In 2026, the era of relying on uncertain peer-to-peer markets and risking bank account freezes is officially over for sophisticated investors in the Emirates. You’ve likely felt the frustration of high slippage or the anxiety of wondering if your bank will flag a large settlement as suspicious. It’s a legitimate concern because regulatory standards like the VARA Travel Rule now apply to every transaction over AED 3,500. This guide provides the definitive blueprint for a secure crypto to bank transfer uae, ensuring your digital assets reach your AED account with institutional-grade speed and total regulatory compliance.

You’ll master the process of converting assets while maintaining the 0% personal income tax benefits currently available to individual traders. While standard retail platforms often struggle with liquidity, professional OTC gateways provide the instant settlement required for high-volume operations. We’ll examine the specific documentation needed for transfers exceeding AED 100,000 and show you how to align your off-ramp strategy with current AML laws. By the end of this article, you’ll have a clear strategy to move your capital with the confidence of a global fintech leader.

Key Takeaways

- Understand how to align with the latest 2026 VARA standards to ensure every large-scale liquidation remains fully compliant with local AML mandates.

- Discover why selecting a regulated gateway for your crypto to bank transfer uae is the most effective strategy for avoiding account freezes and minimizing slippage.

- Master the Level 2 KYC requirements and verification protocols needed to unlock institutional-grade withdrawal limits for seamless AED deposits.

- Identify the specific transaction triggers that cause bank flagging and learn how to navigate daily and monthly transfer thresholds with zero friction.

- Learn how to utilize professional bridges that offer instant settlement and the security of global MSB registrations for your fiat off-ramping.

The Landscape of Crypto to Bank Transfers in the UAE (2026)

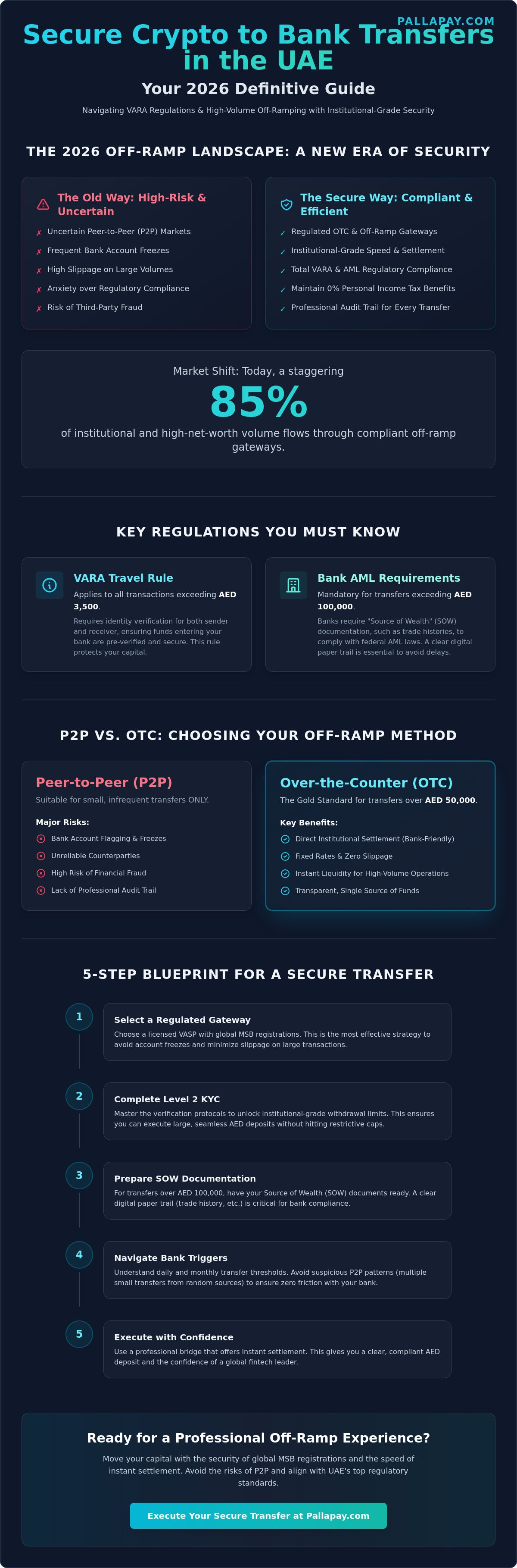

The United Arab Emirates has established itself as the premier global destination for digital asset management. By April 2026, the regulatory framework has matured beyond experimental phases into a robust ecosystem that prioritizes investor security and institutional stability. It’s completely legal to execute a crypto to bank transfer uae, provided you utilize licensed entities that adhere to federal anti-money laundering (AML) protocols. This legal clarity is documented in broader global cryptocurrency regulations, which highlight the UAE’s proactive stance in creating a secure environment for virtual asset service providers (VASPs).

The market has moved away from high-risk peer-to-peer (P2P) exchanges. In previous years, P2P was a common method, but it frequently led to account freezes due to third-party fraud. Today, 85% of institutional and high-net-worth volume flows through compliant off-ramp gateways. These platforms provide the liquidity necessary for large-scale settlements without the slippage or security risks inherent in decentralized marketplaces. This shift ensures that every transfer is backed by a professional audit trail.

VARA Regulations and Your Bank Account

The Virtual Assets Regulatory Authority (VARA) has streamlined the off-ramping process by implementing the “Travel Rule” for all transactions exceeding AED 3,500. This requires providers to verify the identity of both the sender and receiver, which actually protects you by ensuring the funds entering your bank account are pre-verified. Working with an MSB-registered provider is essential for maintaining trust with local financial institutions. VARA’s comprehensive oversight has transformed the UAE into a high-liquidity corridor where blockchain assets are treated with the same professional rigor as traditional fiat currency.

Bank Friendliness: The Current State of UAE Financial Institutions

Banks like Wio and Emirates NBD have pioneered the integration of virtual asset flows into standard retail banking. However, compliance remains a top priority. For any crypto to bank transfer uae exceeding AED 100,000, banks will mandate “Source of Wealth” (SOW) documentation to satisfy federal AML laws. Delays typically occur when users fail to provide clear trade histories or proof of initial investment. You can avoid these bottlenecks by maintaining a clear digital paper trail and using a dedicated settlement partner that understands these institutional requirements.

Methods for Converting Crypto to Bank Deposits

Choosing the right off-ramp method depends entirely on your transaction volume and your requirement for speed. In the 2026 financial landscape, the primary objective of a crypto to bank transfer uae is to bridge the gap between digital liquidity and traditional bank accounts without triggering security alerts. Direct fiat gateways have become the standard for retail users because they offer a streamlined KYC process. However, these gateways often impose strict daily limits that can hinder larger operations. For high-volume traders, the choice typically narrows down to peer-to-peer markets or professional over-the-counter desks.

Peer-to-peer (P2P) trading remains popular for small, occasional transfers, but it carries inherent risks for frequent users. Financial institutions often flag accounts that receive multiple transfers from various individual accounts, as this pattern mimics suspicious activity. To ensure your activities remain within the law, you should consult the official UAE crypto guidance regarding unlicensed service providers. Relying on unverified counterparties can lead to administrative delays or even permanent account restrictions.

P2P vs. OTC: Which is Right for You?

For transfers exceeding 50,000 AED, over-the-counter (OTC) desks are the gold standard. Unlike P2P, where you deal with individuals, OTC desks provide direct institutional settlement. This eliminates the “hidden costs” of P2P, such as high slippage and the risk of unreliable counterparties failing to release funds. OTC services offer a fixed rate and a single, transparent source of funds, which is significantly more attractive to bank compliance departments. If you’re managing a significant portfolio, an institutional off-ramp partner is the most secure way to preserve your capital’s value.

Crypto-linked Mastercards offer a different utility by allowing you to spend assets directly at point-of-sale terminals. While convenient for daily expenses, they don’t serve as a replacement for a true bank transfer. They’re best used as a complementary tool rather than a primary method for moving large sums into a savings or business account.

Automated Fiat Settlement Systems

Modern fintech platforms now utilize automated systems to facilitate instant fiat settlement for business operations. These systems are designed to reduce volatility risk by locking in exchange rates at the moment of the transaction. By using a professional gateway, you can convert your digital assets into AED bank deposits within minutes. This level of efficiency is essential for businesses that need to maintain steady cash flow while operating in the virtual asset space. It’s not just about moving money; it’s about doing so with the precision that modern commerce demands.

Step-by-Step: Executing a Crypto to Bank Transfer in the UAE

Executing a professional crypto to bank transfer uae requires a systematic approach to satisfy both blockchain protocols and institutional compliance. The transition from digital liquidity to a verified bank deposit is a five-stage process that prioritizes security at every junction. Your first priority is selecting a regulated off-ramp provider that maintains deep local AED liquidity. This ensures that your settlement doesn’t suffer from high slippage or extended waiting periods common with international exchanges that lack local banking relationships.

Once you’ve selected a provider, you must complete Level 2 KYC and account verification. As of April 2026, this typically involves submitting a valid Emirates ID and proof of residence to unlock institutional-grade withdrawal limits. For “Verified Plus” users on major platforms, these limits can range from $2 million to $10 million daily. After verification, you can convert your digital assets, such as USDT or BTC, into AED. The final step involves initiating the transfer to your bank account, where you’ll choose between a local transfer for speed or a SWIFT transfer for broader financial management.

Preparing Your Documentation

UAE financial institutions are rigorous regarding Anti-Money Laundering (AML) standards. To ensure a smooth deposit, you must prepare a “Source of Funds” (SOF) file. For withdrawals exceeding AED 100,000, banks will likely request trade certificates, transaction receipts, or even tax residency proofs. Maintaining a detailed trade log serves as your safety net. If a bank inquiry arises, providing a clear digital trail from the initial crypto purchase to the final liquidation demonstrates that your capital is legitimate and compliant with federal laws.

Optimizing for Speed and Fees

Timing your transfer is a critical factor in achieving instant settlement. While blockchain networks operate 24/7, local banking systems adhere to standard UAE business hours. Initiating your transfer during these windows avoids the “weekend bottleneck” where funds might sit in a clearing state. You should also compare fee structures carefully. While some exchanges charge a flat fee of 50 AED for withdrawals, others use a percentage-based spread. Using the Pallapay off-ramp is a strategic choice for those requiring same-day AED delivery with minimal friction. This professional bridge handles the heavy lifting of technology behind the scenes, allowing you to focus on your core financial objectives.

Overcoming Common Challenges in UAE Crypto Withdrawals

Successfully managing a crypto to bank transfer uae requires more than just technical knowledge; it demands an understanding of institutional risk management. Many users fear their bank accounts will be frozen, but in the 2026 regulatory environment, banks don’t freeze accounts simply because they’re linked to virtual assets. Instead, restrictions usually stem from unexplained wealth or third-party transfers that trigger AML alerts. To prevent these bottlenecks, ensure your exchange account name matches your bank account name exactly. Discrepancies between “John Doe” and “Doe Holdings” are a primary cause for “return to sender” scenarios and extended settlement delays.

You must also navigate the specific thresholds established by the Virtual Assets Regulatory Authority (VARA). For instance, any transfer exceeding AED 3,500 falls under the “Travel Rule,” requiring full originator and beneficiary data. If you’re moving amounts over AED 100,000, your bank’s compliance department will likely pause the transaction until you provide a trade certificate or proof of tax residency. Managing these daily and monthly thresholds is a standard part of modern financial operations, not a sign of a failed system.

What to Do If Your Transfer Is Flagged

If your transaction is flagged, don’t panic. The immediate step is to contact your bank’s compliance department with your pre-prepared documentation. Transparency is your best defense in the 2026 landscape. A professional OTC crypto exchange can often mediate these inquiries by providing a clear, institutional-grade audit trail that banks trust. Providing a single, comprehensive PDF containing your trade history and source of funds usually resolves most inquiries within 24 to 48 hours.

Managing Large Volume Liquidity

Cashing out over 1M AED requires a strategy that avoids market impact and high slippage. Standard retail exchanges often lack the depth to handle such volume without significant price drops. This is where OTC crypto exchange services become essential for institutional wealth management. These desks provide deep liquidity and fixed rates, ensuring your capital remains intact during the conversion window.

It’s also vital to consider the tax implications of your liquidation. While the UAE maintains a 0% personal income tax policy on crypto gains for individuals in 2026, businesses are subject to a 9% corporate tax on profits exceeding 375,000 AED. By using a professional settlement partner, you can ensure your transfers are categorized correctly to maintain your tax efficiency. If you’re looking to liquidate high-value assets without friction, consider utilizing our secure off-ramp services to ensure your capital reaches its destination safely.

Pallapay: The Professional Bridge for UAE Crypto Off-Ramping

Pallapay operates as the definitive destination for institutional and retail users seeking a seamless crypto to bank transfer uae. We bridge the gap between blockchain innovation and traditional financial reliability by providing a secure, utility-focused gateway. Our platform is backed by institutional-grade security, including MSB registrations in the United States and Canada, ensuring that every transaction meets global compliance standards. While other platforms operate solely in the digital space, we maintain a physical presence in the UAE’s primary financial districts, providing a level of accountability and trust that’s essential in the virtual asset industry.

Beyond AED settlements, we address the critical need for multi-currency liquidity that many competitors overlook. Our infrastructure allows for instant conversion and settlement into various global currencies, delivering funds directly into your verified accounts. This capability is vital for users who require:

- Instant AED Settlement: Direct deposits into local bank accounts with zero delays.

- Global Currency Access: Seamless conversion into USD, EUR, and INR for international operations.

- Liquidity Management: Access to deep pools that prevent slippage for high-volume liquidations.

This multi-currency approach ensures that high-net-worth individuals and businesses can manage diversified global portfolios without the friction of multiple intermediary banks. It’s a professional solution for those who operate across borders and need a reliable partner to handle the complexities of currency exchange.

The Pallapay Ecosystem Advantage

Efficiency is the core of our “all-in-one” ecosystem. By integrating the Pallapay Wallet with your local bank accounts, you’re able to manage the entire lifecycle of your assets within a single, secure interface. For businesses, we provide customized settlement solutions tailored for retail stores and e-commerce platforms. These tools allow you to accept digital payments and receive fiat deposits instantly, which accelerates your cash flow and supports rapid business growth. Our ecosystem ensures you’re never more than a few clicks away from your capital, regardless of where your business takes you.

Security and Compliance Standards

We’re committed to the highest AML and KYC standards to protect our users from the evolving risks of the digital landscape. Our systems are designed to handle high-volume traders, protecting them from slippage and counterparty risk through deep, institutional-grade liquidity. We provide a transparent fee structure, such as the verified 0.05% plus 5 USDT rate for TRC20 withdrawals, ensuring there’s no hidden cost in your settlement. By handling the heavy lifting of technology behind the scenes, we ensure your crypto to bank transfer uae is always secure and compliant with the latest VARA mandates. Start your secure crypto-to-bank transfer today with Pallapay and embrace The Future of Payments.

Securing Your Financial Evolution

The path to a successful crypto to bank transfer uae in 2026 is defined by transparency and institutional-grade infrastructure. By moving away from high-risk peer-to-peer markets and embracing regulated OTC gateways, you protect your capital from slippage and the volatility of unverified counterparties. Maintaining a clear digital audit trail for transactions over AED 100,000 isn’t just a regulatory requirement; it’s a strategic advantage that builds long-term trust with your bank’s compliance department. This professional approach ensures your assets move from blockchain to bank account with total efficiency.

Pallapay serves as the definitive bridge for this transition. We provide the security of MSB registrations in the USA and Canada, offering the stability needed for instant AED and USD settlements. Our ecosystem handles the technological heavy lifting, allowing you to manage your global liquidity through a single, secure interface. Step into the future of payments with a partner that prioritizes your security and growth. Secure Your Instant Crypto to Bank Transfer with Pallapay today.

Frequently Asked Questions

Is it legal to transfer crypto to a UAE bank account in 2026?

Yes, it’s fully legal to perform a crypto to bank transfer uae in 2026. The UAE has established a robust legal framework through the Virtual Assets Regulatory Authority (VARA) and the Financial Services Regulatory Authority (FSRA). These bodies license virtual asset service providers (VASPs) to ensure all fiat settlements are conducted within federal anti-money laundering (AML) laws. Users simply need to utilize a regulated gateway to remain compliant with the current financial statutes.

Which UAE banks are currently the most crypto-friendly?

Wio Bank and Emirates NBD are currently recognized as leaders in supporting virtual asset transactions. These institutions have integrated specific compliance protocols to handle digital asset flows with high efficiency. While most major banks now accept these transfers, choosing a tech-forward bank reduces the likelihood of manual review delays. It’s always best to notify your relationship manager before initiating high-value liquidations to ensure a seamless experience within the banking system.

How long does a crypto to bank transfer typically take in the UAE?

Transfers typically settle within minutes to 24 hours depending on the chosen off-ramp method. Professional OTC desks and instant settlement gateways offer the fastest results, often providing same-day AED deposits for verified users. Standard exchange withdrawals might take 1 to 3 business days to clear through the local banking system. Using a local liquidity provider is the most effective way to minimize waiting times and avoid the bottlenecks associated with international clearing houses.

What are the fees associated with converting crypto to AED?

Fees vary by provider but usually include a flat withdrawal fee or a percentage-based spread. For example, Rain Exchange charges a flat 50 AED fee for fiat withdrawals to UAE banks. Other institutional platforms might charge a small percentage, such as 0.05% plus a flat amount in the withdrawn currency. Users should compare these costs against the exchange rate slippage to determine the total cost of their crypto to bank transfer uae operation.

Can I transfer large amounts of crypto to my bank without getting flagged?

You can transfer large amounts without being flagged by using a licensed over-the-counter (OTC) desk and providing proactive documentation. Banks flag transactions that appear inconsistent or lack a clear origin. By using a professional bridge that provides an institutional-grade audit trail, you demonstrate transparency to compliance officers. For transfers exceeding AED 100,000, pre-submitting your “Source of Wealth” documents to your bank’s compliance department is a standard best practice that prevents account freezes.

What documentation do I need to provide to my bank for crypto withdrawals?

You need to provide a valid Emirates ID or passport along with “Source of Funds” documentation. For larger withdrawals, banks require trade logs, transaction receipts, or tax residency certificates to satisfy AML requirements. Keeping a precise record of your initial crypto purchases and subsequent trades is essential for long-term account security. These documents serve as your safety net if the bank’s compliance team requests a manual review of your deposit to verify its legitimacy.

Can I withdraw crypto to a corporate bank account in the UAE?

Yes, withdrawing crypto to a corporate bank account is permitted for businesses dealing in virtual assets. However, these entities must be properly licensed and are subject to a 9% corporate tax on profits exceeding 375,000 AED as of 2026. Corporate transfers require more rigorous documentation than personal ones, including business licenses and audited financial statements. It’s a standard business operation for firms integrated into the UAE’s digital economy that prioritize professional capital management.

What is the difference between P2P and OTC for bank transfers?

The primary difference lies in the counterparty and the level of security provided. Peer-to-peer (P2P) involves trading with individuals, which carries a higher risk of bank flagging due to the inconsistent nature of the senders. Over-the-counter (OTC) desks provide direct institutional settlement from a single, verified source. For a secure crypto to bank transfer uae, OTC is the preferred choice for high-volume traders seeking to minimize slippage and maximize compliance with local financial regulations.

Disclaimer

The information provided on this website and blog is for general informational and educational purposes only and does not constitute financial, investment, legal, tax, or other professional advice.

Cryptocurrency and digital asset services may be subject to regulatory restrictions in certain jurisdictions. Users are solely responsible for ensuring compliance with applicable local laws and regulations before using any products or services mentioned on this website.

PallaPay does not guarantee the accuracy, completeness, or timeliness of any information published and accepts no liability for any loss or damages arising from reliance on the content. Any opinions expressed are those of the respective authors and may change without notice.

Certain services, features, or products referenced may be provided through third-party partners, licensed entities, or affiliated service providers subject to separate terms and regulatory approvals. Availability of services may vary by country or region.

This website may contain references to digital assets, virtual currencies, or blockchain-related services that are not available to residents of certain jurisdictions, including where prohibited by law. Nothing on this website constitutes an offer, solicitation, or recommendation to buy or sell any financial instrument or virtual asset.