins across the globe for a fraction of the cost, ensuring that more capital stays within the operational budget.

Navigating the Transition: Security, Compliance, and Integration

Shifting from legacy systems to modern payment rails requires a strategic focus on institutional reliability. When evaluating crypto vs credit card processing fees, the financial incentives are significant, but the transition must be supported by a robust security framework. A successful integration bridges the gap between disruptive technology and standard business practices. It ensures that your operational flow remains uninterrupted while your margins expand. This evolution is not about abandoning established practices; it is about enhancing them with more efficient infrastructure.

Security is the bedrock of this transition. Institutional-grade custody and multi-signature wallets provide a level of protection that rivals traditional financial systems. These technical safeguards ensure that digital assets are handled with the same rigor as fiat currency. By choosing a partner that prioritizes these background processes, you can focus on growth without being overwhelmed by the underlying mechanics of blockchain security. This approach instills absolute trust in both your professional partners and your individual customers.

Training your frontline team is a vital component of a successful retail implementation. Modern retail environments require staff who are comfortable facilitating alternative payment methods at the point of sale. Fortunately, current technology makes this effortless. Interfaces are designed for simplicity, allowing employees to process transactions with the same speed and confidence as a standard credit card swipe. This lack of friction is essential for maintaining the communication rhythm and efficiency that your customers expect.

Compliance and MSB Registration

Compliance is a non-negotiable requirement for institutional trust in the 2026 landscape. Merchants must prioritize partners with verified MSB registrations from authorities like FinCEN in the United States or FINTRAC in Canada. These registrations serve as essential trust signals, proving that the provider adheres to strict KYC and AML requirements. As the Digital Asset Market Clarity Act (CLARITY Act) continues to shape the regulatory environment, working with a regulated entity is the only way to ensure long-term stability. Secure your transactions with an MSB-regulated gateway to protect your business from the risks of unregulated payment channels.

Seamless E-commerce Integration

Integration is vital for maintaining high conversion rates in digital storefronts. Utilizing a payment API allows you to offer diverse payment options directly alongside traditional cards, effectively reducing checkout friction. This is particularly effective given that average order values are often 15% to 25% higher for customers who pay with crypto. Advanced merchant dashboards for e-commerce automate the reconciliation process, making the management of diverse revenue streams a standard, effortless part of your daily operations. Deploy our high-performance payment API to begin optimizing your checkout experience and recapturing lost margins today.

Future-Proofing with Pallapay’s Hybrid Payment Infrastructure

The decision-making process for crypto vs credit card processing fees concludes with the selection of a comprehensive infrastructure partner. While the cost benefits are undeniable, execution requires a system that bridges the gap between digital innovation and institutional reliability. Pallapay provides this bridge through a unified ecosystem that manages the entire lifecycle of a transaction. From the moment a customer initiates a payment to the final deposit in your corporate account, every process is optimized for speed and safety.

Consolidating your payment operations under a single provider offers a distinct strategic advantage. Instead of juggling multiple relationships with banks, processors, and exchanges, you gain a unified view of your global revenue. This integration simplifies reporting, reduces administrative overhead, and ensures that your security protocols are consistent across all channels. The financial comparison of crypto vs credit card processing fees clearly favors blockchain rails, yet the true value lies in the lack of friction within the settlement process. When your business is ready to scale, having a partner that understands the nuances of both digital assets and traditional commerce is essential for maintaining momentum.

Physical retail remains a vital touchpoint for many businesses. Traditional card terminals often lock merchants into high-fee contracts and slow settlement cycles. The Crypto POS Machine changes this dynamic by bringing decentralized efficiency to the checkout counter. It allows you to accept assets like Bitcoin or USDT with the same ease as a standard swipe, while the integrated off-ramp service ensures that your revenue is available as fiat liquidity almost instantly. This single-provider approach removes the friction of managing multiple vendors and disparate systems.

Retail Solutions for the Modern Store

Setting up a physical retail store with crypto-ready terminals is a direct answer to the rising cost of traditional processing. These systems allow you to accept Bitcoin, Ethereum, and USDT while benefiting from instant fiat conversion. This protects your business from market volatility while providing a high-tech checkout experience that sophisticated modern consumers expect. By offering secure and varied payment options, you differentiate your brand in a crowded marketplace and ensure that your margins remain protected from excessive surcharges.

The B2B Advantage: High-Volume OTC and Transfers

Managing corporate liquidity requires more than just a simple payment gateway. For high-volume operations, an OTC crypto exchange provides the necessary depth to handle large-scale conversions without price slippage. This is particularly valuable for international supplier payments. By utilizing blockchain rails instead of traditional wire transfers, you can significantly reduce the cost and time associated with cross-border commerce. Pallapay serves as a strategic partner, offering the tools needed for global business expansion while maintaining absolute financial reliability and operational efficiency.

Strategic Evolution: Securing Your 2026 Profitability

The traditional payment landscape is undergoing a necessary transformation. You’ve seen how legacy interchange models and hidden markups can drain up to 3% of your revenue. Shifting to decentralized rails allows you to eliminate the middleman and reclaim control over your operational costs. The objective comparison of crypto vs credit card processing fees reveals that the path to reclaiming your margins lies in modern, decentralized infrastructure.

Adopting a hybrid approach ensures your business remains agile while maintaining the security of established financial standards. Pallapay serves as your strategic partner in this evolution, offering an integrated ecosystem that spans 180+ countries. We provide institutional-grade security and the reliability of being MSB registered in the USA and Canada. With instant fiat settlement, you gain the benefit of blockchain efficiency without the risk of market volatility.

Switch to Pallapay and reduce your processing fees today.

Your business is ready for the next phase of global commerce. We look forward to facilitating your growth with absolute speed and stability.

Merchant FAQ: Optimizing Payment Strategy

Are there any truly zero-fee credit card processing options?

No truly zero-fee options exist because interchange and network fees are fixed costs set by card brands. You can utilize “zero-cost” processing models like surcharging to pass the 3% to 4% fee to your customers, but this often increases checkout abandonment. A more structural solution involves switching to crypto gateways, which naturally carry fees below 1% without penalizing the buyer at the point of sale.

Is it legal to pass credit card fees to customers via a surcharge?

In 2026, surcharging is legal in most jurisdictions provided you follow strict disclosure requirements. You must display the surcharge clearly at your business entrance and the point of sale to maintain compliance. It’s important to remember that some regions still restrict surcharging on debit cards. Additionally, your surcharge cannot exceed your actual cost of acceptance, which is typically capped at 4%.

How do crypto payment gateways compare to credit card fees?

Crypto payment gateways are significantly more cost-effective, with fees often ranging from 0.5% to 1% compared to the 1.5% to 3.5% common with credit cards. When analyzing crypto vs credit card processing fees, the elimination of cross-border surcharges and currency conversion markups is a primary advantage. For global merchants, this transition can result in a 70% to 80% reduction in total payment processing overhead.

What is the cheapest way to accept international payments in 2026?

The cheapest method is using stablecoin payment rails like USDT or USDC through a fiat-settlement gateway. This bypasses the SWIFT network and traditional correspondent banking fees, which can cost $25 to $50 per transaction plus FX spreads. Stablecoin transfers cost a fraction of a cent on some networks and settle in seconds. This ensures that geographic distance doesn’t dictate your operational costs.

Can I receive fiat currency if I accept cryptocurrency from a customer?

Yes, modern crypto gateways offer instant fiat settlement to protect your business from market fluctuations. When a customer pays in Bitcoin or USDT, the gateway locks in the exchange rate and converts the digital asset to fiat immediately. You then receive a standard bank deposit in USD, EUR, or other local currencies. This process completely removes any risk of price volatility while simplifying your accounting.

What industries benefit most from alternatives to credit card fees?

High-volume retail, luxury goods, and global e-commerce sectors see the most immediate benefits. For luxury retailers, a 3% fee on a $10,000 item totals $300, whereas a crypto gateway would charge roughly $50 to $100. Similarly, industries with thin margins, such as wholesale electronics, use these alternatives to protect their bottom line from being consumed by excessive bank markups and processing dues.

How long does it take to integrate a crypto payment gateway?

Integration is typically very fast, often taking less than 24 hours for standard e-commerce platforms using pre-built plugins. For custom enterprise solutions, using a robust payment API can take a few days of development time. Once the integration is complete, the system works automatically alongside your existing payment methods. It doesn’t require manual intervention for individual sales, ensuring a standard, effortless flow for your team.

Do I need a special bank account to use a crypto-to-fiat gateway?

No, you don’t need a special “crypto” bank account to utilize these modern payment rails. Regulated gateways settle funds directly into your existing corporate or business bank account via standard transfer methods. The gateway handles all blockchain interactions and compliance background processes. Your accounting department simply sees the deposit as a standard fiat transaction, maintaining your existing financial reporting structure.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.