U.S. business owners paid a staggering $187.2 billion in credit card swipe fees in 2024, yet many still hesitate to adopt more efficient digital alternatives. You likely feel that the traditional financial system is expensive; however, the common objections to accepting crypto payments, such as price volatility and regulatory uncertainty, often stall progress. It’s natural to prioritize the stability of your margins and the technical security of your operations above all else.

This guide will demonstrate how modern financial technology has matured to dismantle these barriers, transforming previous risks into measurable competitive advantages. You’ll discover how to leverage a crypto payment gateway to receive fiat currency instantly, ensuring your bottom line remains protected from market fluctuations. We provide a clear framework for mitigating risks through institutional-grade security measures and explain how recent legislation, like the 2025 GENIUS Act, provides the regulatory clarity your business needs to grow. By the end of this article, you’ll understand how to bridge the gap between established commerce and the inevitable global evolution of finance.

Key Takeaways

- Eliminate price risk by utilizing instant fiat settlement, ensuring your profit margins are preserved regardless of market movement.

- Address common objections to accepting crypto payments by understanding how modern API integrations provide the same ease of use as traditional credit card gateways.

- Protect your revenue from fraudulent chargebacks by leveraging the inherent irreversibility of blockchain transactions to secure every sale.

- Navigate global compliance with confidence by partnering with providers that prioritize professional regulatory standards and secure offramp procedures.

- Discover how a comprehensive ecosystem allows you to convert crypto to USD or EUR instantly, bridging the gap between digital assets and traditional commerce.

Why Businesses Still Hesitate to Adopt Cryptocurrency Payments

The “Acceptance Gap” remains a visible friction point in modern commerce. While consumer interest in digital assets has surged to over 560 million global users, operational hesitation still prevents many enterprise leaders from fully integrating these systems. By 2026, cryptocurrency has transitioned from a speculative experiment into a standard asset class. However, a psychological barrier persists among traditional finance leaders who often view decentralized systems with caution. They fear a lack of institutional oversight or a loss of control over their financial pipelines.

Modern financial technology acts as a supportive facilitator in this environment. It doesn’t ask businesses to abandon their established practices; instead, it provides a professional bridge that connects traditional reliability with modern efficiency. By 2026, roughly 19% of U.S. small businesses have already adopted these tools to lower costs and reach new demographics. The goal is to turn technical complexity into a background process that feels like a standard business operation.

The Evolution of Merchant Crypto Adoption

Merchant services have moved far beyond the early days of direct peer-to-peer transfers. In the past, “do-it-yourself” crypto acceptance required businesses to manage private keys and manual conversions, which led to many of today’s common objections to accepting crypto payments. Today, sophisticated gateway ecosystems have replaced those high-friction methods. Institutional-grade infrastructure now handles the underlying blockchain mechanics, allowing merchants to focus on their core growth while the technology manages the transaction flow in the background.

Identifying the Core Categories of Resistance

Resistance to adoption generally falls into three distinct categories that require specific technological answers. Understanding these risks is the first step toward mitigating them effectively:

- Financial Risk: Concerns regarding market volatility and the immediate liquidity of digital assets.

- Operational Risk: Anxiety over technical integration, security protocols, and the potential for hacking.

- Compliance Risk: Navigating Regulatory Compliance and Tax Complexity across different jurisdictions.

By utilizing a professional payment API, businesses can bypass these hurdles. These systems are designed to automate compliance and security, ensuring that your transition into digital finance is both secure and legally sound. When you implement a structured fiat settlement process, the perceived risks of the crypto market effectively disappear from your balance sheet.

Objection 1: Market Volatility and Financial Stability Risks

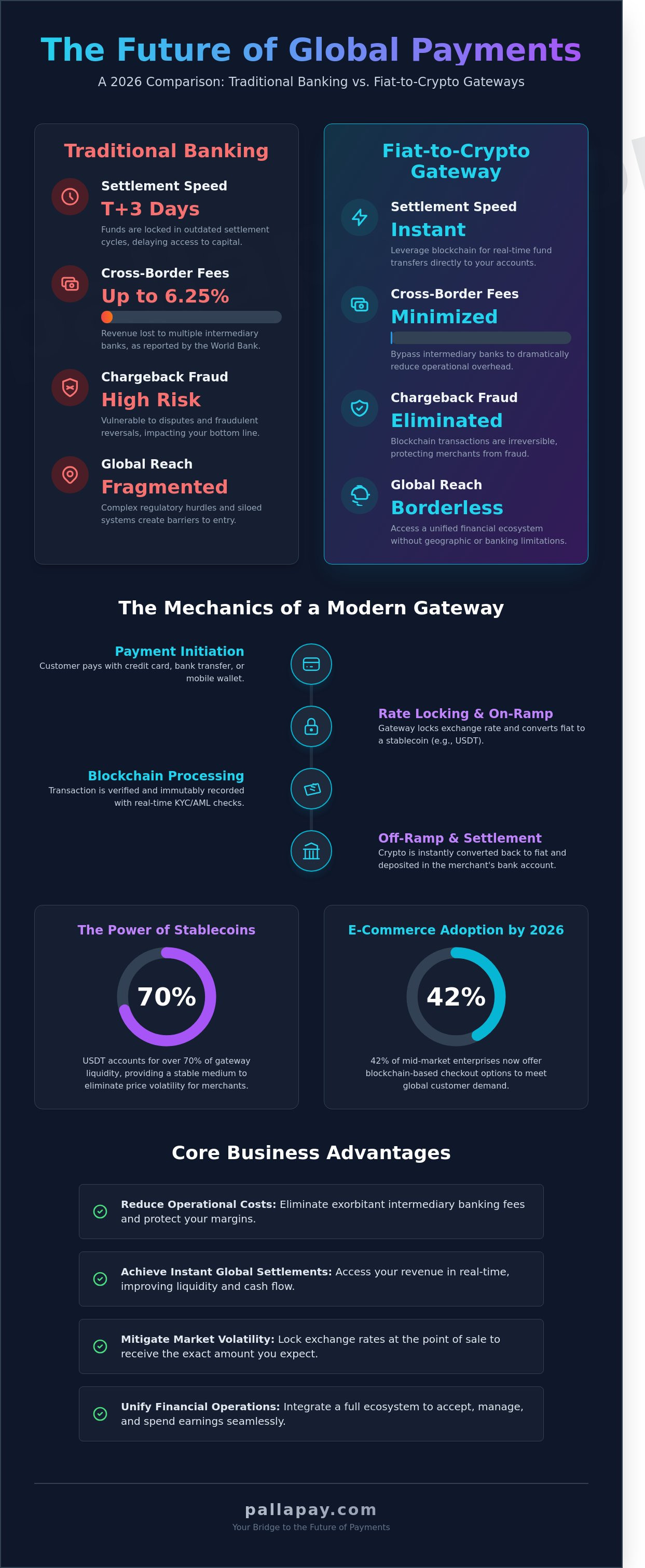

Market volatility is frequently cited as the most significant hurdle for merchants. The fear of losing profit margin between the moment of a transaction and the eventual bank deposit is understandable. This concern remains one of the most common objections to accepting crypto payments, but it’s based on an outdated understanding of how modern payment gateways function. By 2026, the technology has evolved to remove this risk entirely through automated background processes. Businesses no longer need to speculate on market prices to participate in the digital economy.

Modern financial infrastructure acts as a protective shield for your margins. When a customer initiates a payment, the exchange rate is captured in real time. This ensures that the value you see at the point of sale is the value that arrives in your account. By removing the exposure to market swings, businesses can focus on growth rather than monitoring price charts. If you’re looking to stabilize your revenue, you can convert crypto to USD instantly to maintain your financial stability.

How Fiat Settlement Eliminates Price Risk

The primary solution to volatility is a robust fiat settlement system. This mechanism locks in the exchange rate at the exact moment a customer clicks “pay.” Even if the underlying asset’s value fluctuates seconds later, the merchant receives the precise fiat amount requested. This process transitions digital assets to fiat currency automatically, ensuring that businesses never have to ‘hold’ volatile assets on their balance sheet. It effectively treats a Bitcoin or Ethereum transaction with the same financial stability as a standard credit card payment.

The Role of Stablecoins in 2026 Commerce

Stablecoins like USDT have become a preferred settlement layer for international B2B transactions. These assets offer the speed of blockchain technology without the price fluctuations of traditional cryptocurrencies. While traditional banking cycles often take 3 to 5 business days for cross-border settlement, digital asset rails provide near-instant movement of value. This efficiency reduces cross-border transaction fees and improves cash flow management. For businesses requiring physical operational flexibility, services to sell crypto to bank accounts or exchange USDT for cash provide the liquidity needed to meet immediate obligations.

Strategic partners now offer comprehensive ecosystems that handle these complex technical conversions. This allows you to accept a wide variety of assets while settling in the currency that best suits your operational needs. By utilizing these professional tools, you can turn a perceived financial risk into a distinct operational advantage.

Objection 2: Regulatory Compliance and Tax Complexity

Regulatory uncertainty often manifests as a “Regulatory Ghost” in the boardroom. Finance directors frequently worry that adopting digital assets will lead to unintentional non-compliance with anti-money laundering (AML) protocols or complex tax audits. These fears represent significant common objections to accepting crypto payments. However, the regulatory landscape of 2026 is far more defined than in previous years. The enactment of the GENIUS Act in July 2025 provided a comprehensive framework for stablecoins, while the CLARITY Act of 2026 defined most digital assets as commodities. These legislative milestones have replaced ambiguity with a clear roadmap for institutional adoption.

By choosing a partner with formal Money Services Business (MSB) registration, merchants effectively transfer the bulk of the compliance burden to the provider. This professional bridge ensures that every transaction is screened and recorded according to global standards. It’s a shift from a “do-it-yourself” compliance model to a managed service that scales with your business. This level of institutional financial reliability is essential for any merchant aiming to capture a share of the 560 million global crypto users safely.

Partnering with Regulated MSB Entities

MSB registration is the non-negotiable gold standard for merchant security in 2026. When you partner with a regulated entity in regions like the US or Canada, you gain access to institutional-grade financial reliability. The gateway handles the complex Know Your Customer (KYC) and AML checks automatically. This process protects your business from high-risk actors while maintaining a frictionless experience for legitimate customers. It’s a strategic move that transforms a potential legal liability into a secure, regulated operational flow. A regulated partner acts as a supportive facilitator, allowing your leadership team to focus on strategic growth rather than navigating the intricacies of federal laws.

Automating Tax and Accounting Workflows

Manual bookkeeping is no longer a requirement for digital asset commerce. Modern gateways generate automated, tax-ready reporting that simplifies the audit trail for your internal teams. These systems track capital gains at the moment of transaction, removing the need for manual ledger entries or complex year-end reconciliations. By utilizing specialized e-commerce industry solutions, you can integrate sales data directly into your existing accounting software. These automated reporting features are essential for maintaining a clean audit trail across 180+ countries. It ensures that your tax filings are accurate and defensible, regardless of the volume of international sales.

Objection 3: Technical Integration and Security Concerns

Technical complexity and perceived security vulnerabilities are often the final hurdles for merchants. Many business leaders believe that integrating blockchain technology requires a specialized internal team or a complete overhaul of their existing stack. These technical anxieties are among the most persistent common objections to accepting crypto payments. In reality, the 2026 integration landscape has achieved parity with traditional payment systems. Modern solutions are designed to be plug-and-play, ensuring that the underlying mechanics remain invisible to both the merchant and the end consumer.

Security is no longer a matter of manual oversight but of institutional-grade automation. Protecting the digital perimeter involves multi-signature wallets and advanced encryption protocols that far exceed the security standards of traditional magnetic stripe or chip-and-pin systems. By utilizing a professional payment API, you can secure your transaction data without needing to understand the complexities of cryptographic hashing. This technology creates a secure environment where digital assets move with the same reliability as fiat currency, protecting your business from the erratic nature of the early crypto era.

Seamless API and POS Integration

Implementing these solutions follows a logical, step-by-step progression that mirrors standard payment setup. First, select a gateway with a robust API to handle the background logic and currency conversions. Second, configure your checkout experience to ensure zero-friction user journeys, allowing customers to pay with their preferred assets in seconds. For physical storefronts, deploying dedicated crypto POS machines allows for real-time processing in retail store environments. This hardware-software synergy ensures that whether your customer is online or in-person, the transaction is handled with absolute trust and speed. Modern API documentation is now so streamlined that integration times have dropped from weeks to just a few days of configuration.

Turning Irreversibility into a Security Feature

Traditional finance often highlights transaction irreversibility as a risk, yet for merchants, it’s a significant security upgrade. Credit card chargeback fraud remains a hidden cost that drains billions from global commerce annually. Crypto payments protect your revenue from “friendly fraud” because once a transaction is verified on the blockchain, it cannot be reversed by the customer. This transparency builds a different kind of trust. Every sale is final and verifiable, eliminating the anxiety of unauthorized reversals weeks after a product has shipped. By removing the threat of chargebacks, you can protect your margins and simplify your dispute management processes.

If you’re ready to secure your revenue stream, you can integrate a professional payment API today to eliminate chargeback risks and streamline your global operations.

Strategic Solutions: How Pallapay Eliminates Merchant Friction

Pallapay serves as the professional bridge between traditional commerce and the digital future. While previous sections have dismantled the common objections to accepting crypto payments through technical and regulatory evidence, the practical execution requires a unified ecosystem. A fragmented approach often leads to operational friction; however, an integrated platform ensures that every transaction remains efficient and secure. Pallapay provides this stability by combining institutional financial reliability with accessibility-focused tools that simplify the user experience. By 2026, over 560 million global users are active in the digital asset space, and having a strategic partner allows you to capture this market without technical debt.

Speed is a definitive competitive edge in modern finance. The ability to convert crypto to fiat instantly ensures that your business maintains the liquidity required for daily operations. Whether you need to settle in USD, EUR, GBP, or CNY, the infrastructure is designed to handle these conversions in real time. This global reach extends to over 180 countries, providing a secure perimeter for international expansion. You don’t need to be a blockchain expert to succeed; you simply need a facilitator that handles the background complexity while you focus on your core growth objectives.

The Pallapay Ecosystem Advantage

The Pallapay ecosystem is built for high-performance commerce. It combines advanced crypto security with high-volume OTC capabilities, allowing merchants to move significant assets without market slippage. Global desks provide professional support for complex transactions, ensuring that your financial operations remain grounded in practical commerce. A unique benefit of this ecosystem is the Pallapay Mastercard. This tool enables you to spend your crypto earnings instantly at any point of sale, bypassing the multi-day delays typical of traditional banking systems. It turns your digital revenue into a liquid resource for immediate reinvestment or operational expenses.

Getting Started: The Path to Crypto Readiness

Transitioning your business is a logical, step-by-step progression. You can begin by setting up a merchant account and selecting the integration that suits your business model, such as an online gateway for ecommerce or a physical POS machine for retail. For businesses that require traditional bank settlement, the crypto off-ramp provides a streamlined path for transfers to your corporate accounts. This ensures that you can always access your funds in the currency of your choice, including AED, INR, or EUR. The common objections to accepting crypto payments are solved through this comprehensive suite of services. Join the evolution of global commerce today by partnering with a trusted strategic facilitator and secure your place in the future of finance.

Securing Your Competitive Advantage in the Global Economy

The landscape of 2026 offers unparalleled opportunities for businesses to move beyond traditional payment limitations. By addressing the common objections to accepting crypto payments through instant fiat settlement and regulated compliance, you can protect your margins while expanding your global reach. You’ve seen how modern technology transforms perceived risks into operational strengths. Institutional-grade security and automated tax reporting are no longer optional extras; they’re essential tools for any growth-oriented enterprise.

As a regulated MSB in the USA and Canada, Pallapay provides the 2026-ready secure POS and API infrastructure needed to serve customers in over 180 countries. This comprehensive ecosystem ensures that your transition is both efficient and legally sound. It’s time to scale your business with Pallapay’s secure crypto payment gateway. Embracing these advancements positions your company at the forefront of financial innovation. The transition to digital finance is a standard business operation that empowers your brand to lead in an evolving global market. Your progress starts today.

Frequently Asked Questions

Is it legal for my business to accept cryptocurrency payments in 2026?

Yes, it’s legal in many major economies, including the United States and Canada. The GENIUS Act of 2025 and the CLARITY Act of 2026 have established a clear regulatory framework for digital assets and stablecoins. By using a regulated Money Services Business (MSB), you ensure that your operations comply with federal standards, effectively removing the legal ambiguity that once characterized the industry.

How do I protect my business from Bitcoin price volatility?

You can protect your margins by utilizing instant fiat settlement services. This technology captures the exchange rate at the exact moment of the transaction, ensuring the value you receive isn’t affected by subsequent market swings. Many businesses choose to convert crypto to USD or EUR immediately. This process eliminates the financial risk of holding volatile assets on your balance sheet while allowing you to enjoy the benefits of digital commerce.

Do I need to be a tech expert to integrate a crypto payment gateway?

You don’t need specialized technical expertise to implement a modern crypto payment solution. Current API integrations and physical POS machines are designed for seamless, plug-and-play operation within your existing infrastructure. These systems handle the complex background mechanics of the blockchain, allowing your team to focus on standard business operations. Most merchants can complete the setup process in just a few days by following a logical configuration guide.

What are the tax implications of accepting digital assets for services?

Modern gateways simplify tax compliance by generating automated, tax-ready reporting for every transaction. These systems track capital gains and losses at the point of sale, which removes the need for manual ledger entries or complex year-end reconciliations. By addressing these common objections to accepting crypto payments through automation, you maintain a clean audit trail. This ensures that your accounting workflows remain efficient and accurate across different jurisdictions.

Can I convert crypto payments directly into my local bank account?

Yes, you can transfer your earnings directly to your local bank account. Professional off-ramp services allow you to sell crypto to bank accounts in multiple currencies, including USD, EUR, and GBP. This bridge between digital assets and traditional finance ensures you have immediate access to liquidity for your operational needs. The process is fast and secure, providing the same reliability as a standard international wire transfer but with improved settlement speeds.

How do crypto transaction fees compare to traditional credit card processors?

Cryptocurrency transaction fees are typically significantly lower than traditional credit card processing costs. While credit card swipe fees often range from 1.5% to 3.5%, digital asset gateways generally charge between 0.5% and 2%. For example, U.S. business owners paid $187.2 billion in swipe fees in 2024. Adopting crypto payments can lead to substantial cost savings, directly improving your profit margins on every international and domestic sale.

What happens if a customer sends the wrong amount of crypto?

The payment gateway handles payment discrepancies through automated reconciliation protocols. If a customer sends an incorrect amount, the system flags the transaction and provides a clear path for a refund or a top-up payment. This prevents manual bookkeeping errors and ensures your records remain precise. These automated systems are designed to resolve common objections to accepting crypto payments by providing a predictable, professional experience for both the merchant and the consumer.

Is there a risk of my merchant account being hacked?

Institutional-grade security measures effectively mitigate the risk of unauthorized access. Regulated providers utilize advanced encryption, multi-signature wallets, and cold storage to protect your assets and data. These protocols are far more robust than the security standards used in many traditional financial systems. By choosing a partner with a proven track record in digital asset security, you ensure that your merchant account remains protected against modern cyber threats.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.